Prior to the roughly month-long recovery posted by the major equity indices, most sectors suffered significant losses. However, a dark cloud hung over Vroom (VRM) and other companies in the auto dealership market. With soaring inflation combined with global supply chain woes imposing sharp headwinds, Vroom, in particular, suffers a credibility crisis for its higher convenience premium. Therefore, I am bearish on VRM stock.

As a whole, the primary issue with Vroom is that as a mostly online-interfacing company, it must pass down the costs of its convenience factor to the customer. During the COVID-19 crisis, people were more than willing to pay this convenience premium because the threat of infection presented a far greater threat. Now that the current epidemic is monetary inflation, people are far less willing to support discretionary premiums.

Nevertheless, Vroom has done well to reinvigorate speculators’ interest. Mainly, the company posted contextually decent figures for its second quarter of 2022 earnings report. As TipRanks contributor Steve Anderson pointed out, the “results were better than expected in some slots.” In particular, the “good news for Vroom was that it did manage to beat consensus expectations for earnings.”

However, Anderson was also quick to point out that the company “still generated plenty of disappointment.” As he put it, revenue fell short of expectations. “The company posted $475.44 million in revenue for the quarter, which was 37.6% below the consensus estimate. The issues facing Vroom were felt throughout the used car market; CarGurus (CARG) is also down 23% [on Aug. 9, 2022] after reporting earnings.”

To be fair, VRM stock gained a blistering 35% during the past month. For comparison, the Nasdaq Composite index gained 14.5% during the same period. Still, investors should be very cautious about piling into this trade.

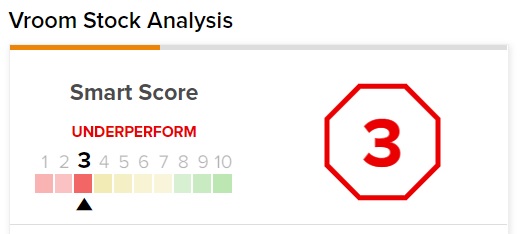

Vroom Stock Analysis

On TipRanks, VRM has a 3 out of 10 Smart Score rating. This indicates the potential for the stock to underperform the broader market.

VRM Stock is a Victim of the Trade-Down Effect

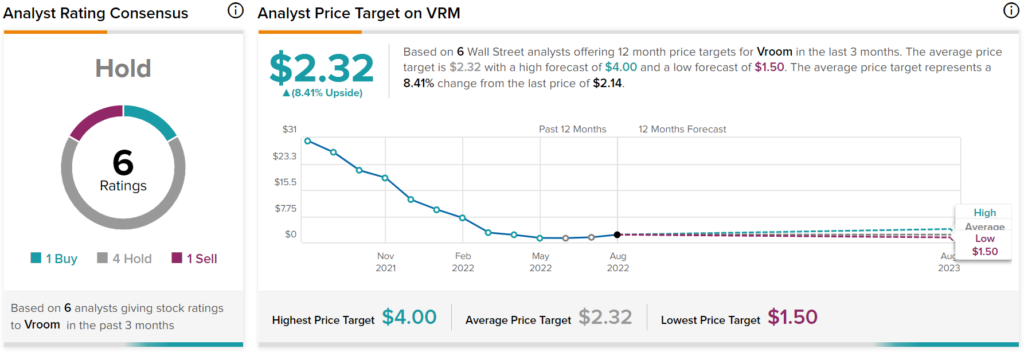

Under a blossoming economy – or one faced with a severe health crisis like COVID-19 – the consensus narrative could be a lot different than it is right now. For instance, Stifel Nicolaus analyst Scott Devitt assigned a Hold rating to VRM stock while setting a per-share price target of $1.50. As of this writing, VRM is priced at $2.14. Part of the reason for the pessimism could be the trade-down effect.

Essentially, as household incomes become pressured – either through layoffs or in the current context of a reduction in purchasing power – consumers don’t always go cold turkey with their purchasing behaviors. Instead, if the option presents itself, people will sacrifice the quality of the underlying goods or services before cutting them altogether.

To use a basic example, people who buy discretionary items through membership-only retailers like Costco (COST) could trade down to non-membership entities like Target (TGT). Should economic pressures sustain, they might trade down again to Walmart (WMT). Should circumstances continue to worsen, these same consumers could end up at discount retailers like Dollar Tree (DLTR).

Unfortunately, Vroom operates at the top end of the trade-down spectrum. With the economy’s long-term viability still questionable, and inflation cutting a major chunk out of household savings, consumers are much more likely to trade down from Vroom’s services to cheaper options. These include CarMax (KMX), independent used-car dealerships, or even a private party.

When it comes to fees, Vroom’s charge depends on where the customer is located. Sadly, this framework is problematic when people can just opt for the traditional option to purchase their next vehicle.

Used Cars are Still Relevant

Although it’s tempting to criticize all car dealerships – particularly those that specialize in used vehicles – as problematic under the present economic environment, that might not be the case. Two critical factors bolster the idea of used cars; they just don’t particularly bode well for VRM stock.

First, as I mentioned in July regarding the bull case for CarMax, per Statista’s Global Consumer Survey, “76% of American commuters use their own vehicles to move between home and work. Should the professional environment normalize and the grand work-from-home experiment fade out, this stat could fundamentally rise in favor of KMX stock. Logically, the more cars on the road, the better the outlook for CarMax.”

“Further, The Wall Street Journal provided what may be the biggest – though perhaps underappreciated – catalyst for the used-car market. It reported that the average age of vehicles on U.S. roadways hit a record 12.2 years, translating to drivers holding onto their rides for as long as possible to avoid costly replacements.”

Still, once a car breaks down, in many cases, outright replacement may be economically superior to throwing precious funds at a vehicular money pit. Therefore, used cars are still relevant. However, analysts may not have the same confidence to say that about VRM stock.

To bring home the argument, just look at Vroom’s operating margin on a trailing-12-month basis. Currently, it stands at a moribund 13.3% below breakeven. In sharp contrast, CarMax’s operating margin is 0.91% during the same period.

No, CarMax is hardly an operating margin king. However, it’s in positive territory, which speaks to the challenges facing Vroom’s business model.

Is VRM Stock a Buy or Sell?

Turning to Wall Street, VRM stock has a Hold consensus rating based on one Buy, four Holds, and one Sell assigned in the past three months. The average VRM price target is $2.32, implying 8.4% upside potential.

Takeaway – VRM Stock is Too Risky for the Current Environment

Even without the fiscal challenges facing VRM stock – such as negative operating margins – Vroom still must contend with the fundamental reality that it’s on the unfavorable end of the trade-down effect. Should the economy improve so that consumers start trading up, then perhaps analysts will have a different discussion. Until then, be careful and be skeptical about VRM.