NIO (NIO) stock has lost almost half of its value over the past 12 months and remains quite volatile. The business remains loss-making, and its path to profitability isn’t clear, given the company’s fairly unstable trajectory and investment in new business units. Personally, I’m bearish on NIO stock. The sector is increasingly competitive and the smart money already appears to have moved to automation. I’m also uncertain about the future of battery-swapping technology.

Confident Investing Starts Here:

- Easily unpack a company's performance with TipRanks' new KPI Data for smart investment decisions

- Receive undervalued, market resilient stocks straight to you inbox with TipRanks' Smart Value Newsletter

Let’s Start with NIO’s Positives

While I remain bearish on NIO stock, it would be remiss of me not to recognize the company’s recent progress. NIO’s Q4 2024 delivery figures highlighted record-breaking results that address concerns about average selling prices (ASP) and sub-brand margin accretion. The company delivered 72,689 vehicles in Q4, including a monthly record of 31,138 vehicles in December. There was also a recovery in NIO’s core brand deliveries, reaching 20,610 units in December. This resurgence suggests that sales have stabilized to some extent, potentially leading to improved ASPs and revenue growth.

The introduction of the premium ET9 sedan, priced at RMB 788,000 (~$108,000) with deliveries starting in March 2025, is expected to further boost ASPs. The limited “First Edition” trim, priced at RMB 818,000, has already sold out its 999 units, indicating strong demand for NIO’s high-end offerings, with some billing the car as China’s answer to the S-Class.

Meanwhile, ONVO, NIO’s sub-brand, recorded more strong growth with 10,528 L60 deliveries in December, representing a 107% month-over-month increase. This rapid ramp-up suggests that previous battery supply bottlenecks have been largely resolved, allowing NIO to capitalize on demand and fulfill pre-orders efficiently. With the above progress in mind, 2025 could certainly be a better year for the company and may represent something of a turnaround.

NIO Operates in a Competitive Market

However, I believe there are several reasons for bearishness, starting with the increasing competitiveness of the sector. The premium segment, where NIO has traditionally focused, is becoming more crowded as traditional automakers enter the EV space. However, the lower-priced market segment is even more fiercely competitive, with companies like BYD (BYDDF) and Tesla (TSLA) aggressively cutting prices to gain market share.

The competition in the lower-priced segment could intensify further if Tesla introduces its rumored Model Q, a more affordable EV aimed at the mass market. This potential move by Tesla could put additional pressure on NIO’s newly launched sub-brand ONVO, which targets the more affordable EV segment. After all, Tesla has been one of the main instigators of pricing pressure in recent years.

NIO’s Infrastructure Headache

Another reason for my bearishness is NIO’s battery-swapping technology, which I once perceived as a real selling point. Today, I believe NIO faces noteworthy infrastructure challenges as it expands its battery-swapping network. The construction of battery swap stations is costly, with estimates ranging from RMB 1 million to 3 million ($160,000 to $470,000) per station.

While these battery-swapping stations will eventually be a revenue-generating asset, building these stations represents a substantial investment that inevitably slows NIO’s expansion into new markets, as the company must carefully balance the deployment of stations with market demand.

Moreover, while battery swapping offers advantages like rapid energy replenishment, I wonder whether the technology faces potential obsolescence as fast charging capabilities improve. With advancements in charging technology, the time difference between swapping and fast charging is narrowing. This trend could potentially render battery swapping less attractive in the long term, especially considering the high costs associated with building and maintaining swap stations.

NIO’s Valuation Doesn’t Scream Cheap

However, core to my bearishness is the valuation. Despite NIO’s recent stock price decline, its valuation metrics suggest it’s not particularly cheap compared to its peers, especially Chinese EV makers. NIO’s Price-to-Sales (P/S) ratio of 1.02 and Enterprise Value-to-Sales (EV/Sales) ratio of 1.11 are higher than those of Li Auto (LI) and BYD — both of which have stronger financial positions.

While NIO’s valuation is lower than XPeng (XPEV) and VinFast (VFS), it’s still not trading at attractive multiples. While Tesla trades at much higher multiples, it’s profitable, has a stronger market position, and is valued according to its potential in artificial intelligence and robotics.

Is NIO Stock a Buy According to Analysts?

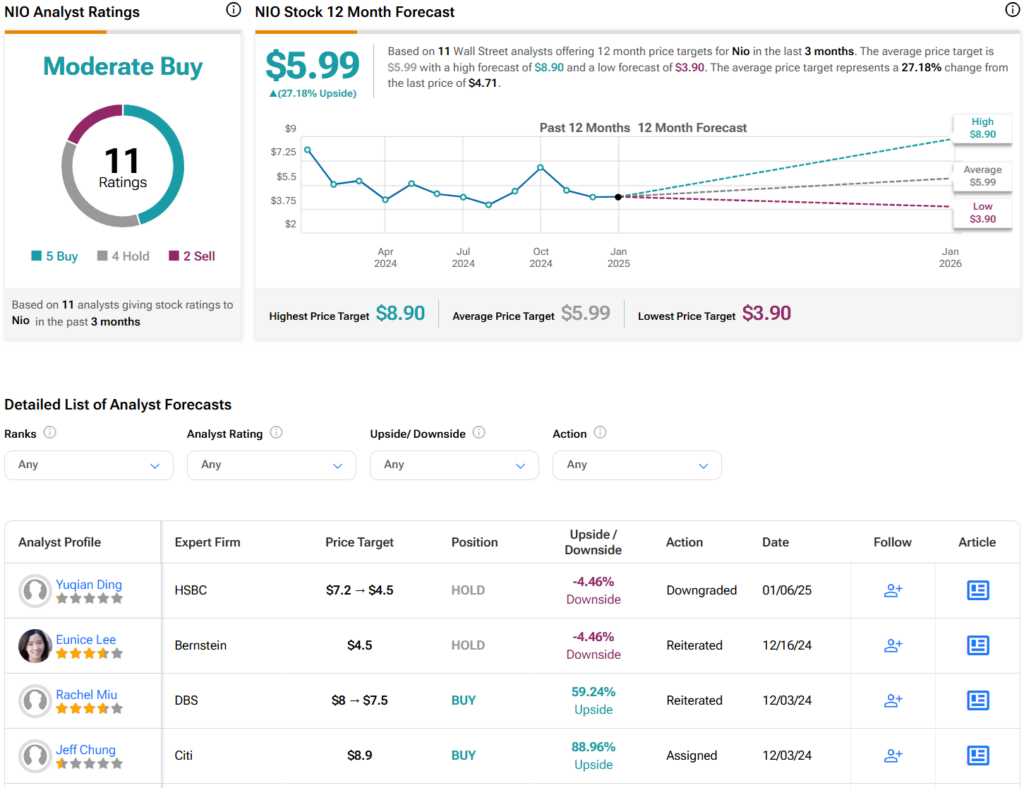

On TipRanks, NIO comes in as a Moderate Buy based on five Buys, four Holds, and two Sells assigned by analysts in the past three months. The average NIO stock price target is $5.99, implying about 27.8% upside potential.

The Bottom Line on NIO Stock

I’m bearish on NIO stock despite its recent progress in deliveries and product launches. While 2025 might bring some recovery, the company’s challenges—including fierce competition, battery-swapping infrastructure costs, and valuation concerns—remain significant. The EV market’s rapid evolution, with advancements in fast charging and price cuts by rivals, puts additional pressure on NIO’s business model. Without a clear path to profitability or a sustainable competitive edge, I find it difficult to justify an investment in NIO at current levels.