Crises can have unexpected impacts, something we are seeing clearly today as combination of critical situations are hitting hard at a long-established order (think generationally high inflation and the Russo-Ukraine war). But the impacts aren’t always as violent, even when the effects are long-lasting.

Don't Miss Our New Year's Offers:

- Discover the latest stocks recommended by top Wall Street analysts, all in one place with Analyst Top Stocks

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

At the height of the 2008 financial crisis, we heard plenty of talk about ‘too big to fail,’ the reasoning given for bailing out huge banking firms. The public outcry is still reverberating in our politics. But it made a bigger, if somewhat quieter splash, in the banking and financial tech realms, with the rise of challenger banks.

These are smaller banking firms, typically rising from the fintech niche, and set up to purposefully challenge the established banking order. The challengers are typically smaller retail banks, with a strong B2C consumer orientation, offering a range of services to customers who may not qualify for banking options via the large, established banks. It’s not uncommon for these challenger to operate mainly via website or app.

In short, the challenger banks have been shaking up the banking industry for the better part of a decade now.

But are current conditions in the banking industry ripe for challenger banks to boom? Analyst Sean Horgan, of Rosenblatt Securities, believes so.

“Our long-term investment thesis for challenger banks has not changed. Incumbent traditional banks are paying ~10x to acquire new customers, leaving challenger banks with a critical cost advantage. Nevertheless, with a renewed sense of show-me-the-money sentiment, the chessboard has been reconfigured. Investors in 2022 appear positioned to reward those who demonstrate a path to profitability as opposed to revenue growth,” Horgan explained.

The immediate bump for the challenger banks, post-COVID, was a resurgence of consumer spending and low interest rates. While these factors are starting to recede, it’s worth taking a look at some of Horgan’s stock picks in this fintech space as examples of just how challenger banks can adapt to meet the changing conditions. We’ve used the TipRanks platform to pull up the details on two of them, which Horgan sees in particularly strong positions for long-term gains.

SoFi Technologies (SOFI)

We’ll start with SoFi Technologies, a San Francisco-based company operating in the personal finance sector. ‘SoFi’ is an abbreviation for Social Finance, and is an accurate description of the company’s approach to banking services. SoFi offers its services online, and boasts 3.5 million members, $59 billion in funded loans, and more than $100 million stored in physical vaults. Among the services offered home and personal loans, credit cards, refinancing for student and auto loans, credit scoring and budgeting, and investments.

SoFi entered the public markets last summer, ten years after its 2011 founding, through a SPAC transaction. The business combination, with Social Capital Hedosophia V, was completed at the end of May and SOFI started trading on the NASDAQ on June 1. Since then, the stock has been highly volatile, with extensive swings both up and down. It is currently down 60% from its initial trading price, and year-to-date has fallen 44%.

Earlier this year, SoFi acquired the digital banking platform Technisys. The move was completed in early March, and involved a transfer of 84 million shares of stock valued at approximately $1.1 billion. Technisys brings a strategic technology stack to SoFi, which estimates that the acquisition will bring between $500 and $800 million in value through 2025.

On March 1, SoFi reported its financial results for 4Q21. This is the third such report since the SPAC. SoFi reported GAAP revenues of $286 million for the quarter, up 67% year-over-year, and perhaps more importantly, reported new-member add of 523,000 in Q4. This was a 39% sequential gain. SoFi has also been working hard on increasing brand exposure, expanding its stadium affiliation, as well as marketing and influencer campaigns.

Looking ahead, management sees some headwinds in 1Q22, including ‘the unexpected extension of the federal student loan payment moratorium to May 1, 2022.’ Overall, however, the company expects to see strong revenue gains in 2022 – but mostly back-end loaded, stronger in the second half than the first. For Q1, SoFi has guided toward $280 million and $285 million at the top line; for the full year, the number expands to $1.57 billion. Among the long-term supports to this view are the January approval of SoFi’s bank charter and its recent acquisition of Golden Pacific Bancorp.

The full-year guidance “inspires confidence,” says Rosenblatt’s Horgan. “Results came in largely as expected, with notable progress on customer acquisition likely surprising to the upside… While we expect consensus to move higher, we also note that we believe there is a reasonable level of conservatism in the guidance, particularly as it relates to the impact of the bank charter benefits and the Technisys acquisition.”

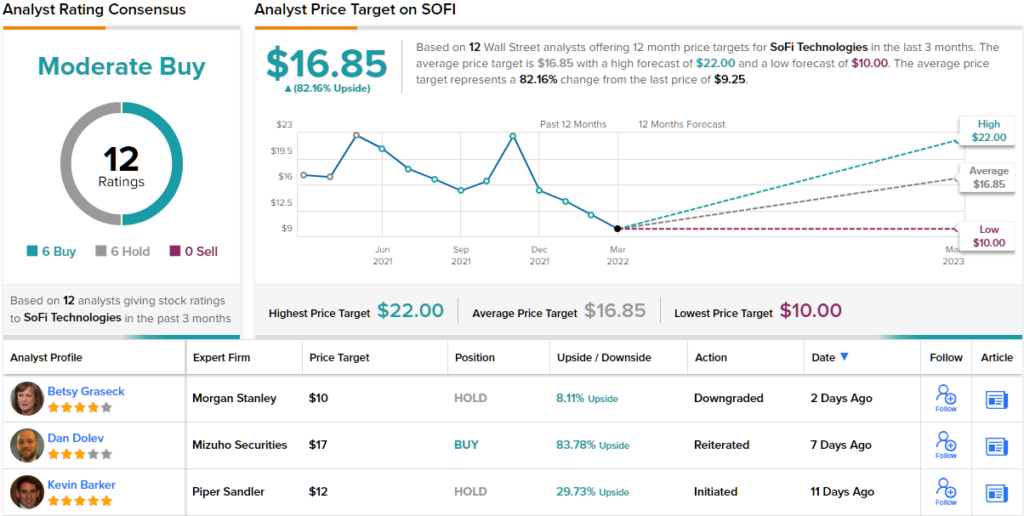

In line with these comments, Horgan rates SoFi shares a Buy, along with a $22 price target. The analyst, therefore, expects the stock to climb 138% over the coming months. (To watch Horgan’s track record, click here)

While Horgan is bullish on SoFi, Wall Street generally is evenly split. The stock has 12 reviews including 6 to Buy and 6 to Hold, for a Moderate Buy consensus view. With an average price target of $16.85, SOFI has ~82% one-year upside from current levels. (See SoFi stock analysis on TipRanks)

MoneyLion (ML)

The second stock we’ll look at is MoneyLion, a financial tech platform in the personal banking sector – in other words, the very definition of a challenger bank. MoneyLion was founded in 2013, and targets its operations to retail customers. The company describes itself as ‘banking with a safety net,’ and offers customers deposit services, cash access, and loans, all available online with control of the services managed in one place, through an app. MoneyLion has engaged with some 9.4 million people, and boasts that it has saved its customers a cumulative $250 million in banking fees.

That’s the positive side. In a setback for the company, MoneyLion suffered a ‘credential stuffing’ attack last summer, a serious security breach attempt to access customers’ private data, and took several ameliorative actions. Addressing the issue, MoneyLion implemented security improvements on customer access, including multi-factor authentication.

The company dealt with the security issue, and then felt the confidence to go public. The ML ticker started trading on September 23 last year, after completion of a SPAC merger with Fusion Acquisition Corporation, in a deal that brought the online bank approximately $526 million in net cash proceeds.

The stock started trading at $8.63, and has been falling steadily since that time. ML shares are down 70% since the SPAC merger, having been buffeted by both the credential stuffing attack and the general market downturn at the start of this year.

Earlier this month, MoneyLion reported its 4Q21 and full-year financial results, and there are some important takeaways. Quarterly net revenue came in at $55.5 million, with the full-year number at $171.1 million. These were up 146% and 115%, respectively, year-over-year, and indicate strong, accelerating growth. That is confirmed by the company’s customer growth; MoneyLion reported 3.3 million customers at the end of 2021, for a y/y gain of 129%. This triple-digit growth has the company expecting to reach break-even status by the end of 2022.

In his note on MoneyLion, Sean Horgan says simply, “Now is the time to put ML on your radar for a potential 4:1 risk/reward opportunity. We don’t expect shares to get much lower than $2-$3, certainly not by year-end 2022, and recommend investors (who can tolerate ST volatility) accumulate at current levels.” Elaborating, he adds, “The path to profitability is in sight, with breakeven EBITDA guided by year-end ’22 and meaningful profitability by mid-year ’23…”

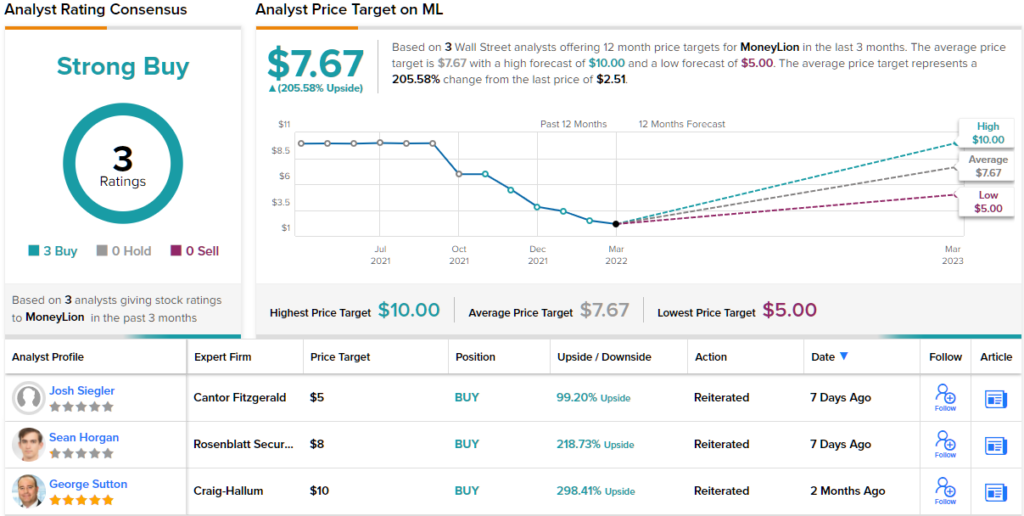

These comments support Horgan’s Buy rating here, while his $8 price target suggests a one-year upside potential of 219%. (To watch Horgan’s track record, click here)

While MoneyLion has seen its share of headwinds, the Street believes that the stock has potential. ML shares have a Strong Buy consensus rating, based on a unanimous 3 reviews, and the $7.67 average price target implies ~206% upside from the share price of $2.51. (See MoneyLion’s stock analysis at TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.