Shares of Williams-Sonoma soared 12.3% in Wednesday’s post-market trading session after the retail company posted strong fiscal 4Q earnings. The outstanding performance was driven by online buying as consumers shopped from home due to pandemic-led restrictions.

Williams-Sonoma’s (WSM) 4Q adjusted earnings jumped 85% to $3.95 per share on a year-over-year basis and outpaced the Street estimates of $3.39 per share. Net revenues increased 27.8% to $2.3 billion, topping analysts’ expectations of $2.17 billion.

The company’s comparable brand revenue growth came in at 25.7% in the quarter, while demand comparable brand revenue growth was 30%. Additionally, e-commerce comparable brand revenue growth stood at 47.9%, making up 70% of total net revenues.

Williams-Sonoma CEO Laura Alber said, “Longer-term, we have accelerated our path to $10 billion in net revenues and see us hitting this milestone in the next five years, with operating margins at 15%.”

The fiscal year 2021 financial performance is expected to be in line with the long-term financial outlook of mid-to-high single-digit net revenue growth and year-over-year non-GAAP operating margin expansion, the company said. (See Williams-Sonoma stock analysis on TipRanks)

Additionally, the company announced an 11.3% increase in its quarterly cash dividend to $0.59 per share. The new dividend will be paid on May 28 to shareholders of record as of April 23. The company’s annual dividend of $2.36 per share now reflects a dividend yield of 1.73%. Furthermore, a new $1 billion share repurchase program was approved, replacing the existing buyback program.

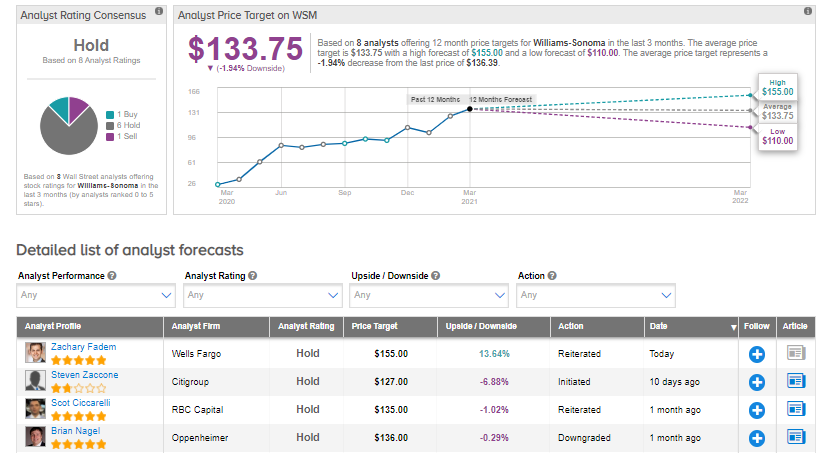

Following the 4Q results, Wells Fargo analyst Zachary Fadem increased the stock’s price target to $155 (13.6% upside potential) from $135 and reiterated a Hold rating.

Fadem commented, “WSM’s Q4 print gave the bulls nearly everything they were looking for with a Q4 comp/margin beat, reaffirmed FY21 growth, higher LT targets and $1B buyback to boot.”

Additionally, the analyst said, “While tough 2H compares add uncertainty and our FY21 model sits below the outlook (EBIT -45bps), it’s clear that our Equal Weight rating has been the wrong call, and we’re still looking for a better entry point.”

Overall, the stock has a Hold consensus rating based on 1 Buy, 6 Holds, and 1 Sell. The average analyst price target of $133.75 implies almost 2% downside potential from current levels. Shares have increased 32.5% so far this year.

Related News:

Arbutus Gets Go Ahead To Kick Off Phase 1a/1b Clinical Trial Of AB-836

Smartsheet Posts Better-Than-Feared Quarterly Loss, Sales Outperform

Jabil’s Sales Guidance Tops Estimates After 2Q Beat; Shares Jump Pre-Market