Shares of Uber (UBER) are starting to find their legs after surging 45% off their June 2022 lows. Undoubtedly, the company faces many pressures as rising interest rates push investors to part ways with unprofitable growth companies. Though Uber has been racking up losses as of late, the firm is on the cusp of a big push into GAAP profitability at some point in 2024. If Uber can make good on its profitability goals, the stock is bound to be rewarded by investors. I am bullish on Uber stock.

Uber Stock: On the Cusp of Profitability

Uber has the growth story, but it also has the means to become a profitable company as management continues to iron out inefficiencies while environmental headwinds finally dissipate. Though Uber stock may be grouped alongside the broader basket of unprofitable tech plays, it may be more of an early-stage Amazon (AMZN), which was slammed for lacking profitability until after its big push.

Like Amazon, Uber is seeking to expand its total addressable market. The ride-hailing firm wants to have the one super-app that consumers go to if they need someone or something transported from point A to point B. With transportation services that go above and beyond its traditional ride-hailing or food-delivery service, Uber is well on its way to dominating the world of shared transportation.

Though a recession could take a bite out of supply, the mobility powerhouse seems unlikely to fall short of GAAP profitability within two years. As labor woes ease, Uber can get supply and demand in the right spot. Further, Uber One could be a profitability accelerator that many investors may discount.

The Uber One subscription offering — a service that offers subscribers discounts on rides, food delivery, and other perks — boasts more than 10 million users. Such a subscription could enhance margins and demand if it proves sticky. Uber One is an intriguing offering that could propel the top and bottom lines as it proves its value to consumers.

Uber Records Positive Free Cash Flow for the First Time

In the second quarter, Uber posted a $1.33 per-share loss, wider than the $0.27 per share loss expected. The earnings shortfall was forgiven by investors who applauded the firm’s $8.1 billion in revenue and its first-ever move into positive free cash flow. Uber’s free cash flow came in at $382 million for the second quarter, and the management team expects more free-cash-flow positivity to come as it looks to improve its profitability prospects.

Mobility demand remained incredibly robust, with no signs that an economic slowdown is looming. Undoubtedly, it will be interesting to see how demand fares as we inch closer to a recession. Uber’s service may be far more recession-resilient than many investors think, given the lack of money-saving alternatives. Indeed, Uber provides ample time savings compared to commuting via public transit.

Further, if the coming recession proves mild or short-lived, Uber may be able to trend higher while the rest of the market sinks. Until there’s evidence of fast-slipping demand, I think investors ought to give Uber the benefit of the doubt as it kicks into high gear with its profitability push.

Uber is Well-Equipped to Take Share

Even if a recession takes a small bite out of demand, Uber seems well-poised to add to its lead over rivals like Lyft (LYFT) in mobility and DoorDash (DASH) in food delivery. With such a strong network, the Uber One service could lock users within its ecosystem and cause some to delete rival apps.

Though 5% savings on rides and food delivery (zero delivery fees on select orders) may not seem like much of a benefit to subscribe for, I do think that many members will stick around after seeing just how much they’re saving in a given month.

Existing Uber users gain one month of free access to the service. In such a trial month, many will likely shut out other offerings for Uber’s mobility and delivery services. Indeed, most frequent users will find the savings from Uber One worthwhile.

Although additional savings for Uber One members are money out of the pockets of Uber, the positive effect on demand and greater certainty through rocky environments could prove more than worthwhile for Uber.

I view Uber One as a margin and sales driver that could be the secret sauce to put its competitors in their place. At the end of the day, Uber has a powerful network. With a service like Uber One, it’s leveraging its network incredibly well to cross-sell across its mobility and food delivery divisions.

Is Uber stock a Buy, Hold, or Sell?

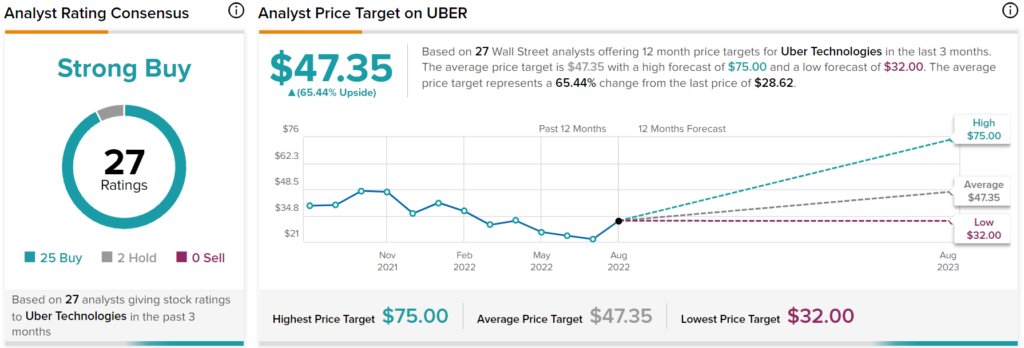

Uber stock has a Strong Buy consensus rating based on 25 Buys, two Holds, and zero Sells assigned in the past three months. The average Uber stock price target of $47.35 implies 65.4% upside potential. Analyst price targets range from a low of $32.00 per share to a high of $75.00 per share.

Takeaway: Profitability Could Power Uber Stock to New Heights

Uber stock is on a mission, and its Uber One could help it make a sustained move into profitability far sooner than most think. There are rivals, but Uber is more than capable of outdoing them going into recession.