Recently, Kevan Stuart Gorrie, a five-star-rated insider of Granite REIT (TSE: GRT.UN), has been purchasing the stock. This could signal that the company is undervalued and has upside potential ahead. Granite REITs’ valuation suggests that the stock can climb, and analysts agree as well, giving it a Strong Buy rating. Additionally, the stock has a respectable 4.2% dividend yield as an added bonus. Therefore, GRT.UN stock seems like it could be a solid investment.

We also wrote about two other insider-buying scenarios that are similar to this one. The first article is about Slate Office REIT (TSE: SOT.UN) and the second one is about Plaza Retail REIT (TSE: PLZ.UN).

Industrial Real Estate is a Solid Long-Term Bet

Granite REIT develops, owns, and manages industrial real estate in the U.S., Canada, Austria, the Netherlands, and Germany. Industrial real estate, while more sensitive to recessions than residential real estate, is still resilient. Industrial buildings are increasingly being modernized, as they are often used as e-commerce fulfillment centers. In fact, 5% of Granite’s revenues come from Amazon (NASDAQ: AMZN). Therefore, GRT.UN has e-commerce tailwinds supporting its performance.

Granite’s other tenants are of high quality as well. Its biggest tenant, Magna International (TSE: MG) (NYSE: MGA), which is an auto parts company, makes up 28% of GRT. UN’s revenues. While the high revenue concentration may sound concerning, Magna is a solid, profitable company and has an A- credit rating. Granite has also been diversifying its revenue base more over the years, relying less on Magna. Its top 10 tenants make up 49% of revenue.

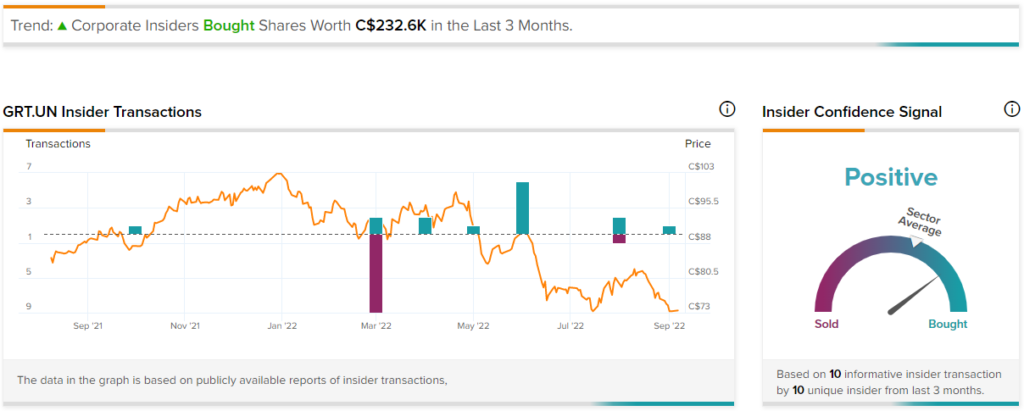

Insider Kevan Gorrie Buys GRT.UN Stock — Why It Matters

Kevan Stuart Gorrie’s recent buys are important to note for a few key reasons. First, he is a five-star-rated insider, ranked #1,377 out of 95,054 insiders on TipRanks, with an average return of 16.1% per transaction and a success rate of 78% (measured on a one-year basis). Therefore, his transactions have been worth following.

Also, his transactions are classified as “Informative Buys,” which hold more weight than “Uninformative Buys.” He’s made several purchases recently, starting four months ago, with the most recent one taking place five days ago.

In the past four months, he has bought $144.5 thousand worth of GRT.UN stock. This may not sound like much, but he likely wouldn’t be buying if he thought the stock was going to drop. The recent buys ranged from prices of C$72.97 to C$91.05 per share, with the stock currently trading at C$73.48.

Is Granite REIT Stock Undervalued?

GRT.UN stock may be undervalued, which would justify the insider buying. An important and easy valuation metric to use for Canadian REITs is the price-to-book ratio. Note that this metric isn’t as useful for American REITs due to accounting differences. Granite REIT’s price-to-book ratio is around 0.85x, meaning that it’s trading at a 15% discount to its net worth. This metric alone gives it about 18% upside potential before it reaches its net asset value.

In fact, Granite REIT has traded at an average price/book ratio of 1.2x over the past five years. The valuation premium was likely due to Granite REIT’s history of rapidly increasing its book value per share. Its book value per share was C$41.34 at the end of 2016 and is now just above C$85 as of Q2. Most Canadian REITs do not grow this quickly.

Still, there’s something to consider. Here’s what we mentioned in a recent article about a different REIT in a similar situation: “One thing to keep in mind is that its book value may potentially drop in the short term because rising interest rates are causing property values to fall, which somewhat justifies the discount. However, there is that margin of safety, and a drop is likely to be temporary in nature, in our opinion.”

We think that as the economy eventually normalizes, GRT.UN stock’s price/book ratio can rise to about 1.0x or higher, and its book value per share should eventually continue its uptrend.

Is Granite REITs Dividend Worth It?

As mentioned earlier, Granite REIT has a ~4.2% dividend, and it is paid monthly. The dividend by itself shouldn’t be enough to entice income investors, especially since it has only grown at a five-year CAGR of 2.8%. However, when combined with the company’s price/book discount and its uptrending book value per share over the long term, the dividend is an extra bonus that will boost shareholder returns.

Also, its dividend is covered, as the company’s adjusted funds from operations (AFFO) payout ratio was ~79% for the last 12 months.

Analysts Believe Granite REIT Stock is a Strong Buy

According to analysts, Granite REIT stock earns a Strong Buy consensus rating based on four unanimous Buy ratings assigned in the past three months. The average GRT.UN stock price forecast of C$96.50 implies 31.3% upside potential. Analyst price targets range from a high of C$100 to a low of C$90.

Conclusion: Granite REIT Stock Looks Solid

Granite REIT looks like an attractive investment for a few reasons. First, it operates in a resilient industry that will be supported by e-commerce growth. Next, a highly-rated insider has been buying up shares at an average price that is higher than the current price. Also, GRT.UN is trading at a 15% discount to its net worth, with an uptrending book value per share, implying solid long-term upside potential. Meanwhile, investors can receive a 4.2% dividend. Finally, analysts are bullish, seeing 31.3% upside potential.