Global restaurant chain operator Yum! Brands, Inc. (YUM) delivered strong third-quarter results driven by record unit growth and continued digital sales momentum, especially in the KFC and Taco Bell brands. Shares closed at $125.88 on October 28.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

The company posted adjusted earnings of $1.22 per share, up 21% year-over-year and significantly higher than analyst estimates of $1.08 per share.

To add to that, total revenue came in at $1.61 billion, increasing 11% compared to the year-ago period, and also surpassed Street estimates of $1.59 billion.

Further, compared to the prior-year quarter, YUM added 760 net new units, recording unit growth of 4%, systemwide sales (excluding foreign currency translation) grew 8%, and same-store sales grew 5%. (See Insiders’ Hot Stocks on TipRanks)

Commenting on the results, David Gibbs, CEO of Yum! Said, “As we continue to navigate the short-term uncertainties of the COVID recovery, we are incredibly confident in the ability of our iconic brands and our world-class talent to drive growth and maximize stakeholder value by delivering on our long-term growth algorithm.”

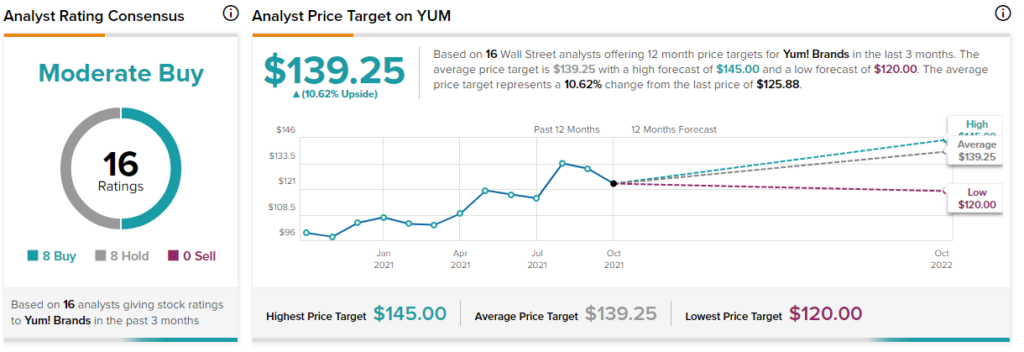

Delighted with the underlying comparable-store sales strength in the international segment (excluding Asia and China), Christopher O`Cull of Stifel Nicolaus maintained a Buy rating on the stock with a price target of $145, implying 15.2% upside potential to current levels.

O`Cull noted that YUM’s digital and off-premise channels have witnessed rapid expansion due to the COVID-19 pandemic and believes sales growth in these channels will continue. Finally, the analyst also stated that YUM’s limited exposure to the European market strengthens the company’s position as he expects Europe’s recovery to be slower than that of the U.S. and China.

O`Cull said, “We remain confident the company can maintain reasonably strong comp momentum in its U.S. and International segments despite periods of pandemic-related disruptions. More important, in our view, was the impressive level of development in the quarter and management’s confidence in YUM’s ability to sustain development momentum over time, driven by improving new unit economics and innovation around new store formats.”

With 8 Buys and 8 Holds, the stock has a Moderate Buy consensus rating. The average Yum! Brands price target of $139.25 implies 10.6% upside potential to current levels. Shares have gained 32.6% over the past year.

Related News:

ADP Beats Q1 Expectations; Shares Hit All-Time High

General Motors Plunges 5.4% Despite Exceeding Q3 Expectations

Dynatrace Falls 9.9% Despite Posting Strong Beat-and-Raise Q2 Results