Investors are once again becoming increasingly wary of retail REITs. This is due to the ongoing macroeconomic turmoil, which is assumed to lessen consumers’ purchasing power, thus softening the overall foot traffic in retail properties. That said, Acadia Realty Trust (NYSE:AKR) seems to be delivering good results. Its 4.6% dividend yield appears enticing when considering there is room for the dividend to grow from here. However, I am neutral on the stock, as my appetite for the space remains apathetic.

Can Acadia’s Recovery Momentum Continue?

Investors have lately become increasingly wary that Acadia’s post-pandemic recovery may be short-lived. However, as the company’s latest results showed, Acadia’s positive trajectory remains solid. In fact, Acadia closed the first half of Fiscal Year 2022 by delivering better-than-expected results. In Q2, Acadia’s revenues came in at $84.3 million, an increase of 12.9% compared to last year. This fine increase was due to Acadia’s retail locations still being affected by limitations related to COVID-19 in Q2 2021.

Further, Acadia’s Core Portfolio recorded a 4.8% and a 7.1% gain sequentially and year-to-date in same-property NOI (Net Operating Income), respectively. This was driven by rent commencements on new leases and healthier credit conditions.

Other positive KPIs include Acadia’s Core Portfolio occupancy and leasing rates, which stood at 90.5% and 94.1% at the quarter-end, respectively, remaining stable quarter-over-quarter despite the recent concerns. After all, it’s worth noting that consumer spending in the U.S. hit another all-time high in the second quarter of 2022.

Management remains relatively confident in the company’s expansion strategy, as proven by the continuous development of Acadia’s Fund platform. Specifically, during the three-month-period, Acadia’s Fund platform completed $85 million worth of acquisitions while its acquisition pipeline stayed vigorous.

Further, FFO came in at $23.4 million ($0.23 per share) and included an $8.9 million ($0.09 per share) unrealized mark-to-market loss on Albertsons. This compares with an FFO of $28.1 million, or $0.30 per share, in Q2 2021. Thus, excluding the one-off effect from Albertsons, FFO/share actually grew year-over-year.

Amid a better-than-expected performance, management boosted its FFO per share outlook for Fiscal Year 2022. The company now forecasts that FFO/share will land between $1.20 and $1.32 for the full year, up from 1.17 to $1.32 previously.

AKR Stock’s Dividend Should Grow from Here

Acadia has a relatively shaky dividend track record. The company initially slashed its quarterly dividend from $0.21 to $0.18 during the Great Financial Crisis. Then, Acadia began to grow payouts gradually all the way to 2020, when the dividend-per-share advanced to $0.29. Then COVID-19 arrived, and the impact of the pandemic resulted in Acadia once again being forced to slash the dividend. However, Acadia has started to increase its dividend again, as was the case following the previous recession.

Last February, the quarterly dividend was increased by 20%, from $0.15 to $0.18. While it’s still at similar levels to 2009 and 2012, it’s certainly a step in the right direction.

When using the midpoint of management’s FFO/share outlook of roughly $1.26 and the present dividend-per-share run-rate of $0.72, the payout ratio stands at a somewhat comfortable 57%. Therefore, it’s entirely possible that bold dividend hikes similar to last February’s hike could prevail over the next few years.

Overall, there are both positive and negative factors that could affect Acadia’s dividend growth prospects. On the one hand, dividend growth should be supported by strong leasing activity.

On the other hand, retail REITs are likely to encounter headwinds if the macroeconomic landscape stays tense and occupancy levels remain below optimal levels. Still, based on the current data, it appears that Acadia’s dividend should only grow from its current place.

In any case, investors should not expect that the company’s pre-COVID payout levels ($0.29/quarter, $1.16/year) will resurface soon if the company wishes to maintain a healthy payout ratio.

Risks & Qualities Attached to AKR Stock

In my view, the biggest risk that Acadia faces is declining foot traffic in its locations which would, in turn, lower the cash flows of its tenants. This could cause tenants to demand lower rents, which means that the trust’s properties would be worth less as their future cash flow would shrink. This is entirely possible if consumers’ purchasing power declines in the coming quarters following the shaky macroeconomic environment the market is presently experiencing.

Still, there are some notable qualities hooked to Acadia. One of the most attractive is that Acadia features the “safe haven” component of retail properties, which are necessities. Approximately half of its suburban shopping centers are grocery-anchored, while 40% of its annual base rent comes from essential retailers. Target (NYSE:TGT) is its largest tenant.

Other tenants amongst its top 10 ones are Royal Ahold, the TJX Companies (NYSE:TJX), and Trader Joe’s, which indicates that Acadia’s tenant base is of high quality. Thus, its counterparty-related risks are certainly less alarming compared to its lower-quality peers.

Is AKR Stock a Buy?

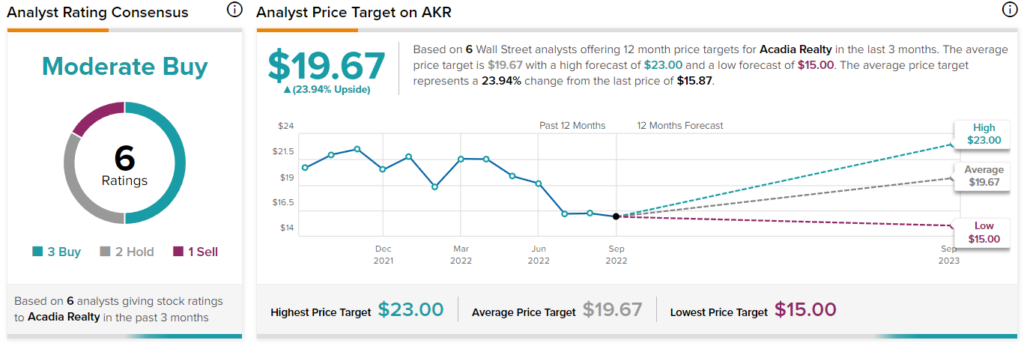

Regarding what Wall Street analysts are expecting, AKR Stock has a Moderate Buy consensus rating based on three Buys, two Holds, and one Sell assigned in the past three months. At $19.67, the average AKR stock price forecast suggests 23.9% upside potential.

Takeaway – AKR Stock Has Some Positive Developments, but Risks Remain

Acadia Realty Trust has retained its positive momentum following its post-COVID-19 recovery. After slashing the dividend in 2020, there is now ample room to support meaningful hikes from its present levels. Still, the retail real estate industry remains a rather risky place to be invested in these days. Thus, investors should not blindly invest in the company expecting only positive advancements in the coming quarters.