My bullish thesis on Verizon (NYSE:VZ), the second most valuable U.S. telecom carrier, centers on its role as a defensive stock suited for portfolio strategy rather than solely relying on future price appreciation. Despite grappling with significant debt and cash flow disruptions in recent years, Verizon has maintained its dividend growth. After briefly examining its consistent dividends and strategic portfolio role, I will explain why I consider investing in Verizon, a defensive stock, to be a favorable opportunity at present.

Dividend Consistency and Growth amid Backdrops

Since the 1980s, when it was still called Bell Atlantic, Verizon has paid generous dividends to its shareholders. Over the last 17 years, the company has increased its dividend every year, with a CAGR of 5.3% in the last decade.

In the last three years, Verizon has risen its quarterly dividend per share from ~$0.63 $0.665. However, during this time, the stock has dropped about 30%. This downturn could be attributed due to fierce domestic competition, high investments in 5G infrastructure, and significant debt from strategic past acquisitions like AOL, Yahoo, and TracFone.

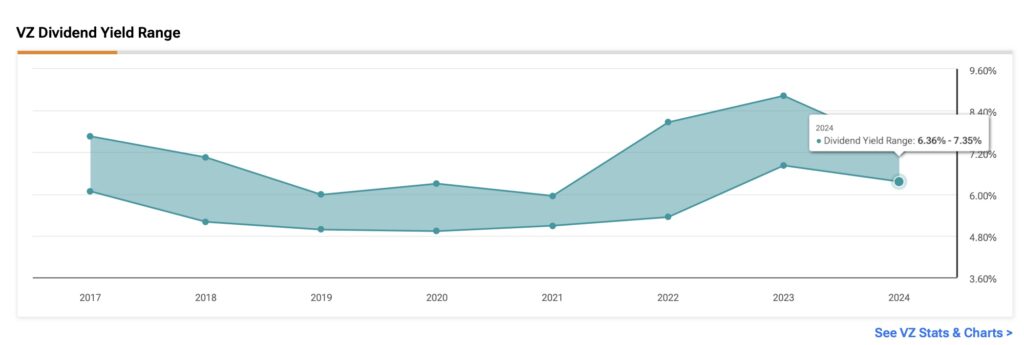

Despite these challenges and the stock’s devaluation, Verizon remains a long-term dividend grower, though at a modest growth rate of 2.7% over the last 20 years. Currently, Verizon’s dividend yield is 6.5%, which is well above the telecom industry average of 2.5% and slightly higher than AT&T’s (NYSE:T) yield of 5.9%.

In 2023, Verizon distributed $11 billion in dividends, which represented 85% of its free cash flow. This is a significant increase from five years ago, when $10 billion in dividends accounted for only 50% of its free cash flow. This shift may explain Verizon’s recent years of underperformance. In comparison, AT&T used only 38% of its free cash flow for dividends in 2023 despite similar financial pressures in 2022. It is also worth noting that in terms of GAAP net earnings, Verizon’s payout ratio is 56.8%, higher than AT&T’s 47%.

Verizon’s management highlighted in the most recent earnings call that CapEx spending was $4.4 billion in the March quarter, down from $6 billion the previous year. This reduction aligns with Verizon’s goals of enhancing free cash flow and deleveraging. Consequently, Verizon’s dividends should remain stable, offering an attractive yield.

Importantly, Verizon’s CEO Hans Vestberg stated, “We have struck a balance between profitable growth and free cash flow that supports both our dividend and a stronger balance sheet. This gives us greater flexibility to accelerate deleveraging throughout the second half of the year, bringing us closer to our long-term leverage targets.”

VZ: A Strategic Stock to Own

In the current bull market, where AI stocks surge double or even triple digits over a year, it might be hard for investors to get excited about buying Verizon stock.

However, I believe that even growth-focused investors should consider VZ stock strategically as an essential defensive holding during turbulent times. In a diversified portfolio, Verizon stock can offer benefits due to its low correlation with the S&P 500, maintaining a low beta of 0.4 over the last five years.

With Verizon stabilizing its investment spending and returning to previous levels of free cash flow, investors can feel reassured by its stability, which supports a defensive investment strategy bolstered by robust dividend payments. The enticing and relatively secure dividend yield of 6.5% is notably two percentage points higher than the 30-year Treasury rate.

Is Verizon Stock Attractively Priced?

As Verizon stock trades at a forward P/E ratio of almost 8x, it is trading 10% below its average over the last five years. This presents a potentially attractive entry point, especially given the stock’s historically low volatility profile.

However, investors need to set their expectations accordingly, recognizing that Verizon is not a growth story, much like AT&T, which trades at a forward P/E of 8.4x. This explains the discount to rival T-Mobile (NASDAQ:TMUS), which is now the market favorite. T-Mobile has grown 140% in the last five years, while Verizon and AT&T have shrunk in value. T-Mobile’s 19x forward P/E is justified by expected EPS growth of 23% by the end of 2024 and 20% by the end of 2025. However, it is certainly not a compelling dividend payer, as it yields 1.1%.

Focusing on a strategic portfolio, which involves playing defensively, is often more important than choosing the highest growth stock. For this reason, I believe that Verizon, delivering predictable dividends, regaining its free cash flow, and trading at a discounted valuation, is a great option in this case.

Is VZ Stock A Buy, According to Analysts?

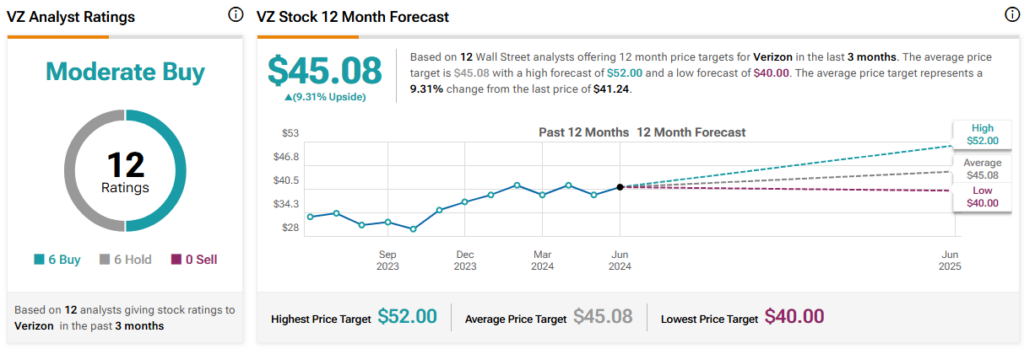

Overall, Wall Street analysts hold a cautiously optimistic view on Verizon, with a Moderate Buy rating. Among the 12 analysts covering the stock, there are six Buys and six Hold ratings. The average price target for VZ stock stands at $45.08, suggesting a potential upside of 9.3%.

The Bottom Line

Considering Verizon’s defensive stock profile, low volatility, and minimal correlation with the broad market, adding it to your portfolio could be a savvy strategy.

Despite recent challenges that have somewhat disrupted its historically low volatility and affected cash flows, Verizon has continued to grow its dividend distributions. The debt load should still be monitored closely, but it appears that Verizon is gradually returning to normalcy in its cash flow generation.

I believe the optimal time to invest in a stock with this profile is when its valuation is at a historical discount, as it is currently. Therefore, I view Verizon as a Buy today.