Advanced Micro Devices (AMD) has been pummeled by the tech sell-off. The sell-off has been widespread and macro-driven by rising interest rates, which should not impair AMD’s underlying value to the degree of the price decline. AMD has hit the growth at a reasonable price threshold. I am Bullish on AMD.

Maximize Your Portfolio with Data Driven Insights:

- Leverage the power of TipRanks' Smart Score, a data-driven tool to help you uncover top performing stocks and make informed investment decisions.

- Monitor your stock picks and compare them to top Wall Street Analysts' recommendations with Your Smart Portfolio

The Sell-Off

The Nasdaq 100 Index (NDX) is down over 21% from its all-time high, which puts it past the standard threshold of a bear market (a drop of at least 20%). AMD is trading at nearly half of its all-time highs that it set in November 2021. AMD’s sell-off period aligns with the NDX sell-off period.

AMD and NDX have a high correlation of 0.80 for the last six months, an R-squared of 0.64, and AMD has a beta of 1.78. Six-month values are all higher than longer terms, meaning that AMD’s returns have increased its reliance on the performance of the broader market.

When individual assets are overly attached to the broad market performance, it can create oversold and overbought scenarios. AMD has been disproportionately punished.

Why AMD is Oversold

Bears argue that AMD was a large pandemic beneficiary that is now facing the downside. The fact of the matter is if semiconductors face headwinds, they will only be short term in nature.

The short term is slightly hindered, as GPU demand has largely diminished. This is due to large Ethereum (ETH-USD) miners no longer purchasing GPUs as the switch to proof-of-stake is expected to occur within 2022. However, GPUs only make up a small portion of AMD’s overall sales and profits.

As well, many are citing the decrease in market prices of GPUs, but AMD wasn’t getting the benefit of higher prices; retailers and resellers were. To prove this, we can look at AMD’s computing and graphics segment’s operating margin; if it is notably higher, it means AMD has been able to extract higher prices from its customers. Q4-2021’s computing and graphics operating margin is 21.9%, compared to pre-shortage Q4 2019’s margin of 21.7%, materially the same.

Some bears will cite Intel’s (INTC) entry into the GPU market as a reason for downside potential. Intel’s GPUs are expected to come to market in Q2 2022, but leaked performance data shows they are trailing well behind AMD and Nvidia’s (NVDA) current offerings, both of which are expected to be refreshed in Q3/Q4 2022.

AMD’s long-term growth is still intact. Enterprise Solutions are leading AMD’s long-term fiscal growth, not the retail market. Enterprise revenue grew 113% for 2021, while retail Computing & Graphics only grew 45%. Profit growth shows an even bigger discrepancy because AMD is starting to benefit from economies of scale for its enterprise line. 2021 Enterprise profit grew 406% year-over-year, compared to Computing & Graphic’s 65%.

AMD’s future is largely based on the Enterprise segment, which is less cyclical than the retail side.

Investing in Long-term Growth

AMD announced on April 4th that it has a definitive agreement to acquire Pensando for ~$1.9 billion. Pensando will aid AMD in its data center value proposition. Pensando’s products allow for a more efficient distribution of computing power, which lifts the overall efficiency of data centers.

The data center market is growing fast. According to Arizton, the data center market should grow to a market size of $288.3 billion by 2027, a 4.95% CAGR.

AMD also finalized its acquisition of Xilinx for $35 billion in February. The two companies are synergistic and should be a catalyst for long-term growth. The merger combines the engineering talent of the two teams, and the underlying products are synergistic for adaptive computing.

Xilinx’s offerings allow for AI-driven edge computing. The AI market is expected to grow even faster. According to a report by Fortune Business Insights, the AI market size is expected to grow to $1,394 billion by 2029, a 20.1% CAGR.

A key commonality between these two acquisitions is they are not directed at enhancing AMD’s retail offerings; they are aimed at large corporations. AMD is pushing into higher-margin markets.

Financially Undervalued

AMD is a growth company and has had its price butchered due to a perceived reduction in growth. AMD management expects growth of 31% for 2022 (before the Xilinx merger).

When a profitable company like AMD is expecting significant growth, a P/E ratio of 33 is extremely low. The forward P/E ratio of ~21 highlights the undervaluation when growth is considered.

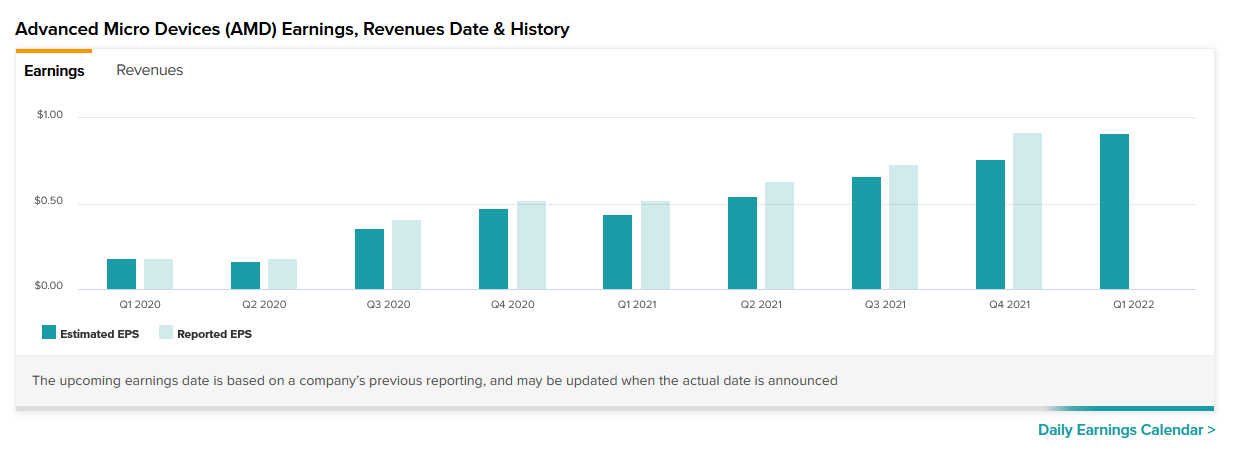

Additionally, the forward P/E ratio uses analyst estimates. Analysts have historically underestimated AMD earnings.

AMD reports Q1-2022 earnings on May 3rd, so we will see if analysts continue to underestimate the company.

Wall Street’s Take

Turning to Wall Street, AMD earns a Moderate Buy rating, with 13 Buys and eight Hold ratings assigned over the past three months.

The average AMD stock price forecast of $143.94 implies 67.7% upside potential.

Conclusion

The bearish argument of the cyclical downturn has been overblown for AMD. The recent sell-off has made the broad market panic. I agree with Wall Street; I am Bullish on AMD.

Discover new investment ideas with data you can trust.

Read full Disclaimer & Disclosure