Despite posting disappointing top revenue and earnings misses for Q4 last week, Zymeworks (ZYME) has seen its shares rally over 5%, thanks in part to a positive outlook from analysts on the company’s prospects over the next year. In 2024, the company made significant strides in its product pipeline, kicking off human trials for ZW191 and ZW171, both targeted to combat solid tumors. Further, Ziihera, a HER2-positive biliary tract cancer treatment, has recently secured approval for its use in the United States. Despite a net loss for 2024, the company remains financially stable, with existing cash resources to fund operations well into the second half of 2027.

Runway for Robust Pipeline Extends into 2027

Zymeworks is a clinical-stage biotechnology company working on multi-functional biotherapeutics to improve care for hard-to-treat diseases. The company has recently announced that it is making significant inroads, especially with the start of first-in-human studies for ZW191 and ZW171, both of which have been developed to address vital needs in treating solid tumors. Furthermore, the company plans to expedite the IND submission for ZW251, an antibody-drug conjugate targeting the protein Glypican-3 (GPC3), which has been linked to cancer, to mid-2025.

In addition to its pipeline of treatments, Zymeworks partnered product, Ziihera (zanidatamab-hrii), recently achieved a breakthrough with its expedited approval and release for HER2-positive biliary tract cancer. Further decisions on the regulatory actions in the European Union and China and the results from the HERIZON-GEA-01 study of Ziihera are expected in the second half of 2025.

In 2024, Zymework’s reported revenue of $76.3 million was primarily driven by milestone payments from various drug development and supply partnerships. The company’s R&D expenses dropped to $134.6 million from $143.6 million in 2023 due to the completion of related manufacturing and IND-enabling studies in 2023.

This resulted in a net loss of $122.7 million for the year, up from $118.7 million in 2023. Yet, as of year-end, the company had $324.2 million in cash resources, sufficient to fund operations into the second half of 2027.

Analysts Response Mostly Bullish

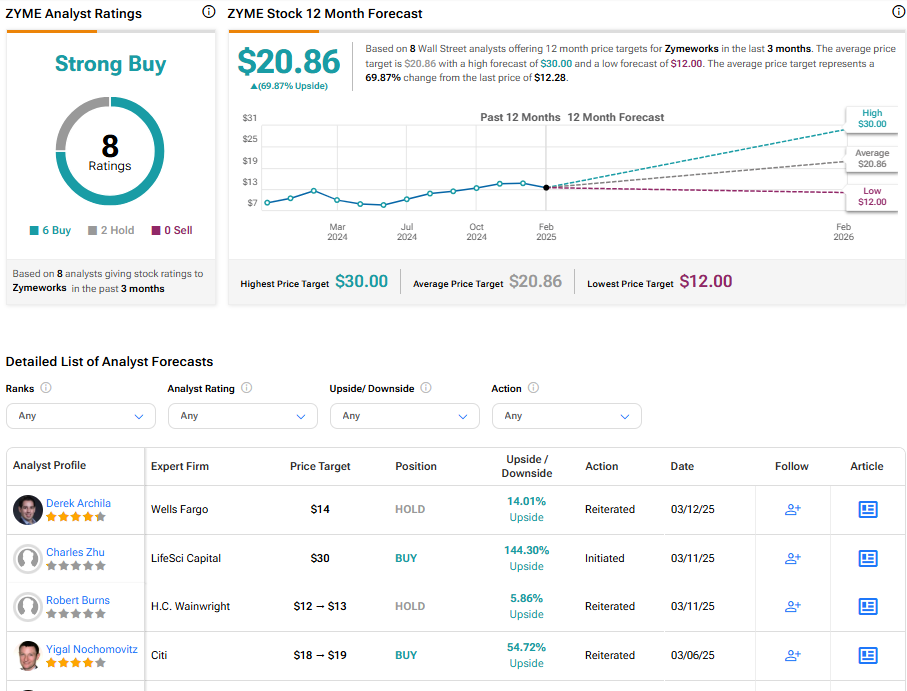

Response to the recent financial results has been mixed among analysts following the company. Robert Burns of H.C. Wainwright has reiterated his Hold rating on the shares, with a price target of $13.00, noting a greater-than-expected net loss in Q4 of 2024 due to lower-than-forecast revenue. He suggests that potential upcoming catalysts, such as regulatory decisions and clinical trials in 2025, pose the risk of setbacks and warrant a cautious approach.

Conversely, Leerink Partners analyst Andrew Berens has maintained a bullish stance on ZYME, giving it a Buy rating, noting the promising outlook for the zanidatamab program, with an expected readout in 2H of 2025, that might suggest a positive performance trajectory. Further, the company’s focus on advancing other candidates like ZW251, backed by its strong financial position, bodes well for upside potential.

Zymeworks is rated a Strong Buy overall, based on the recent recommendations of eight analysts. The average price target for ZYME stock is $20.86, which represents a potential upside of 69.87% from current levels.

See more ZYME analyst ratings.

Questions or Comments about the article? Write to editor@tipranks.com