Chipmaker stocks have certainly had their ups and downs over the years, but this year, they’ve been heading mostly down, creating the potential for investors to pick and choose the cream of the crop at a discount. In this piece, we used TipRanks’ Comparison Tool to evaluate two popular semiconductor stocks — Advanced Micro Devices (AMD) and NVIDIA (NVDA). A closer look reveals why AMD deserves a bullish view, while a bearish view may be more accurate for NVDA.

Don't Miss Our Christmas Offers:

- Discover the latest stocks recommended by top Wall Street analysts, all in one place with Analyst Top Stocks

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

Advanced Micro Devices and NVIDIA have both benefited from cryptocurrency mining and other trends that drove increases in semiconductor sales.

Meanwhile, the semiconductor industry has had a difficult time since the early days of the pandemic as shortages squeezed supplies of everything from cars to smartphones and tablets.

However, the recently signed CHIPS and Science Act should give the chipmaking industry a boost. It’s aimed at bolstering the semiconductor supply chain and promoting R&D on advanced technologies in the U.S. Some chipmakers are likely to benefit from this law more than others.

The State of the Semiconductor Industry

In the U.S., one trend that’s sure to drive growth in the chip industry is the CHIPS and Science Act. Unfortunately, neither AMD nor NVIDIA is expected to benefit from that law, which is aimed at driving domestic semiconductor production. Although both companies are based in the U.S. and design their own chips, they contract third-party companies like Samsung (GB: SMSN) and TSMC (TSM) to manufacture their semiconductors.

As a result, they can’t benefit from the $52 billion the federal government has earmarked for companies to build new fabrication plants in the U.S. However, there are other effects to consider when looking at AMD and NVIDIA.

The pandemic opened a lot of people’s eyes to the importance of computer chips. Many industries were put on hold due to the widespread shortages of semiconductors. Deloitte estimates that the global semiconductor industry will be worth about $600 billion this year.

The firm also estimates that chip shortages during the pandemic likely cost more than $500 billion in lost sales, including $210 billion in lost auto sales. Deloitte sees the trend line of semiconductor sales as “steeper than ever before as we enter a period of robust secular growth.” As a result, there should be plenty of sales available to the chipmakers that take the necessary sales to attract them.

Advanced Micro Devices

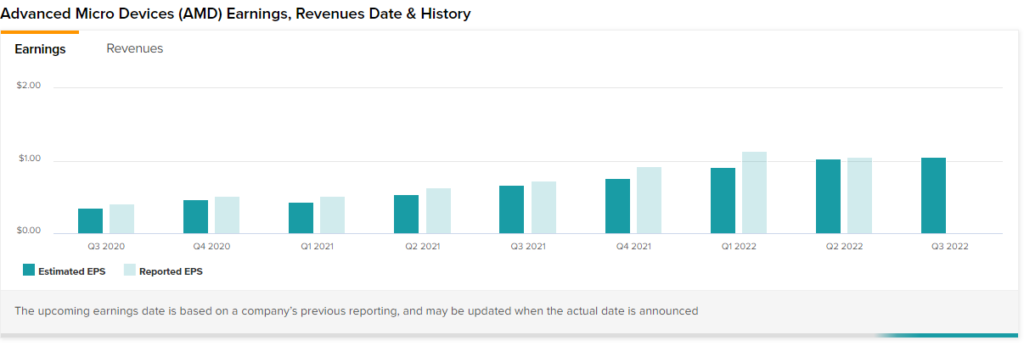

On that note, reviewing AMD’s and NVIDIA’s earnings results is very revealing. In Q2, AMD reported adjusted earnings of $1.05 per share on $6.55 billion in revenue. Analysts had been expecting earnings of $1.03 per share on $6.53 billion in revenue.

The chipmaker’s total revenue rose 70% year-over-year on the back of growth in all segments and the addition of sales from the recent Xilinx acquisition.

As a result, the slowdown in crypto mining due to the Ethereum (ETH-USD) blockchain’s switch from proof-of-work to proof-of-stake shouldn’t drastically reduce AMD’s sales.

It should also be noted that AMD’s gross margin for the June quarter declined only two percentage points year-over-year to 46% — despite this year’s soaring inflation. The chipmaker’s non-GAAP gross margin actually increased, rising six percentage points year-over-year to 54%. AMD also posted record non-GAAP operating income of $2 billion or 30% of revenue, a 24% increase year-over-year, and record non-GAAP net income of $1.7 billion.

There are other things to like about Advanced Micro Devices. For example, the company’s cash and equivalents stood at $6 billion at the end of June, while debt was less than half of that at $2.8 billion. The chipmaker also repurchased $920 million in shares during the quarter and reported record cash from operations of $1.04 billion. Free cash flow rose to $906 million.

All in all, the Q2-earnings report was a strong showing, given macroeconomic challenges. However, AMD did disappoint with its guidance, as it expects $6.7 billion in sales for the current quarter, plus or minus $200 million. Analysts had been looking for $6.83 billion.

Additionally, AMD’s P/E is low relative to its history at 40x. The chipmaker’s P/E has been declining since it peaked at ~270x in January 2020. Although AMD’s P/E is high compared to others, like Intel (INTC), the robust earnings and sales numbers suggest a premium could be warranted.

In fact, Hold-rated Intel has been struggling with execution, which is another reason AMD’s numbers have been better than Intel’s. With AMD shares down about 37% year-to-date due to the tech-focused sell-off, this could represent an attractive entry point.

Is AMD Stock a Buy?

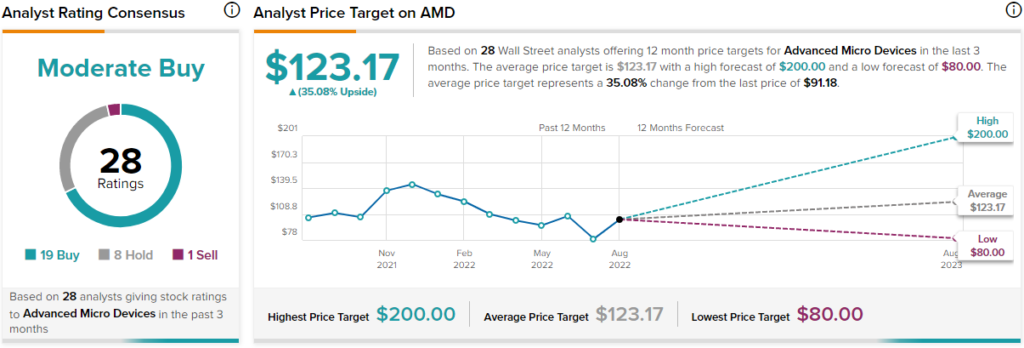

Turning to Wall Street, Advanced Micro Devices has a Moderate Buy consensus rating based on 19 Buy ratings, eight Hold ratings, and one Sell rating over the last three months. At $123.17, the average AMD price target implies upside potential of 35.1%.

NVIDIA

An analysis of NVIDIA’s latest earnings report reveals general weakness compared to AMD. It certainly seems as if the economic slowdown and soaring inflation have taken a bigger bite out of NVIDIA’s numbers.

The chipmaker reported adjusted earnings per share of $0.51 on $6.7 billion in revenue. Analysts had been expecting EPS of $0.50 on $6.7 billion in sales. While AMD’s sales soared compared to last year, NVIDIA’s revenue rose only 3%. Its gross margin fell 21.3 percentage points year-over-year, falling to 43.5%, compared to AMD’s largely-stable gross margin.

While AMD posted several record numbers, NVIDIA reported declines virtually across the board. Non-GAAP net income fell 51% year-over-year to $1.3 billion, while adjusted operating income fell 57% year-over-year to $1.3 billion.

NVIDIA cited “challenging market conditions” in its Gaming segment for the earnings disappointments. The chipmaker also reported write-downs on some of its Data Center inventory, while AMD had reported an 83% year-over-year increase in sales from its Data Center business.

For the October quarter, NVIDIA guided for $5.9 billion in sales, plus or minus 2%. That compares to the consensus of $6.9 billion, a significantly larger disappointment than AMD’s guidance.

With so many disappointments, NVIDIA surely deserves a lower P/E than AMD, but its ratio stands at 43.6X. In fact, the company’s stock rose more than 1% the day after its most recent earnings report, although it’s down 45% year-to-date.

Is It Good to Buy Nvidia Stock? Analysts Weigh In

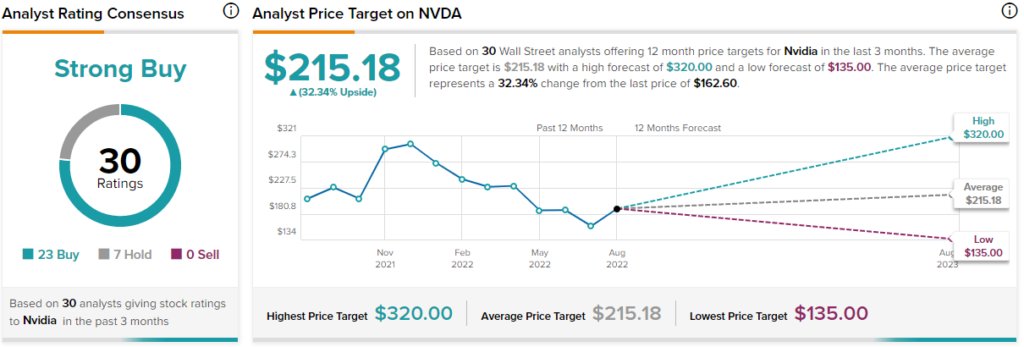

Turning to Wall Street, NVIDIA has a Strong Buy consensus rating based on 23 Buys, seven Holds, and zero Sell ratings over the last three months. At $215.18, the average NVIDIA price target implies upside potential of 32.3%.

Conclusion: AMD Looks Cheap Relative to NVIDIA

Aside from the P/E ratios and earnings numbers that make AMD look cheaper than NVDA, one other thing that should be considered when comparing the companies is AMD’s acquisition of Chinese chipmaker Xilinx. It’s unclear just how much that acquisition boosted the company’s latest earnings results because it did not break down Xilinx’s contributions.

However, Xilinx reported about $1 billion in sales for the quarter it reported in January. Thus, based on that amount, the chipmaker could have added about 37% of the sales increase AMD reported in the most recently completed quarter. If that estimate is accurate, then AMD is still growing organically on top of the Xilinx acquisition, although it’s difficult to know just how much organic growth the company is enjoying.

At the end of the day, NVIDIA’s higher P/E doesn’t appear warranted when comparing the two chipmaker’s earnings results. It seems many analysts may believe NVIDIA will have turned the corner by the time the earnings report for the October quarter comes out, but there is no certainty on that. Thus, NVIDIA currently looks riskier than AMD.