Intel (INTC) stock has been down 43% over the past 12 months, massively underperforming peers in the semiconductor and artificial intelligence (AI) industries. A variety of reasons, including poor business performance, strategic challenges, sizable foundry losses, and high debt levels, have all contributed to Intel’s downfall and made me an INTC bear. The stock was once famous for leading the IT sector, but now, it is at an existential crossroads with other competitors at home and abroad, winning end-user hearts and minds ahead of it. The stock has metamorphosed from a leader into a laggard, and what’s worse, one of the best revenue opportunities in history (AI) has arrived at just the wrong time for INTC.

Confident Investing Starts Here:

- Easily unpack a company's performance with TipRanks' new KPI Data for smart investment decisions

- Receive undervalued, market resilient stocks straight to you inbox with TipRanks' Smart Value Newsletter

Moreover, INTC has been bleeding market share to rival Advanced Micro Devices (AMD) in both the retail and institutional segments and losing out more broadly as customers transition from CPUs to GPUs in the AI boom. Even though INTC has grown over the past five years, the stock is still going backward relative to its market peers.

Challenges Plaguing Intel’s Trajectory

Intel’s recent struggles paint a picture of a company grappling with operational and strategic headwinds. The semiconductor giant’s foundry business, critical to U.S. ambitions for chip independence, generated just $4.5 billion in Q4 2024 revenue – primarily from internal design units rather than external clients – and registered a stunning $2.3 billion loss.

Despite a deal to manufacture chips for Amazon (AMZN) Web Services, Intel Foundry has struggled to attract broader demand, reflecting a reliance on legacy processes and an inability to compete with Taiwan Semiconductor Manufacturing Company’s (TSM) sturdy manufacturing moat.

Compounding these issues, China – which accounts for 29% of Intel’s revenue – has hinted at antitrust probes targeting the firm, a retaliatory move amid U.S.-China trade tensions. This vulnerability threatens to slow Intel’s expansion as it faces rising capital expenditures and restructuring costs.

Meanwhile, TSMC’s dominance in cutting-edge nodes like chip-on-wafer-on-substrate (CoWoS) production in Taiwan underscores Intel’s technological lag. Despite a series of efforts to catch up with its peers – including the five nodes in a four-year program – Intel’s path to reclaiming leadership in advanced manufacturing remains fraught with execution risks and cultural mismatches in adopting TSMC’s proven methodologies.

Geopolitical Tailwinds and Nearshoring Opportunities

However, Intel’s fortunes could pivot on escalating U.S. efforts to secure semiconductor sovereignty. The Trump administration’s Executive Order 14179 and proposed revisions to the CHIPS Act prioritize domestic AI chip production, with Vice President Vance emphasizing the need for “American-designed and manufactured chips.”

As the U.S. pushes to reduce reliance on Taiwan – a geopolitical flashpoint due to China’s territorial claims – Intel benefits from subsidies and policy tailwinds aimed at bolstering local fabs. Nearshoring trends in the UK and Europe, driven by similar supply-chain resilience concerns, could further open partnerships or state-backed contracts for Intel Foundry.

While TSMC’s Arizona expansion faces delays in replicating Taiwanese expertise, a potential Intel-TSMC joint venture – though complicated by operational divergences – might accelerate knowledge transfer and CoWoS-capable production. Such collaboration could position Intel as a linchpin in Western efforts to balance TSMC’s Taiwan-centric operations, particularly if U.S.-China tensions escalate.

Valuation Intrigue

Intel’s valuation presents a complex picture, with the company facing significant challenges in the near term but showing potential for improvement in the coming years. Despite current struggles, analysts anticipate a gradual recovery in Intel’s financial performance. The price-to-earnings (P/E) ratio, currently not meaningful due to negative earnings, is expected to improve dramatically by 2028, potentially reaching 8.7 times. This trajectory suggests Intel may become increasingly attractive to value investors as its turnaround efforts take hold.

Consensus earnings per share (EPS) growth estimates paint an optimistic picture, with triple-digit growth projected for 2026 and strong double-digit growth in subsequent years. However, Intel’s substantial debt load of $50.7 billion remains a concern, especially compared to its market capitalization of $102.2 billion. While the company’s cash position of $22.1 billion provides some cushion, managing this debt will be crucial as Intel navigates its transformation and capital-intensive investments in manufacturing capabilities.

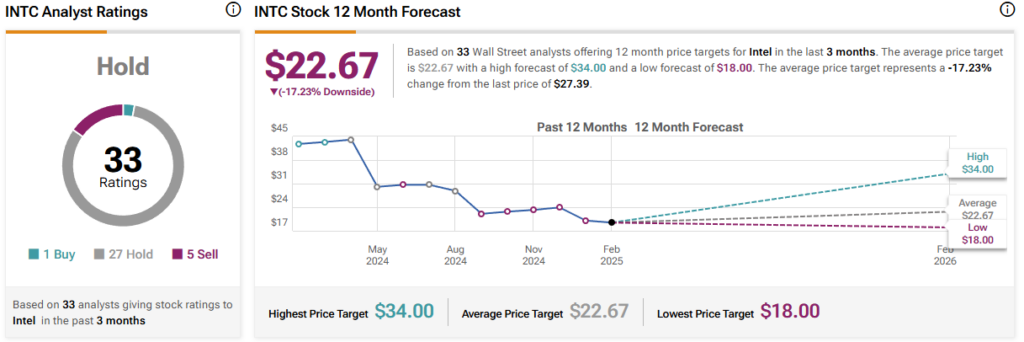

Is Intel a Buy, Hold, or Sell?

On TipRanks, INTC is a Hold based on one Buy, 27 Hold, and five Sell ratings assigned by analysts in the past three months. The average INTC stock price target is $22.67 per share, implying a 17.3% downside potential.

Intel Remains a Gamble at the Mercy of External Factors

I’m bearish on Intel due to its technological setbacks, mounting losses, and heavy debt burden. The foundry unit’s struggles and China’s antitrust threats add to the headwinds. However, US policy changes from the CHIPS Act and nearshoring initiatives could provide a turnaround opportunity if Intel executes its market offensive effectively. The firm’s valuation hints at a potential upside if projected earnings growth materializes, but with analysts overwhelmingly neutral, Intel remains a high-risk bet dependent on geopolitical shifts and operational improvements.