Record quarterly revenues for Duolingo (DUOL) did not translate into a gain for the stock, as the company warned that increased spending on marketing and developing artificial intelligence features could harm future profits. Shares of the language learning app are down over 7% in Friday’s premarket session despite the company beating expectations for its top line in Q4 and offering upbeat guidance for revenue growth.

DUOL Sees Record Users

Daily active users (DAUs) rose 51% in the Fiscal fourth quarter of 2024 from a year before to 40.5 million, while the number of paid subscribers rose 43% year-on-year to 9.5 million.

Revenues in the fourth quarter rose 39% to $209.6 million, above Wall Street’s estimates, while net income was up from $12.1 million in the year-ago quarter to $13.9 million. Bookings were $271.6 million, up 42% from a year before.

Guidance on revenues was also solid, with the company guiding Fiscal 2025 first quarter revenue between $220.5 million and $223.5 million, against a consensus estimate for around $220.8 million.

DUOL Expects Margin Pressure

But concerns about margins in the first half of the year helped to drive investor sentiment down after a solid rally this year. Investments in AI features and increased marketing spending will “front loaded” in the first half of the year.

In Fiscal 2025, the company expects a “temporary” 170 basis point year over year impact on gross margin, with the biggest impact in the first half, when it expects a 300bps hit to its margins. The company guided adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) margin in the first half of 25%, below the 25.7% reported for Fiscal 2024.

“There’s going to be an upfront cost for AI, which will happen probably throughout this whole year,” said CEO Luis von Ahn on the call with analysts. “We expect margins to improve in the second half of the year as we work to improve AI costs.”

The company forecasts “meaningful margin expansion in Q3 and Q4 as we realize AI cost efficiencies and as our marketing spend as a percentage of revenue comes down,” he added.

Despite the margin concerns, von Ahn nevertheless hailed a “truly exceptional” fourth quarter. The company saw its highest ever quarterly bookings, revenue, daily active users, and net new subscribers, he said.

DUOL stock was recently buoyed by reports it’s seeing a big surge in users signing up to learn Chinese.

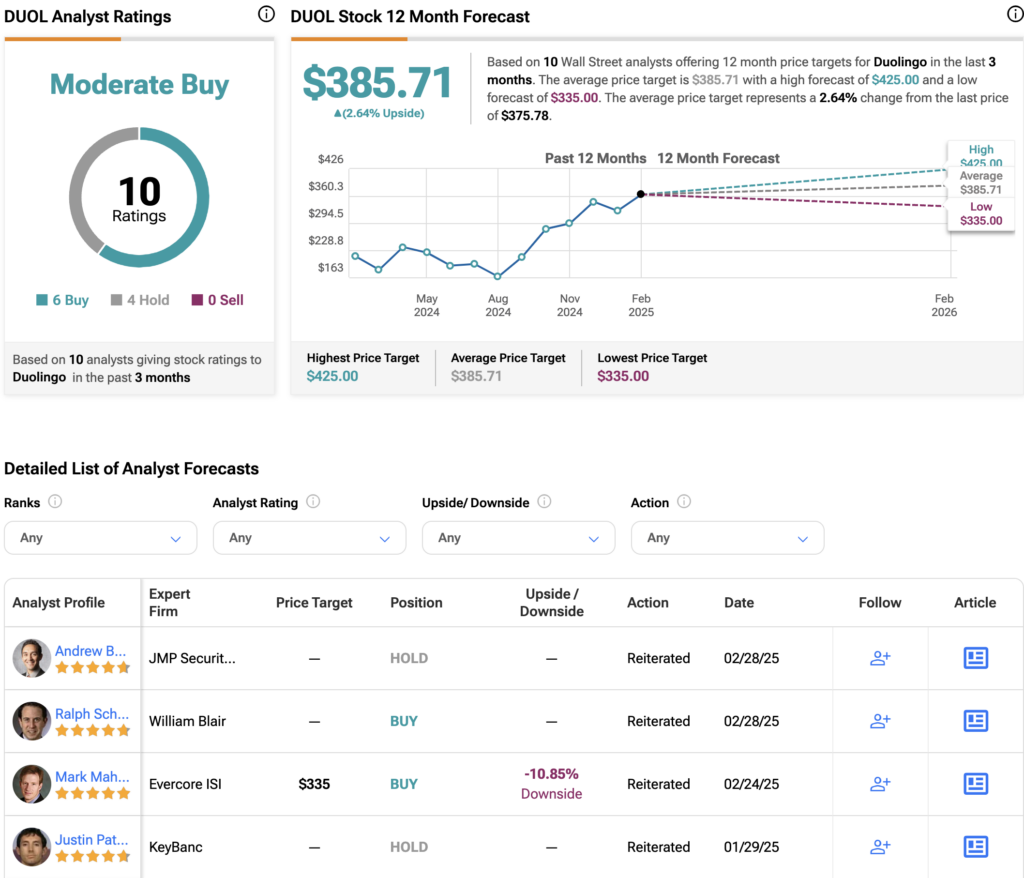

Is DUOL a Good Stock to Buy?

Overall, Wall Street has a Moderate Buy rating on DUOL, based on six Buys and four Holds. After rallying over 90% in the last 12 months, the average DUOL price target of $385.71 implies over 2% upside to current levels, though analysts may make changes after the earnings update.