WNS Holdings (WNS) reported stronger-than-expected fiscal 2022 Q1 results, topping both earnings and revenue estimates, driven by robust revenue growth and improved margins despite COVID-19 related issues faced during the quarter.

Shares of the global business process management services provider have gained 32% over the past year.

The company reported adjusted earnings of $0.76 per ADS (American Depositary Share), beating analysts’ expectations of $0.68 per ADS. Revenues of $236.3 million exceeded the consensus estimate of $230.1 million.

Notably, revenues grew 21.9% on a year-over-year basis, driven by new client additions and a favorable currency impact. The company reported earnings of $0.50 per ADS in the prior-year period.

WNS’s CEO Keshav Murugesh commented, “Despite challenges related to a spike of COVID-19 cases in India during the quarter, WNS was able to execute well in a difficult environment, protecting the health and safety of our employees and the mission-critical operations of our clients.” (See WNS stock charts on TipRanks)

He further added, “The company continues to see significant opportunities to capitalize on an under-penetrated customer base, a strong new business pipeline, and a robust BPM market driven by demand for digital transformation and improved competitive positioning.”

Based on management’s visibility and strong Q1 results, the company raised its guidance for Fiscal 2022. The company now forecasts adjusted earnings in the range of $3.09 to $3.28 per share, while the consensus estimate is pegged at $3.13 per share. Revenues are forecast to grow 11% to 16% and be in the range of $961 – $1,009 million, versus the consensus estimate of $983.2 million.

Following the upbeat Q1 results, Cowen & Co. analyst Bryan Bergin increased the price target from $82 to $90 (11.3% upside potential) and reiterated a Buy rating on the stock.

Bergin said, “Broadly healthy pipeline commentary is encouraging, as is BPMs’ proficiency in hybrid operational execution which increasingly will be a new normal. Raised FY22 outlook remains conservative should Travel client recovery momentum continue.”

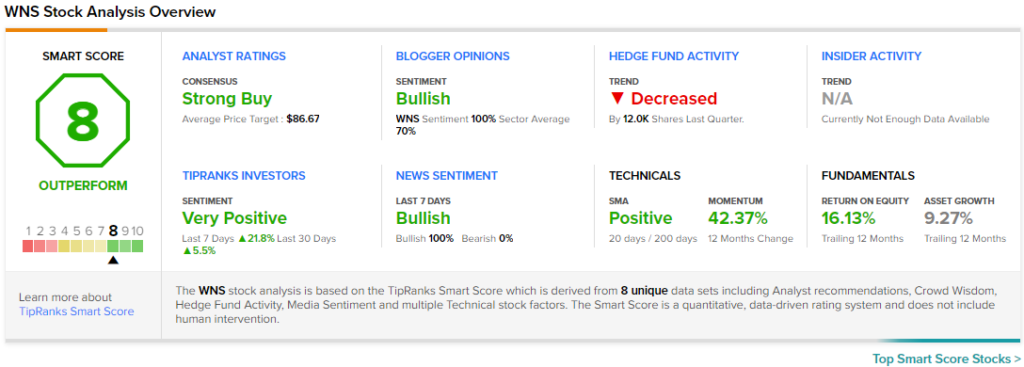

Consensus among analysts is a Strong Buy based on 5 Buys and 1 Hold. The average WNS price target of $86.67 implies 7.1% upside potential to current levels.

WNS scores an 8 out of 10 on TipRanks’ Smart Score rating system, indicating that the stock has strong potential to outperform market expectations.

Related News:

PepsiCo Shares Jump 2.3% on Q2 Beat and Raised Guidance

Goldman Sachs Reports Blowout Q2 Results; Hikes Dividend by 60%

Organigram Bounces 11% on Q3 Revenue Beat