Winnebago Industries (WGO) has not been immune to a challenging environment for recreational vehicles (RVs), with the company recently reporting disappointing results by missing top-and-bottom-line expectations for Q1 FY2025. The drop is primarily attributed to selling lower volumes and reducing average selling prices per unit. Despite a flourishing RV business in 2021, which saw a record quarterly revenue high, the firm now faces a challenging macroeconomic landscape and a drastic fall in industry-wide sales. This slump is linked to rising interest rates, causing consumers to postpone large purchases like RVs.

Nonetheless, Winnebago anticipates better days ahead with its Fiscal 2025 guidance pointing to anticipated demand and strengthening its position with new products, healthy channel relationships, and a robust financial foundation. With its stock trading at a relative discount, this could be a window of opportunity for value-oriented investors willing to be patient while the RV market recovers.

Winnebago Positioned for Industry Rebound

Winnebago is a significant player in the North American outdoor lifestyle products manufacturing industry. The company has a broad portfolio of brands, including Winnebago, Grand Design, Chris-Craft, Newmar, and Barletta – all predominantly utilized in leisure travel and outdoor recreational events.

The RV sector has experienced significant challenges due to escalating interest rates and careful consumer spending. Revenue in the Towable RV and Motorhome RV segments has declined despite efforts to boost sales through increased discounts. Furthermore, the promotional environment and decreased sales have led to a sharp fall in the gross margin.

Despite current conditions, the long-term outlook appears more positive with healthier dealer inventory levels in place. This could potentially bolster more substantial margins and earnings when the industry recovers from the downturn.

A Challenging Q2 Ahead

Winnebago has recently announced results for the Q1 of FY 2025, reporting a significant decrease in revenues, with $625.6 million down 18% year-over-year. This downturn was primarily due to decreased unit volume and a reduced average selling price per unit associated with the product mix. Gross profit for the quarter was $76.8 million, down by 33.7% from last year’s $115.8 million. The company’s gross profit margin fell by 290 basis points to 12.3%.

Operating expenses slightly increased by 1.3%, reaching $77.7 million, due mainly to strategic investments. There was a net loss of $5.2 million for the quarter compared to a net income of $25.8 million in the first quarter last year. The adjusted loss per share was $0.03, in contrast to the adjusted earnings per share of $0.95 in the first quarter of last year.

As of the quarter’s end, the company reported a total outstanding debt of $696.9 million, with working capital at $556.1 million. The Board of Directors has approved a quarterly cash dividend of $0.34 per share to be paid on January 29, 2025.

What’s expected in 2025

Management has offered fiscal guidance for 2025, forecasting revenue between $2.9 billion and $3.2 billion. The company has revised its expected reported EPS to $2.50-$3.80 per share and adjusted EPS to $3.10-$4.40 per share, maintaining the midpoints of the previous outlook. This outlook considers current trends in the RV sector, market competition, customer preference changes, and key macroeconomic factors that could impact demand.

Despite anticipated seasonal fluctuations and challenging market conditions, the company is confident in its ability to leverage the expected surge in demand during the spring selling season, which it attributes to its strong product lineup, healthy channel partnerships, and robust financial base.

Analysts Remain Cautiously Optimistic

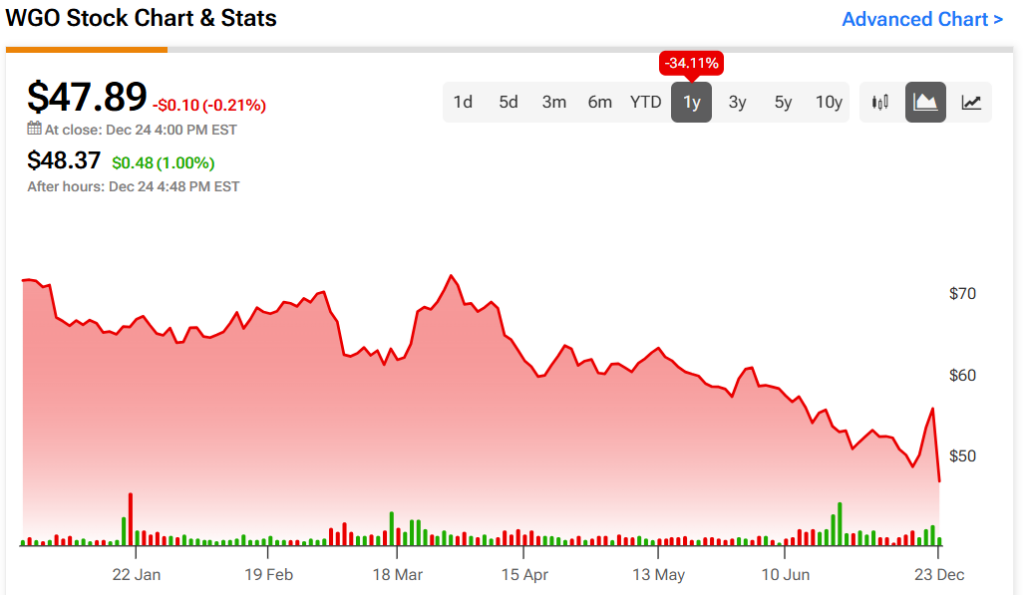

The stock has been downward trending, shedding 34% over the past year. It trades at the bottom of its 52-week price range of $49.68 – $74.35 and shows ongoing negative price momentum as it trades below the major moving averages. It trades at a relative discount, with a P/S ratio of 0.49x compared to the Consumer Discretionary sector average of 0.93x.

Analysts following the company have been cautiously optimistic about WGO stock. For instance, Citi’s James Hardiman, a four-star analyst according to Tipranks’ ratings, recently lowered the price target on the shares to $61 while maintaining a Buy rating, noting the company’s Q1 results were well short of expectations, with a problematic Q2 likely to follow. Yet, Winnebago is optimistic about the second half of its fiscal year.

Winnebago Industries is rated a Moderate Buy overall, based on the most recent recommendations of nine analysts. Their average price target for WGO stock is $67.67, representing a potential upside of 41.30% from current levels.

Bottom Line on WGO

Despite its industry leadership position, Winnebago has not escaped the recent recreational vehicles (RV) industry downturn and anticipates further challenges in Q2. However, the company maintains a positive long-term outlook, expecting a recovery in the RV market. The stock trades at a relative discount, which could present an opportunity for patient, value-driven investors.