Shares of vacation rental management platform Vacasa, Inc. (VCSA) jumped nearly 35% yesterday on the back of the company’s robust second-quarter showing and upped guidance.

Buoyed by rising guest demand, revenue surged 30.6% year-over-year to $310.35 million, outperforming estimates by $24.9 million. Impressively, while the Street estimated a net loss per share of $0.18, Vacasa posted an EPS of $0.02. Also, the total gross booking value increased by 32% during this period to $676 million. In sync, the gross booking value per night also increased by 13% over the prior year to $411.

Furthermore, the platform added thousands of new homes during the quarter and expects a 30% increase in the number of homes under management this year.

The company has also raised its guidance owing to present booking trends. It now expects full-year 2022 revenue to land between $1.16 billion and $1.18 billion. Adjusted EBITDA is anticipated to be flat at a loss of $7 million.

Is Vacasa a Good Stock to Buy?

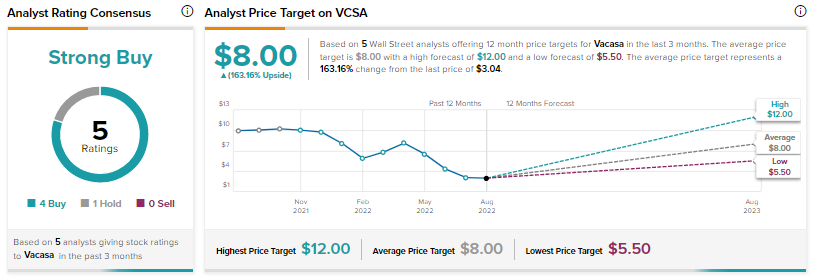

Following the Q2 results, JMP Securities analyst Nicholas Jones has reiterated a Buy rating on Vacasa alongside a price target of $6.50. Overall, the Street has a Strong Buy consensus rating on the stock with an $8 price target. This implies a massive 163.16% potential upside.

Hedge funds, though, are going the opposite way and have trimmed their Vacasa holdings by 857,000 shares in the last quarter. This indicates a negative hedge fund confidence signal in the stock.

Rising Travel is Lifting All the Boats

Vacasa already caters to guests across 400 locations in North America, Belize, and Costa Rica. The company adjusts rates in real-time to help maximize revenue for homeowners. Moreover, a focus on expanding its footprint coupled with a larger trend of increased travel and tourism bodes well for Vacasa.

The thesis is also playing out in bigger names, from Hyatt (H) to Airbnb (ABNB), who have seen robust numbers this quarter as well.

Read full Disclosure