When it comes to online travel agencies, there are really two main players in the space — Booking Holdings (NASDAQ:BKNG) and Expedia (NASDAQ:EXPE) — and both are benefiting from the post-pandemic recovery in the industry. In this piece, we used TipRanks’ Comparison Tool to evaluate these two online travel agency stocks.

Overall, it seems difficult for investors to go wrong when choosing either Booking or Expedia. In fact, Kovitz portfolio manager Bryan Engler told ValueWalk in a recent interview that he liked both Booking and Expedia. However, he added that if Booking didn’t exist, Expedia would be one of the best companies in the world, and that sums up this entire thesis into a single statement.

Where the Travel Industry Stands Now

The COVID-19 pandemic grounded planes, shuttered hotels, and locked the nation, its citizens, and its businesses down for months. When the lockdowns finally started to ease, people were itching to get out of their homes and even out of their regions, creating pent-up demand for travel.

As a result, Booking Holdings and Expedia Group were both poised to win big from all that pent-up demand, and their earnings numbers show that they certainly did. Some suggest that neither the U.S. nor the European tourism market has recovered to their pre-pandemic levels, meaning there could be even more room for growth in the coming years.

However, other indications suggest the industry could be recovering faster than what many have suggested. Business is booming for online travel agencies. The global online travel booking platform market is expected to enjoy an impressive compound annual growth rate of 14.64% between 2022-26.

Looking at Expedia and Booking in particular, one key difference between them is that Expedia gets most of its business in the U.S., while Booking primarily serves Europe. Additionally, Booking is significantly larger than Expedia, reporting 246 million room nights booked in the second quarter, versus Expedia’s 82.5 million.

Despite the claims that travel in Europe has not reached pre-pandemic levels yet, Booking is already above where it was before the pandemic in the number of room nights booked at 213 million for the second quarter of 2019.

Booking Holdings

It’s easy to see why so many hedge fund managers are bullish on Booking Holdings — and why that bullish view appears warranted. A closer look also reveals why Booking appears to be in a better position than Expedia.

However, at first glance, Booking might look overvalued to some compared to Expedia, although its valuation is down relative to history. Booking’s forward P/E stands at around 18 times, which is down significantly from around 31 times earlier this year.

In 2020, before the travel industry started making a comeback, Booking’s forward P/E hovered at around 130 to 157 times, but it has since fallen dramatically. Between August 2020 and June 2021, the forward P/E was between 40 and 50 times, making Booking’s current valuation look appealing relative to history.

A look at the company’s earnings and financials reveals even more to like. In the June 2022 quarter, Booking reported adjusted earnings of $19.08 per share on $4.3 billion in revenue, compared to the consensus numbers of $18.19 per share and $4.4 billion in revenue.

In the year-ago quarter, Booking reported a net loss of $2.55 per share on an adjusted basis with $2.16 billion in revenue. However, the company was profitable for all of 2021, reporting earnings of $1.17 billion.

One other place where Booking really stands out is in its cash versus liabilities. At the end of its most recent quarter, the company had $11.84 billion in cash and equivalents versus $10.3 billion in current liabilities and $9.8 billion in total debt.

Is BKNG Stock a Buy or Sell?

Booking Holdings has a Moderate Buy consensus rating based on 15 Buys, seven Holds, and zero Sells assigned over the last three months. At $2,418.45, the average Booking Holdings price target implies upside potential of 23.6%.

Expedia Group

Similar reviews of Expedia’s earnings results and valuation show why a bullish view may also be appropriate for this company, but compared to Booking, it just isn’t quite as strong. Expedia reported adjusted earnings of $1.96 per share on $3.2 billion in revenue for the second quarter, compared to the consensus numbers of $1.57 per share on $3 billion in revenue.

The company lost money during the first quarter, posting adjusted earnings of -$0.47 per share on $2.2 billion in revenue. In addition, Expedia posted a net loss of -$269 million for all of 2021 after a steep, pandemic-related loss of $2.7 billion for 2020.

Looking at the company’s balance sheet, Expedia has a decent cash position, but not as good as Booking’s position. Expedia had $5.6 billion in cash and equivalents at the end of its most recent quarter, $13.8 billion in current liabilities, and total debt of $7.1 billion.

At first glance, Expedia appears to be cheaper than Booking, with a forward P/E of around 13 times. However, Booking’s stronger numbers detailed above show why a premium is warranted versus Expedia’s valuation.

Like Booking, Expedia’s P/E and stock price have come down dramatically, making it cheap compared to its own history. Expedia’s P/E dropped sharply from around 47 times to 27.5 times in November 2021 before gradually sliding throughout the year to where it stands now.

The company’s P/E peaked at an unsustainable 402 times in April 2020, immediately after the steep market-wide drawdown, but it quickly plunged, falling into the red in a matter of weeks. Expedia’s valuation finally bottomed out at a P/E of around -540 times before recovering sharply to around 172 times in May 2021.

Is EXPE Stock a Good Buy?

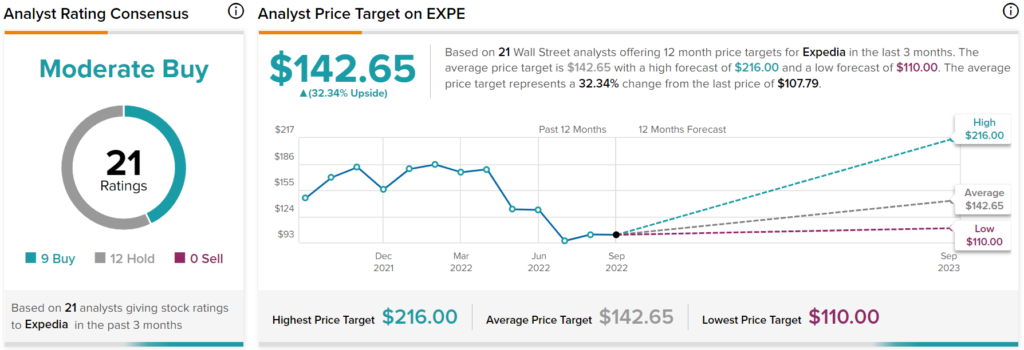

Expedia has a Moderate Buy consensus rating based on nine Buys, 13 Holds, and zero Sells over the last three months. At $142.65, the average Expedia price target implies upside potential of 32.3%.

Conclusion: Bullish on BKNG and EXPE, but BKNG is Better

Expedia Group and Booking Holdings are both hot hedge fund positions, with 13F filings from earlier this year revealing some big funds like Dan Loeb’s Third Point and Stanley Druckenmiller’s Duquesne Capital holding stakes in one or both stocks. As already shown, a closer look reveals why a bullish view on both might be appropriate, but for investors who can only pick one, Booking is the better choice.

Booking stock is down over 20%, while Expedia stock is off almost 42% year-to-date, and it’s easy to see why. Booking’s revenue, profits, and other key operating metrics have recovered from the pandemic more quickly than Expedia’s metrics have.