Advanced Micro Devices (NASDAQ:AMD) has shown in the past that it has what it takes to rein in a segment leader. Intel was once the undisputed CPU king, but over the years, by a combination of offering its own excellent products and taking advantage of the bigger firm’s missteps, AMD has significantly closed the gap and claims a much bigger chunk of the CPU market today.

Now, it is faced with the challenge of halting the progress of another runaway leader. So far, Nvidia has completely dominated the AI accelerator market and due to limitations in supply, customers frequently opt for the complete Nvidia package, including switching and interconnect components, to ensure priority delivery of accelerators.

However, according to Barclays analyst Tom O’Malley, that could be about to change, and AMD stands to reap the rewards.

“We see 2024 as the year AI begins to open up, which primarily benefits AMD and we think that valuation will center more on ’26 and beyond as investors contemplate a larger market, and a more positive share dynamic for AMD,” O’Malley opined.

O’Malley also highlights that hyperscalers are currently facing a dilemma. They must overcome the software obstacle posed by Nvidia by deploying hardware to facilitate software learning. While Nvidia maintains a substantial lead, O’Malley thinks that the “desire to have a second source will overwhelm difficulties for the software ecosystem.”

And it appears that this is indeed happening. Following a trip to Asia in November and checking in with the supply chain, O’Malley is already receiving “much stronger feedback” on AMD’s MI300 AI accelerator series. Therefore, although the company has projected $2 billion in MI300 sales for CY24, O’Malley believes that the company is likely to reach a run-rate of closer to $4 billion by the end of the year. By 2025, he anticipates this figure climbing to more than $7 billion. He explained, “We think the ramp is driven by multiple customers across hyperscale and Enterprise and more 2H loaded (we model 40% Q/Q growth in Q3/Q4).”

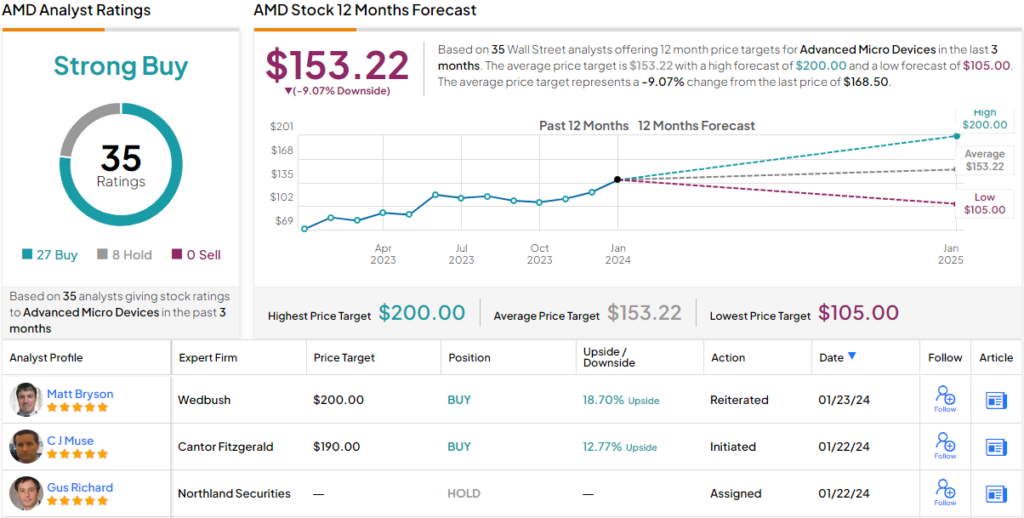

Accordingly, given these prospects, O’Malley has raised his price target for AMD from $120 to a Street-high $200, implying the shares will climb ~19% in the year ahead. Needless to say, O’Malley’s rating stays at Overweight (i.e., Buy). (To watch O’Malley’s track record, click here)

O’Malley also expects some “pushback here” given AMD already commands a high valuation, but going back to the Intel case, he thinks a comparable scenario could play out again here. “Similar to the stock run when AMD started to take share in the server CPU market, we think investors will look at share dynamics of a more mature market, which helps justify valuation,” he summed up.

Elsewhere on Wall Street, with 26 Buy ratings outweighing 8 Holds, the stock boasts a Strong Buy consensus rating. However, it’s worth noting a somewhat contradictory aspect: the average price target is $153.22, indicating a 9% downside from current levels. It will be interesting to see if other analysts follow O’Malley’s lead and revise their price targets upward. (See AMD stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.