Tech stocks have cooled off in the last two months after an impressive rally beginning in 2023. The tech-heavy Nasdaq Index (NDX) recently entered correction territory, which means it was down over 10% from all-time highs (although it has recovered a bit since). Nonetheless, the pullback allows investors to buy quality tech stocks such as Nvidia (NVDA) and Taiwan Semiconductor (TSM) at a discount. I am bullish on these two stocks due to their reasonable valuations, widening cash flows, and the artificial intelligence megatrend

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

Nvidia Stock: Down 16% from All-Time Highs

Yes, the hype for NVDA stock has dwindled recently, and the stock is down 16% from its all-time high, but looking at the bigger picture, the stock has surged over 700% since the start of 2023.

The key reason for Nvidia’s stellar stock returns is its earnings and revenue growth. It reported sales of $10.92 billion in Fiscal 2020 (ended in January), while revenue rose to $79.77 billion in the last 12 months. Moreover, its diluted earnings per share have risen from $0.11 to $1.71. So, the stock is doing well.

Nvidia and AI

Nvidia’s unrivaled GPUs are currently at the epicenter of the artificial intelligence megatrend and are the top supplier of computing power used to train AI models. However, the AI race is heating up as big-tech giants such as Meta Platforms (META), Microsoft (MSFT), and Alphabet (GOOGL) are investing heavily in this segment to gain an early-mover advantage.

Nvidia’s GPUs are part of the Data Center segment, which grew sales by a whopping 427% year-over-year to $22.6 billion in Fiscal Q1 of 2025. In the quarter ended in April, Data Center sales accounted for 86.8% of total sales.

According to KeyBanc (KEY), an investment bank, the upcoming launch of Nvidia’s Blackwell chips, including the GB200, could drive over $200 billion in Data Center revenue by 2025.

Nvidia’s Cash Flows and Dividends

Nvidia’s financial state and dividend payments are my final reason for bullishness on the stock. The company’s leadership in GPU allows it to enjoy attractive profit margins, resulting in widening cash flows.

The firm’s unlevered free cash flow has risen from $3.10 billion or $0.11 per share in Fiscal Q1 of 2024 to $12.26 billion or $0.61 per share in Fiscal Q1 of 2025.

Comparatively, Nvidia pays shareholders a quarterly dividend of $0.01 per share, indicating a payout ratio of less than 2%. Therefore, Nvidia has enough flexibility to reinvest in capital expenditures, target accretive acquisitions, and raise dividends further, all of which should enhance shareholder value.

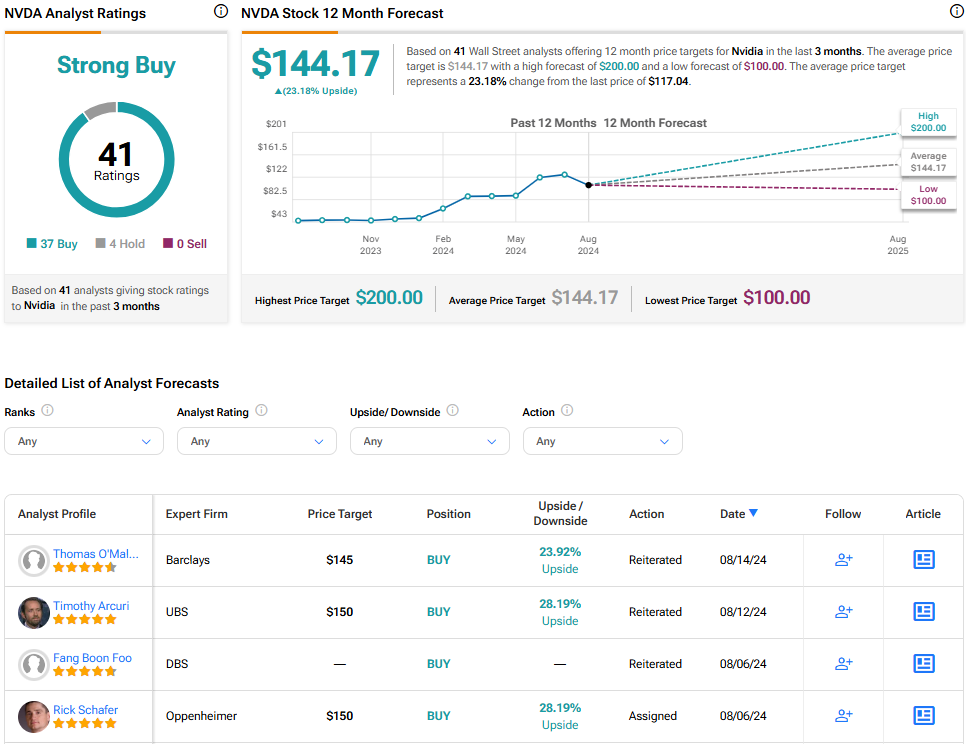

Is NVDA Stock a Buy, According to Analysts?

Of the 41 analysts tracking Nvidia, 37 have Buy ratings, four have Hold ratings, and none recommend a Sell, indicating a Strong Buy consensus rating. The average Nvidia stock price target is $144.17, indicating an upside potential of 23.2% from current levels.

Taiwan Semiconductor Stock: Down 13% from All-Time Highs

Another great stock is Taiwan Semiconductor, Valued at $870 billion by market cap, and is among the largest companies in the world. Founded in 1987, Taiwan Semiconductor manufactures integrated circuits and wafer semiconductor devices. TSM leads the global semiconductor foundry market with a 61.7% market share.

Several companies, including Nvidia, Apple (AAPL), and Alphabet, bank on TSM to manufacture chips, allowing it to increase its sales from $35.7 billion in 2019 to $74.97 billion in the last 12 months.

Down 13% from all-time highs, Taiwan Semiconductor stock has returned close to 740% to shareholders in the past decade. If we include dividend reinvestments, cumulative returns are closer to 966%. This is a mouthwatering statistic, which gives me great reason to be bullish on the stock. Moreover, TSM has not yet hit its ceiling.

The Bull Case for TSM

Taiwan Semiconductor’s growth story is far from over. It increased its sales by 33% year-over-year in Q2 of 2024 while forecasting growth of 32% in the current quarter. It has forecast capital expenditures between $30 billion and $32 billion in 2024, higher than its previous estimates of $28 billion to $32 billion. TSM emphasized allocating 70-80% of these expenses toward advanced technologies such as AI.

In the last 12 months, TSM’s unlevered free cash flow stood at $19.56 billion, up from $9.2 billion in 2019, providing it with the resources to target business growth.

Analysts tracking TSM stock expect adjusted earnings per share to rise by 26.4% to $6.55 in 2024. So, priced at 25.8x forward earnings, TSM stock is quite cheap, given that the average median multiple stands at 28x.

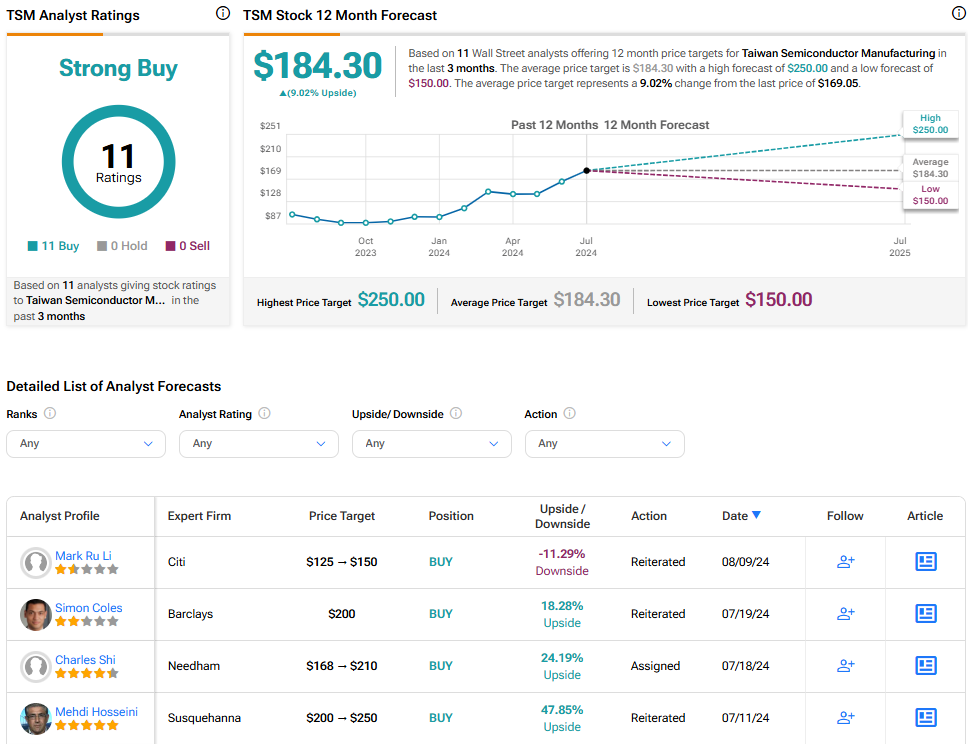

Is TSM Stock a Buy, According to Analysts?

Each of the 11 analysts tracking TSM stock has a Buy rating. The average target price for TSM stock is $184.30, indicating an upside potential of 9% from current levels.

The Takeaway

Both Nvidia and TSM are part of the AI sector, which is poised for rapid growth in the upcoming decade. Furthermore, the two companies trade at a discount to consensus analysts’ estimates and should deliver outsized gains due to widening cash flows and strong earnings growth. Both stocks present a compelling opportunity for investors, as both companies haven’t yet peaked. In conclusion, I am very much bullish on NVDA and TSM stocks.