Shares of personal finance fintech SoFi Technologies (SOFI) have been a painful ride for investors over the past year, now down more than 75% off their all-time high of around $25 per share. Undoubtedly, the rate-induced market sell-off has hurt unprofitable small-cap firms the most. Though SoFi is one of the most forward-thinking financial technology companies out there, it’s hard to draw a line in the sand after its recent valuation reset. For that reason, I am neutral on SOFI stock.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

SoFi Stock: Neobank Versus Old-School Banks

Neobank SoFi has come a long way from its days as a refinancer of student loans. The firm is ready to expand its footprint in the realm of financial services, even if it means clashing swords with some of the biggest financial institutions in the country. With rates on the rise, the tables seem to be tilted back in favor of the traditional, old-school financial institutions with big balance sheets. Further, SoFi and other fintechs may find themselves being out-innovated by the big banks as they push to adapt to the times.

The big banks have deep pockets, and many have not shied away from innovative projects.

Goldman Sachs (GS) is an old-school financial institution that helped the Apple (AAPL) Card come to be. Arguably, the Apple Card is one of the most innovative credit cards on the market, with a wealth of digital features and functionality for users of Apple’s iOS operating system.

SoFi’s acquisition of a national bank charter opens new windows of opportunity for the firm to expand its services. As a neobank, SoFi is an intriguing play that may gain a bit of an edge over its fintech rivals, as it can keep deposits to make a deeper dive into the loan business.

In any case, bank stocks don’t tend to boast the highest multiples in the world, and until SoFi can produce a sustained profit, it may be viewed as a less worthy bank through the eyes of investors. Profitability prospects matter, and as rates rise, fewer investors will be willing to pay up for growth. In a market full of profitable old-school banks, why take the risk on a neobank that may not make a profitable push until years down the road?

In an environment where credit is easy, I see the case for owning SoFi stock over the big banks. However, given the trajectory of rates, it’s tough to tell if SoFi will be able to beckon investors back into the name without truly cutting-edge features that its rivals can’t easily replicate.

In terms of cutting-edge features, I’m not talking about Buy Now, Pay Later (BNPL), a financial trend that’s since lost its luster. SoFi needs to stay on its toes and reinvest considerable sums to continue taking meaningful market share away from rivals.

SoFi Could Clash With Goldman Sachs in Retail Banking

Goldman Sachs has its own share of retail-banking ambitions under its Marcus banner. Goldman is an investment banking heavyweight that’s catered to the most affluent of individuals for many years. It’s a relative newcomer to retail banking. Like SoFi, Goldman seeks young professionals in the higher-income range and tries to leverage tech in its favor to gain market share.

Though Goldman and SoFi couldn’t be more different, they seem to be targeting the same market. Currently, SoFi appears to have the technological advantage with its convenient app that offers a wide range of services. SoFi is also hanging onto the many young, loyal customers that used it to pay off student loans.

Goldman has the brand name in its favor and a foot in the door with tech titan Apple. With rumors swirling around partnerships beyond the Apple Card, Goldman may be the more enticing retail-banking newcomer.

SoFi Beats on Q2 Earnings

In the second quarter, SoFi saw net revenue soar 57% to $362.5 million. Per-share losses of $0.12 came in a penny higher than the $0.13 loss estimate. Powering SoFi’s quarter was strength in personal loans. Net interest income also surged 101% year-over-year to around $114 million.

SoFi is still very much on the growth track. However, such growth will require the firm to continue racking up lofty expenses over time. With a bank charter in hand, SoFi can leverage its own technologies to evaluate credit risk. As SoFi ramps up its loan business, there’s a real chance that it may be able to outdo traditional banks in loans if its tech proves superior at gauging creditworthiness.

With a third straight quarter of almost in-line earnings in the rear-view mirror, SoFi stock is starting to look intriguing after its flop. Shares of the neobank trade at 5.6 times sales, making it cheaper than many no-growth stalwarts out there.

Personally, I think the negativity is a tad overblown, but SoFi is likely to be up against it as the Federal Reserve continues to raise interest rates in a bid to reduce inflation.

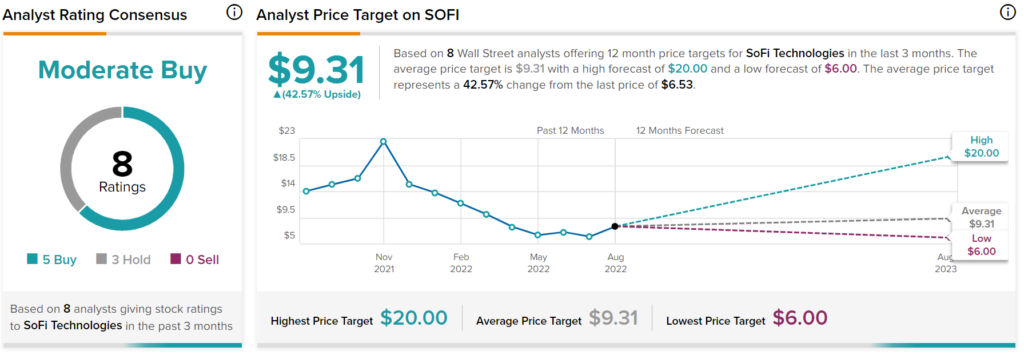

What is the Price Target for SoFi Stock?

SoFi has a Moderate Buy consensus rating based on five Buys, three Holds, and zero Sells assigned in the past three months. The average SOFI stock price target of $9.31 implies 42.6% upside potential. Analyst price targets range from a low of $6.00 per share to a high of $20.00 per share.

Takeaway – SOFI is Innovative, but Competition is Fierce

SoFi is a very unique fintech stock with ambitious plans. The risks are high, given stiff competition from the likes of the big banks. However, so too are the rewards, as the firm looks to change banking with an innovation-first mindset.