Chinese e-commerce giants Alibaba (NYSE:BABA) and JD.com (NASDAQ:JD) recently reported better-than-anticipated quarterly results, as they shifted their focus to discounted goods and value offerings to attract customers burdened with an uncertain macro environment. The slower-than-anticipated recovery in the Chinese economy following its reopening has pushed BABA and JD to modify their strategies for reviving their businesses, relying on bargain deals amid intense competition.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

BABA, JD Lure Customers with Bargain Deals

Earlier this month, Alibaba delivered its strongest quarterly revenue growth in almost two years, with the Q1 FY24 (June quarter) top line rising 14% year-over-year to RMB 234.16 billion. During the earnings call, management said that the company has been seeing “a very clear trend of merchant growth” on its Taobao and Tmall platforms since the company launched its value-for-money battle this fiscal year.

In particular, Taobao launched a new budget channel in April, named 99 Temai, offering an extensive range of items, including household goods and snacks. The move came amid growing competition in China’s e-commerce space, especially from PDD Holdings’ (NASDAQ:PDD) Pinduoduo platform, which is known for its bargain deals. Competition is also heating up from Douyin, a ByteDance-owned video-sharing platform that is rapidly expanding its e-commerce business.

“In the June quarter, we on-boarded a large number of new merchants, a significant portion of whom quickly started contributing to that value for money battle, winning over and converting users,” said Trudy Dai, chief executive of the Taobao and Tmall Group.

Dai added that Alibaba’s value-for-money battle will be an area of major investment. The company aims to make customers understand that the product offerings on Taobao and Tmall are not expensive. Further, the company intends to guide its merchants to offer value-for-money deals to boost their growth and ensure stable returns over the long term.

Meanwhile, rival JD.com also exceeded analysts’ Q2 2023 revenue estimates, thanks to its focus on lower-priced products. The company’s revenue grew 7.6% to about RMB 288 billion. JD Retail witnessed a rise in user shopping frequency and retention, which drove higher gross merchandise value in the quarter.

Earlier this year, JD.com launched an RMB 10 billion discount program to compete with budget shopping app Pinduoduo’s stellar rise and popularity among Chinese customers.

In an interview with Reuters, Jacob Cooke, co-founder and CEO of WPIC Marketing + Technologies, a Beijng-based e-commerce consulting firm, noted that JD.com’s low price strategy, coupled with its strength in service and logistics, has broadened its user base. Additionally, this strategy has made the platform a preferred choice over Pinduoduo in the 3C (computer, consumer electronics, and communications products) and appliance verticals.

Both Alibaba and JD.com are making their platforms attractive to merchants through lower fees and other arrangements. Interestingly, the third-party merchants on JD’s marketplace more than doubled year-over-year in the second quarter.

Overall, while China’s economic situation continues to put pressure on Alibaba and JD.com, the two companies are trying their best to thrive amid a competitive environment by focusing on discounted merchandise. They are also working on improving their profitability through cost reduction and streamlining efforts.

Wall Street’s Ratings for Chinese E-Commerce Giants

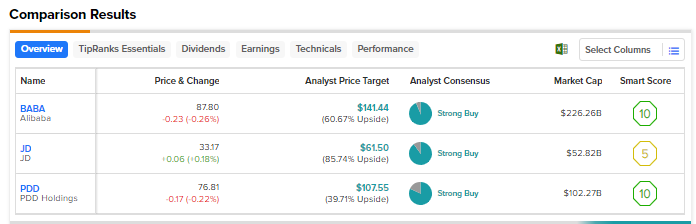

The U.S.-listed shares of Alibaba are essentially flat on a year-to-date basis, while those of JD.com and PDD Holdings are down about 41% and 6%, respectively. Using TipRanks’ Stock Comparison Tool, we find that Wall Street has a Strong Buy consensus rating for all the three Chinese e-commerce giants discussed here. Given the steep year-to-date pullback, analysts see the highest upside potential, of about 86%, in JD.com stock.