Blockbuster hit Moana 2 helped drive The Walt Disney Company (DIS) to beat quarterly profit expectations amid a resurgence in studio successes, even as the company started to lose Disney+ streaming customers.

DIS posted Fiscal first quarter earnings on Wednesday that topped Wall Street forecasts, with adjusted earnings per share (EPS) rising 44% to $1.76 versus the $1.46 expected. Revenues rose 5% to hit $24.69 billion vs. $24.62 billion expected. Shares rose about 1% in pre-market trading.

However, the company saw a 1% decline in subscribers to its flagship Disney+ streaming platform. Total paid Disney+ subscriptions fell to 124.6 million from 125.3 million over the quarter, though Hulu subscriptions rose 3% during the period to 53.6 million.

Disney also warned that it expects another “modest decline” in Disney+ subscribers during the second quarter. More positively, price hikes helped the average monthly revenue per paid subscriber increase 4% to $7.99.

DIS Earnings Driven by Films as Parks Take Weather Hit

Operating income at its Entertainment division rose $800 million to $1.7 billion, with a significant contribution from Moana 2 during the quarter as revenues rose 9% to $10.87 billion.

Moana 2 became Disney’s third 2024 release to exceed $1 billion at the box office, joining Inside Out 2 and Deadpool & Wolverine in the club and capping a record year for the studio as audiences at last returned to theaters in meaningful numbers.

However, domestic theme park operating income within the Experiences segment declined 5% as it took a $120 million hit from hurricanes Helene and Milton in Florida. International Parks and Experiences operating income increased 28% from a year ago.

Ahead of the Superbowl, sports is also delivering well, with domestic ESPN advertising revenue up 15% from Q1 Fiscal 2024.

DIS Fiscal 2025 Outlook Positive

For Fiscal 2025, DIS expects high single digit adjusted EPS growth, within which Entertainment is set to deliver “double-digit percentage segment operating income growth.” It anticipates operating income at its Direct-to-Consumer business, which includes the Disney+ platform, to be $875 million. Sports should grow about 13% and Experiences, which includes theme parks, is set to grow 6-8%.

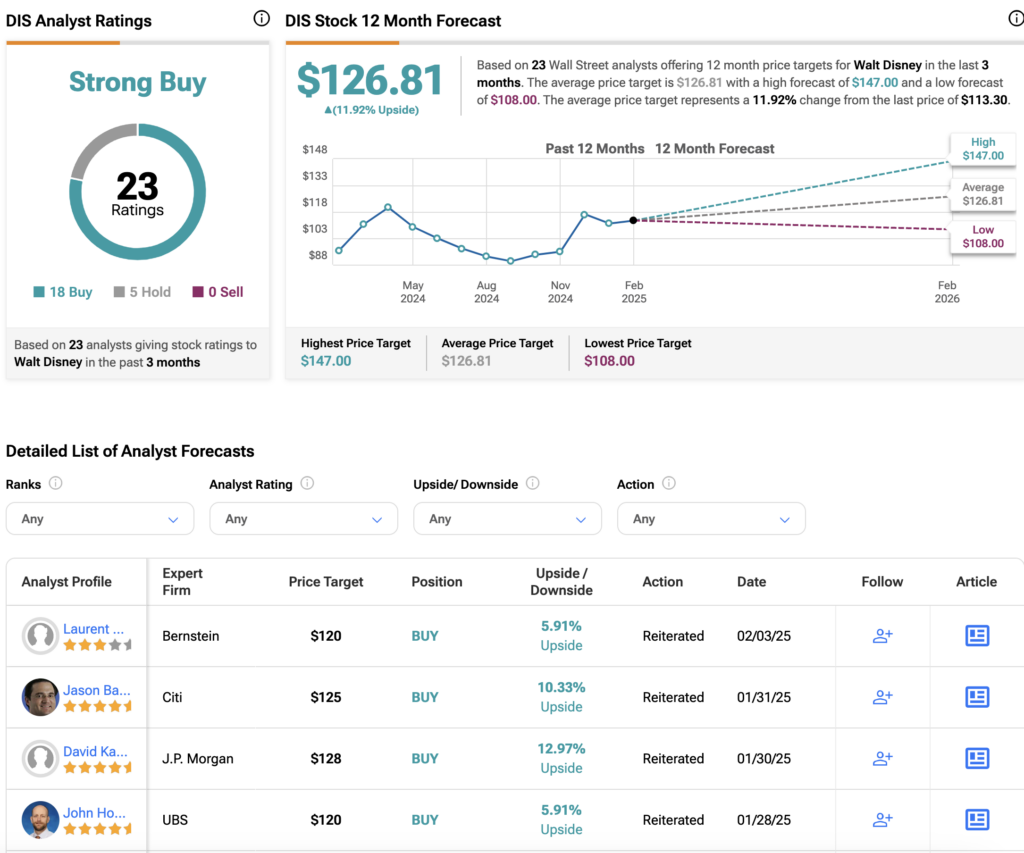

Is DIS a Good Stock to Buy?

Overall, Wall Street has a Strong Buy consensus rating on DIS stock, based on 18 Buys and five Holds. The average DIS price target of $126.81 implies about 12% upside.