The odds might not be in favor of Chinese tech behemoth Alibaba (NYSE:BABA) right now, but the tides may turn soon. Its recent $1 billion investment in its cloud business might help Alibaba balance the e-commerce woes until the latter gets back on its feet again.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Given that over the past few years, Alibaba’s cloud business has quickly emerged as a major revenue driver, emphasis on this business may help solve some problems for the company. It is worth noting here that Alibaba Cloud was the world’s third-largest provider of public cloud service, as of 2021.

Alibaba’s Billion-Dollar Resurrection Plan

Alibaba recently pledged $1 billion for a “global partner ecosystem upgrade,” which involves funding the technological innovations of global partners handling the sales, tech support, and customer service areas of the company’s worldwide cloud business. This may help uplift the thriving business, which is facing some headwinds currently.

The growing national security trust issues between China and the U.S. have driven several customers away from the Alibaba Cloud in favor of foreign servers. Even the Chinese short-video posting platform TikTok moved its data to Oracle servers to avoid regulatory scrutiny in the future. This makes us think that the investment might have been part of Alibaba’s efforts to retain its existing partners and even attract more partnerships and adoption.

The threat to Alibaba’s footing in the global cloud market can be mitigated via this investment. Importantly, Alibaba Cloud’s 11,000-strong partner roster includes U.S. tech giants Salesforce (NYSE:CRM), VMware (NYSE:VMW), Fortinet (NASDAQ:FTNT), and IBM (NYSE:IBM). This gives us a deeper insight into why Alibaba needs to up the ante in partner retention efforts.

Additionally, current trends in Alibaba’s core e-commerce business are not so encouraging. Overall, consumer demand has slowed considerably and is expected to remain so for some time. So far this year, Alibaba’s shares have lost 33%. Multiple headwinds played a part in the decline, including China’s zero-tolerance policy to control the resurgence of COVID, inflation, trade hostilities with the U.S., fear of getting delisted along with other Chinese stocks, etc.

Even now, the outlook for China’s economic growth is dim. Goldman Sachs recently sharply trimmed its 2023 growth forecast for China to 4.5% from 5.3%, citing continued COVID-Zero policies in Beijing at least until the first quarter of 2023 ends.

Therefore, the next best thing for Alibaba to do is take its cloud business up a notch to balance the weakness in e-commerce. To that end, the investment may be a great stepping stone. Although the company heavily relies on its e-commerce business for revenues, a meaningful and growing part of its revenues comes from its huge cloud business, which has managed to compete for head-on with the likes of Amazon (NASDAQ: AMZN) and Microsoft (NASDAQ:MSFT).

Is it Safe to Buy Alibaba?

All things said, Alibaba is a safe investment option.

Alibaba’s three retail segments contribute more than 50% of overall retail sales in the vast economy of China. So, as the economy recovers (which it will, like it does after every market cycle), this part of the business should be the first to rise.

Moreover, the global $1 billion cloud program is expected to boost its footing in the global cloud market. Interestingly, the global cloud computing market is still growing and is expected to reach $480.04 billion by the end of this year, according to Fortune Business Insights. Remarkably, by 2029, this number is likely to increase to $1.712 trillion. Alibaba’s stronghold is only going to get stronger with efforts like these.

Also, even if the stock runs the risk of getting delisted from the NYSE, investors will be given a chance to cash out, so that shouldn’t be a worry.

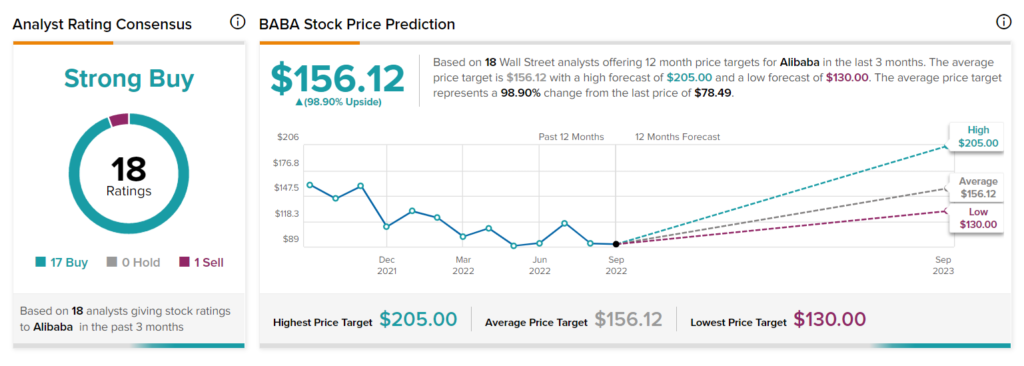

What is the Target Price for BABA Stock?

Wall Street analysts are bullish on BABA, with a Strong Buy consensus rating based on 17 Buys and one Sell. The average price target stands at $156.12 currently, which means it still has room for growth by about 99%.

Footnote: This Could Be a Great Time to Buy Alibaba

Various upsides can be seen which can drive Alibaba’s long-term trajectory, like market dominance and economic recovery in China.

Moreover, the company’s current valuation is around 44.5x trailing 12-month earnings, which is significantly below its 5-year high of 67.6x, which it achieved in July this year.

These call for some serious consideration from investors without any recent bias to accumulate shares of BABA.