California-based Zendesk (ZEN) launched in 2007. It provides customer service platforms and more. (See Analysts’ Top Stocks on TipRanks)

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

With this in mind, we used TipRanks to take a look at the newly added risk factors for Zendesk. (See Insiders’ Hot Stocks on TipRanks)

Q3 Financial Results

Zendesk reported revenue of $347 million for Q3 2021, against $262 million in the same quarter last year, and exceeded the consensus estimate of $335.1 million. It posted adjusted EPS of $0.17, same as a year ago and matched the consensus estimate. The company ended Q3 with $533.5 million in cash.

Zendesk anticipates Q4 revenue in the range of $366 million to $372 million. It expects 2021 full-year revenue in the band of $1.33 billion to $1.34 billion.

Corporate Updates

Zendesk has agreed to acquire Momentive (MNTV) together with its survey platform SurveyMonkey. The deal values Momentive at about $28 per share and Zendesk plans to pay for the purchase with its stock.

As a result, Momentive shareholders will end up with a stake of 22% in Zendesk if the merger is successfully completed. The transaction is expected to close in the first half of 2022, and Zendesk hopes the merger with Momentive will help it achieve $3.5 billion in annual revenue in 2024 instead of 2025 as it earlier forecast.

Zendesk plans to host its 2021 investor day on November 18. The event will include executive presentations and question and answer sessions.

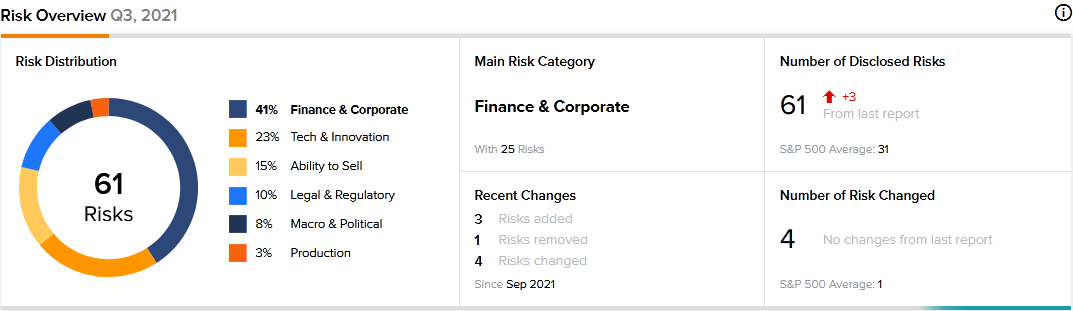

Risk Factors

Zendesk carries 61 risk factors, according to the new TipRanks Risk Factors tool. It recently updated its risk profile with three new risk factors related to the pending Momentive acquisition.

Zendesk has told investors that its expenses related to the Momentive acquisition could increase if the transaction delays to close. It says delays could be caused by regulatory requirements, and the need for the deal to be approved by shareholders of both companies.

It has also informed investors that even if it succeeds in closing the Momentive acquisition, it may not fully achieve the anticipated benefits of the merger.

Zendesk has also cautioned investors that the agreement to acquire Momentive could cause uncertainty among its staff, customers, and suppliers. As a result, some employees may decide to leave and some customers, and suppliers may delay or cease doing business with the company.

Forty-one percent of Zendesk’s risk factors fall under the Finance and Corporate. That is below the sector average of 48%. Zendesk’s stock has declined 14.6% over the past 12 months.

Analysts’ Take

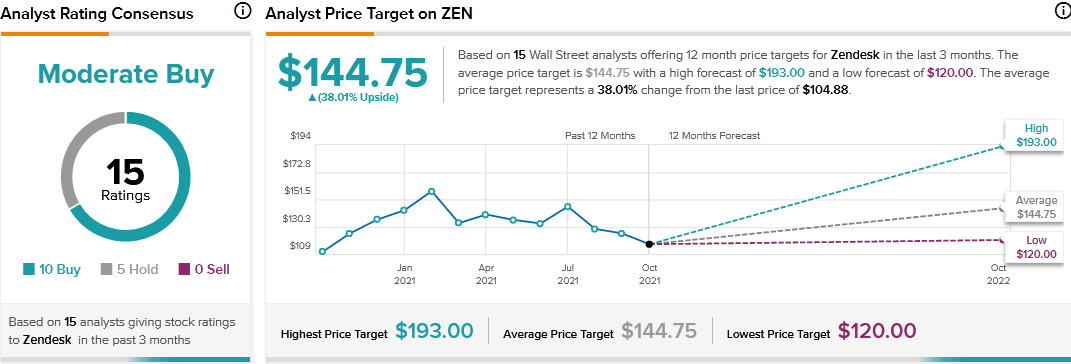

Following Zendesk’s Q3 earnings report, Jefferies analyst Samad Samana downgraded the rating on Zendesk stock to a Hold from a Buy.

Furthermore, the analyst lowered his price target to $120 from $175. Samana’s reduced price target still suggests 14.4% upside potential. The analyst noted that Zendesk delivered strong Q3 results, and issued an encouraging Q4 outlook.

Samana is concerned about the Momentive acquisition deal though, and thinks that Zendesk’s target of getting to $3.5 billion revenue in 2024 may not come easily.

Overall, consensus among analysts is a Moderate Buy based on 10 Buys and five Holds. The average Zendesk price target of $144.75 implies 38% upside potential to current levels.

Related News:

Seagen Adds Two New Risk Factors

Arthur J Gallagher Outlines New Risk Factors

Lightspeed to Expand Footprint in Australia and the U.S.