Apple’s (NASDAQ:AAPL) new AI-driven iPhone is expected to boost the tech giant’s growth, but it might be wise to temper expectations.

Stay Ahead of the Market:

- Discover outperforming stocks and invest smarter with Top Smart Score Stocks

- Filter, analyze, and streamline your search for investment opportunities using Tipranks' Stock Screener

That’s the takeaway from Barclays analyst Tim Long, the Street’s biggest Apple bear, after reviewing the initial iPhone shipment data from China.

“Early pre-order data from China points to a softer start to the IP16 cycle, with a negative mix shift due to weakening consumer spend, macro pressure and competition,” the 5-star analyst said. “The roll-out of Apple Intelligence in Chinese language is not until CY2025, which may dampen early enthusiasm for IP16.”

Drawing insights from discussions with industry insiders and a review of pre-order numbers from major Chinese e-commerce platforms, Long observed a year-over-year decline in overall pre-orders during the first few days, along with a reduced share of pro models. The analyst mentioned that pro model orders dropped by double digits year-over-year, while base and plus models experienced y/y growth.

Additionally, as noted above, Apple Intelligence doesn’t launch in the Chinese language until calendar year 2025 while weak macroeconomic conditions and rising competition are still putting pressure on iPhone sales. To wit, in an effort to drive demand for the iPhone 15, Apple had to offer significant price discounts of around 20%.

Long also notes that delivery times for pro models were shorter compared to last year. “We heard that supply is better for IP16 due to better production yield but lower demand for pro models likely also contributed to shorter delivery times, in our view,” the analyst said on the matter.

As Apple typically adjusts its initial orders in early October based on sell-through data points, sell-through remains a critical metric. The earlier iPhone launch adds two extra days of sell-through to the September quarter (11 days for the iPhone 16 compared to 9 days for the iPhone 15), but this factor is largely accounted for. Long estimates September quarter iPhone shipments to be around 51 million units, due to the additional selling days. “However,” he goes on to say, “Dec-Q builds might be at risk if sell-throughs disappoint. And we heard some iPhone suppliers have.”

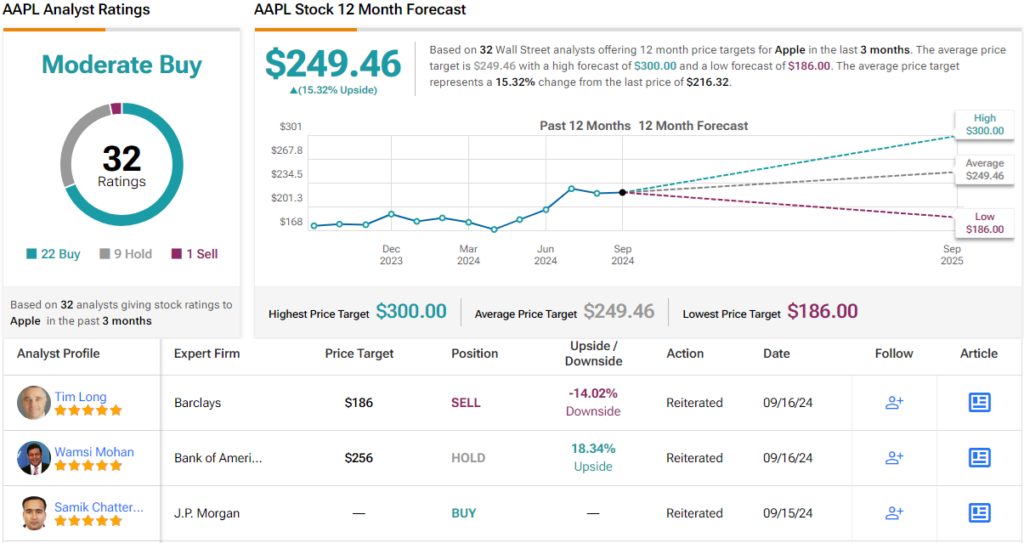

So, what does this ultimately mean for investors? The verdict according to Long is that AAPL remain an Underweight (i.e., Sell) while his $186 price target suggests the shares will lose 14% of their value over the next year. (To watch Long’s track record, click here)

However, Long stands alone in his bearish stance. The rest of the analysts have a more optimistic outlook, with additional 22 Buys and 9 Holds contributing to a consensus rating of Moderate Buy. The average price target sits at $249.46, suggesting shares will climb 15% higher over the next 12 months. (See AAPL stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.