Since posting expectation-beating revenue for the third quarter in November, Workiva (WK) has seen shares spike up over 40%. The company offers a unique SaaS platform that combines financial reporting with elements of Environmental, Social, and Governance (ESG) and Governance, Risk, and Compliance (GRC). Over the past year, Workiva has seen solid growth, with the number of customers reaching 6,237, marking a net increase of 292. The company’s revenue retention rates have also been strong, and larger contracts have seen notable growth.

The outlook indicates continued growth, with total revenue for 2024 expected to reach between $733 and $735 million. While the stock is potentially attractive over the long term, it trades at a relatively rich valuation, suggesting investors might want to wait for a more favorable window of opportunity.

Workiva’s Client List Thrives

Workiva provides a unified software-as-a-service (SaaS) platform that facilitates financial reporting, ESG, and Governance, Risk, and Compliance (GRC) integration. The platform streamlines complex reporting processes that help ensure secure, transparent, and auditable integrated reporting.

Key metrics show growth and retention in its customer base. The client portfolio grew to 6,237 customers, a net increase of 292 from the previous year. The company also recently reported a steady revenue retention rate of 98%, increasing to 111% when including add-on revenue.

Workiva also recently noted an uptick in large contracts. It reported 1,926 customers with an annual contract value (ACV) of over $100,000, a 23% increase from the previous year. The number of customers with an ACV of more than $300,000 and $500,000 increased by 29% and 28%, respectively.

Solid Revenue and Earnings Growth

The company recently posted Q3 2024 financial results with expectations beating revenue of $186 million, representing a 17% increase from the $158 million realized in Q3 2023. This revenue was primarily driven by a 19% increase in subscription and support revenue, contributing $171 million. Despite GAAP losses from operations of $22 million, an increase from the $16 million loss of the previous year, non-GAAP income from operations was reported at $8 million, a rise compared to the non-GAAP income of $5 million in last year’s third quarter.

The GAAP gross profit for Q3 2024 was $142 million, compared to $120 million in the same quarter of the previous year, reflecting a margin increase from 75.8% to 76.5%. Non-GAAP gross profit for the same quarter was reported at $146 million, which equates to a 20% increase from the previous year, and the margin improved to 78.6% from the prior year’s 76.9%.

Net losses decreased significantly, with GAAP net loss reported at $17 million compared to the $56 million loss in Q3 2023. Concurrently, non-GAAP net income flipped to a positive $12 million from a $35 million net loss in the prior year’s third quarter, while non-GAAP earnings per share (EPS) of $0.21 slightly missed analyst projections by $0.02.

As of the quarter’s end, Workiva reported a total of $776 million in cash, cash equivalents, and marketable securities.

Workiva’s management has released financial guidance for the fourth quarter and full year of 2024. The company’s Q4 total revenue is anticipated to be between $194 million and $196 million, with a GAAP loss from operations ranging from $16 million to $14 million. The non-GAAP income from operations is projected to fall between $13 million and $15 million. The expected GAAP net loss per basic share will be between $0.21 and $0.18, whereas the non-GAAP net income is estimated to be between $0.31 and $0.34.

For the full year 2024, the total revenue is expected to be between $733 million and $735 million, with a GAAP loss from operations between $79 million and $77 million and non-GAAP income from operations between $30 million and $32 million. The GAAP net loss per basic share is projected to be between $1.05 and $1.02, while non-GAAP net income per basic share is between $0.93 and $0.96.

Ongoing Positive Price Momentum

The recent price surge in the shares has helped salvage what had been a down year, with the shares now up 7% over the past year. The stock trades near the upper end of its 52-week price range of $65.47 – $116.83 and shows ongoing positive price momentum as it trades above major moving averages. However, the stock trades at a premium, as the P/S ratio of 8.7x is well above the Information Technology sector average of 3.21x.

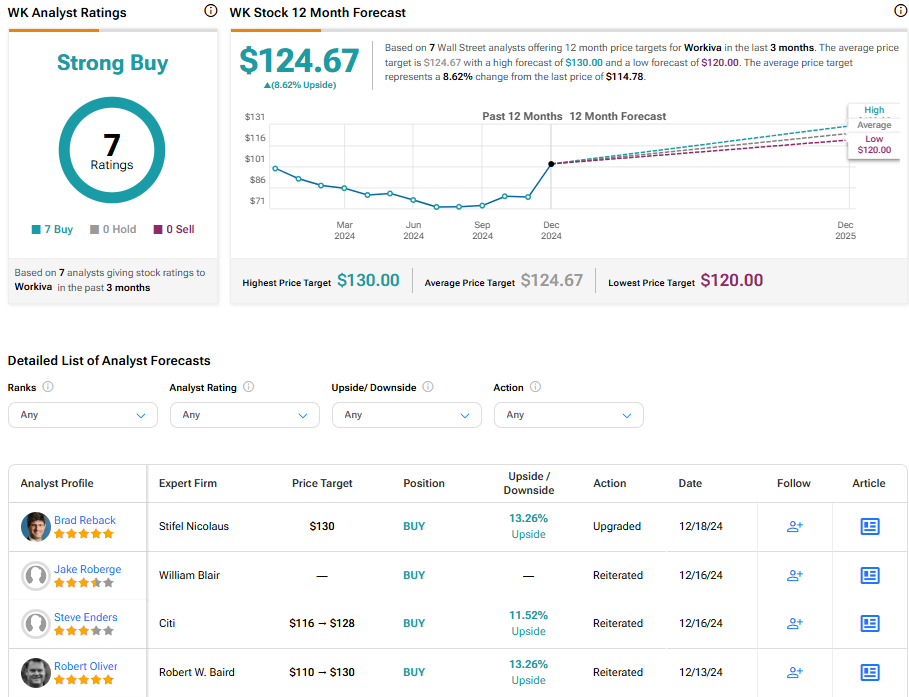

Analysts following the company have been constructive on WK stock. For example, Stifel analyst Brad Reback, a five-star analyst according to Tipranks’ ratings, recently upgraded the shares to a Buy rating with a price target of $130, noting sales execution and revenue and margin growth expectations position the company for sustained outperformance.

Based on seven analysts’ recent recommendations, Workiva is rated a Strong Buy overall. Their average price target for WK stock is $124.67, representing an 8.62% upside potential from current levels.

WK in Summary

Workiva has shown significant growth and resilience this past year. Its customer base has steadily expanded, helping to drive a surge in revenue. Although the stock’s current valuation is high, suggesting caution in investing immediately, its strong performance and positive outlook make it a potential long-term asset for investors. Investors may want to look for a more favorable window of opportunity to explore this promising investment.