After the stock’s nearly halving in value in the last nine months, Wells Fargo says it’s time to look on Wingstop (WING) more favorably again. Analysts at Wells Fargo (WFC) initiated coverage of Wingstop with an Overweight (Buy) rating and $270 price target, suggesting over 20% upside. Compares – jargon for how the company performed compared to the year before period – look set to lower the bar for success in the second half of the year.

While it comes against a tough industry backdrop as consumers rein in spending and a “growthy” valuation multiple that present near-term headwinds for the shares, there is a potential to re-rate into “much easier” compares in the second half of 2025, the analyst tells investors in a research note.

It believes Wingstop has multi-year sales levers, “top tier” paybacks, and strong free cash flow, and it recommends buying the recent pullback in the shares.

WING was hammered following the release of the restaurant company’s Q4 2024 earnings. Revenue of $161.82 million missed Wall Street’s estimate of $164.84 million, although earnings per share of $0.93 easily beat the $0.86 estimate. Guidance was weak though and, as it comes against tough compares in the first half of 2025, helped pushed the stock lower.

The stock was also hit by a wave of price target cuts. Piper Sandler’s Brian Mullan went from $300 to $271, TD Cowen’s Andrew Charles from $365 to $305 and then to $265, Stifel Nicolaus’ Chris O`Cull from $400 to $375, and Wedbush’s Nick Setyan cut the stock from $390 to $355.

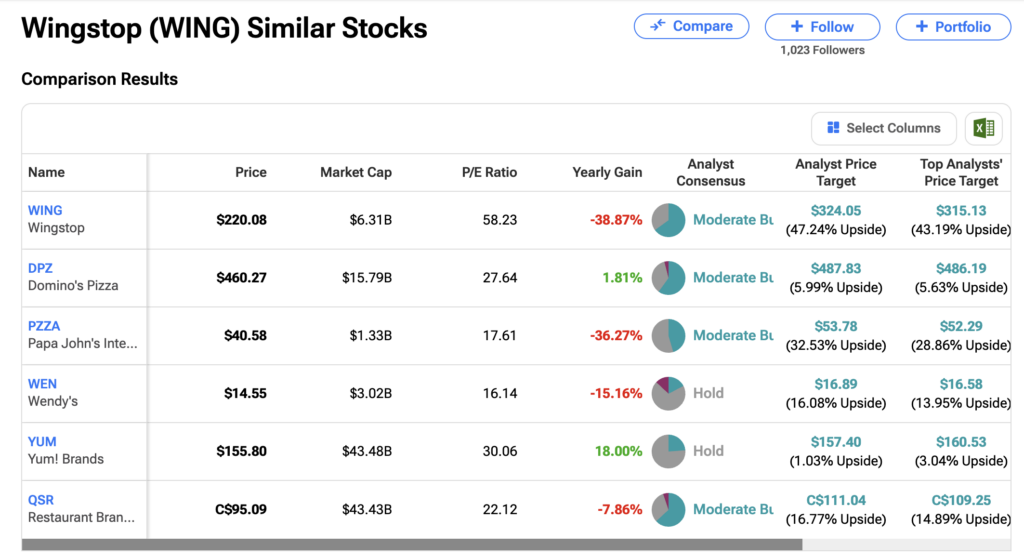

Investors interested in checking out stocks in a particular sector can use the Similar Stocks feature on a stock’s TipRanks page to find out about relevant peers such as Domino’s Pizza (DPZ) and Wendy’s (WEN).

In terms of the “growthy” valuation multiple mentioned above, WING trades on a price-to-earnings multiple of over 58, which is high compared to peers, as the graphic below indicates.