Tesla (NASDAQ: TSLA) may not be doing so well in China even as its sales soared 18% month-over-month in January. Last year, TSLA slashed its prices in China twice.

Stay Ahead of the Market:

- Discover outperforming stocks and invest smarter with Top Smart Score Stocks

- Filter, analyze, and streamline your search for investment opportunities using Tipranks' Stock Screener

Even with the higher sales in China, it is widely believed that the EV major has lagged behind its Chinese competitors when it comes to the introduction of new models in this market, improvement in its navigation systems, and the addition of luxury interior touches.

In a bid to change this, TSLA recently halted production temporarily at its plant in Shanghai to make production upgrades and roll out a revamped Model 3 in China. The company aims to produce 20,000 vehicles per week at its Shanghai factory in March.

But will these measures be enough to take over its Chinese competitors? As Elon Musk, Tesla’s Founder and CEO admitted on its Q4 earnings call that the Chinese market was the “most competitive in the world.”

According to a Reuters report, citing data from the China Passenger Car Association (CPCA), Tesla’s market share is eroding – from 15% in 2020 to just 10% last year. This loss of market share is not because of falling demand for EVs. On the contrary, the Chinese Association of Automobile Manufacturers has projected sales of EVs and plug-in hybrids to surge by 35% this year to 9 million vehicles, representing around 33% of the country’s total new vehicle sales.

Chinese Peers are Overtaking Tesla

Among Tesla’s Chinese competitors, the Warren Buffet-backed BYD (BYDDY) has been the most formidable one. The company delivered the second-best vehicle delivery numbers in China in January after Tesla as sales soared 62.4% year-over-year.

BYD has already overtaken TSLA in terms of global volumes and currently has around 60 different versions of EV and plug-in hybrid cars.

As Charlie Munger told CNBC, “Tesla last year reduced its prices in China twice. BYD increased its prices. We are direct competitors. BYD is so much ahead of Tesla in China … it’s almost ridiculous.”

Indeed, BYD expects to report an adjusted annual profit for FY22 of $2.4 billion, a massive jump of 1,200% over FY21.

When it comes to TSLA’s navigation systems, there have been reports that these systems have been slow to update and not entirely free of errors on Chinese roads.

As a Chinese auto blogger, Chang Yan told Reuters, “This is a sharp contrast with Nio, (EV brands) Xpeng and Li Auto, whose navigation aids have been working almost perfectly.”

This is also echoed by these Chinese EV companies’ January numbers as except for Li Auto (LI), both XPeng (XPEV) and NIO (NIO) saw a jump in vehicle deliveries.

Analyst Gordon Johnson of GLJ Research is not gung-ho about TSLA’s prospects in China either. The analyst is bearish about the stock with a Sell rating with a price target of $73. Johnson’s price target implies a downside potential of 65.9% at current levels.

The analyst pointed out that TSLA sold just 6,963 thousand cars in China in the week between February 6 to February 12 – only 39% of around 17,734 thousand vehicles produced by the company every week in Shanghai in January.

Accordingly, Johnson sees Tesla’s Q1 sales in China down by 25.8% quarter-on-quarter to around 90,000 units, well below the consensus estimates of around 129,000 units.

The analyst commented, “Stated more clearly, should TSLA’s 1Q23 domestic China sales come in below and/or around 100K, as the data currently suggests it will, we believe the stock would come under acute selling pressure.”

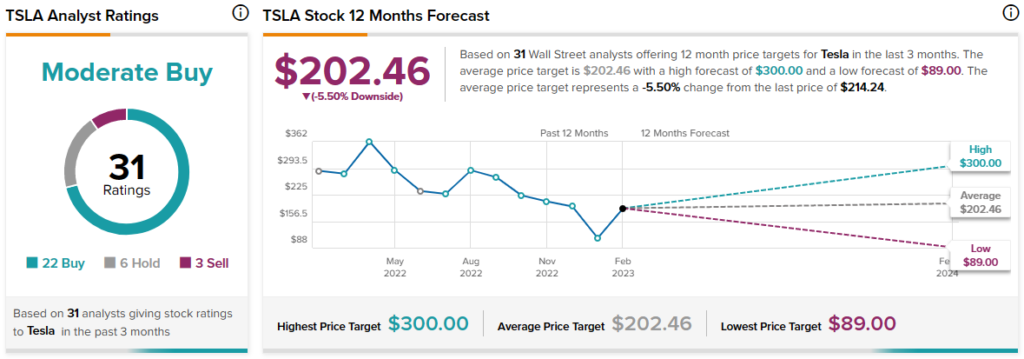

Barring Johnson, other analysts remain cautiously optimistic about TSLA stock with a Moderate Buy consensus rating based on 22 Buys, six Holds and three Sells.