Taiwanese chip giant Taiwan Semiconductor Manufacturing Company (TSM), otherwise known as TSMC, has seen its stock fall around 30% from recent highs, creating what I view as an attractive entry point ahead of its Q1 2025 earnings report this coming Thursday. The company remains at the epicenter of a geopolitical tussle likely to send economic tremors worldwide, so its latest performance is considered a leading indicator and a barometer for the entire semiconductor sector. Despite near-term market jitters, I remain convinced that the stock is undervalued at ~$150 per share. TSMC’s dominance in AI chip manufacturing, accelerating revenue growth, and large-scale capacity expansion continue to support my Strong Buy rating.

AI Demand Fuels TSMC’s Growth

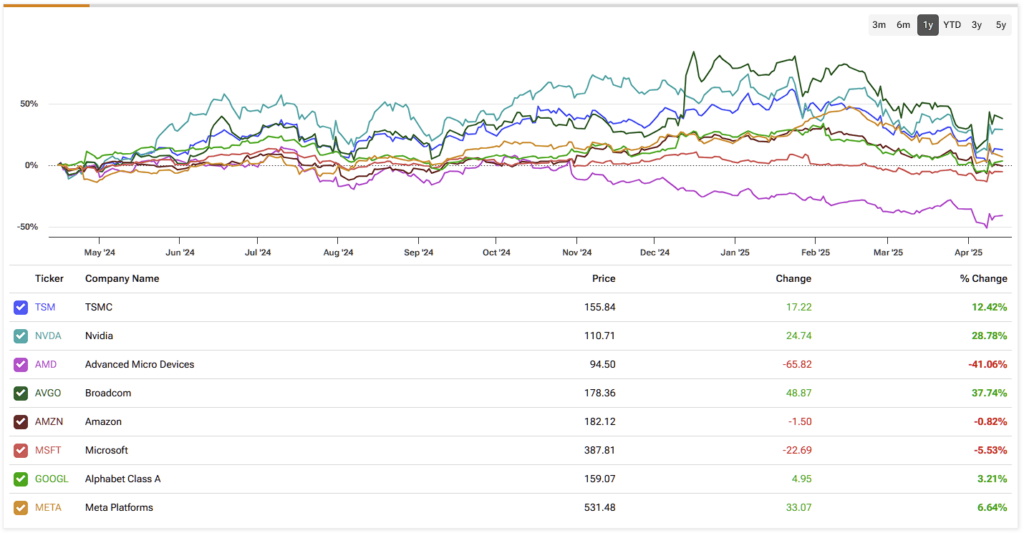

TSMC plays a central role in powering the global AI boom. It is the primary manufacturer of advanced chips used in artificial intelligence, and the world’s top semiconductor designers rely on its foundries. That includes Nvidia (NVDA), Advanced Micro Devices (AMD), Broadcom (AVGO), and even hyperscale cloud players that are building custom silicon. All roads in AI chip production lead to TSMC.

Recent reports show that Nvidia alone has secured over 70% of TSMC’s advanced CoWoS packaging capacity for 2025, underscoring the overwhelming demand for next-generation AI GPUs. Shipments of these chips are projected to grow more than 20% per quarter, with annual shipments set to exceed two million units—a powerful signal of the strength of the AI cycle. AMD is also ramping up orders for its central processing units and Instinct MI300 accelerators, and together with Nvidia, it has essentially filled TSMC’s advanced packaging schedule through 2025.

It’s not just the traditional chip firms driving this demand. Hyperscalers like Amazon’s AWS (AMZN), Microsoft (MSFT), Alphabet (GOOGL), and Meta (META) are aggressively expanding their AI infrastructure. These companies are investing billions to secure capacity for proprietary custom AI chips that can be sold to other businesses or end-users.

TSMC’s Earnings Show Momentum and Resilience

TSMC’s latest financial performance confirms that this surge in AI demand is translating into real earnings power. Preliminary revenue for the first quarter of FY2025 was up 42% year-over-year. That kind of growth is remarkable for any company—let alone a mega-cap name in a sector that saw mixed demand just a year ago.

Analysts expect the bottom line to show similar strength when the company formally reports earnings on April 17th. Consensus estimates point to a 54% jump from last year—a net profit of around $10.7 billion for the quarter. These figures illustrate how effectively TSMC captures gains from AI and high-performance computing trends.

Much of this strength stems from TSMC’s ability to command premium pricing for its cutting-edge chips. With limited competition at the leading edge, the company is well-positioned to sustain healthy margins. Given the strong start to the year and the deep backlog of AI-related orders, I expect management to provide a confident outlook for the remainder of 2025.

The company’s balance sheet also remains a source of strength, with about $75 billion in cash and short-term investments at the end of FY2024. That liquidity supports its aggressive capital expenditure plans while enabling it to return capital to shareholders through dividends.

Geopolitical Tensions Create Risk With Strategic Opportunity

Of course, no analysis of TSMC would be complete without addressing geopolitical concerns. The company’s location in Taiwan has long been considered a risk, especially given rising tensions between the U.S. and China. Those concerns are valid and partly explain why TSMC sometimes trades at a discount relative to its growth profile.

That said, TSMC is not standing still. It has made significant strides in diversifying its manufacturing footprint, with new fabs under construction in the U.S., Japan, and potentially Europe. These moves serve two key purposes: first, they reassure governments and customers that TSMC can continue operating in a crisis scenario; second, they align the company with Western policy priorities.

The company’s U.S. expansion is particularly significant. Its partnership with the U.S. government, which could involve up to $165 billion in investment across multiple U.S. sites, reflects a deepening strategic relationship. As Western countries continue to prioritize semiconductor independence, TSMC’s global expansion could yield not just operational resilience but also geopolitical goodwill. While ongoing discussions about tariffs remain fluid, TSMC’s growing U.S. presence makes it more likely to receive favorable treatment from policymakers.

Is TSMC a Buy, Sell, or Hold?

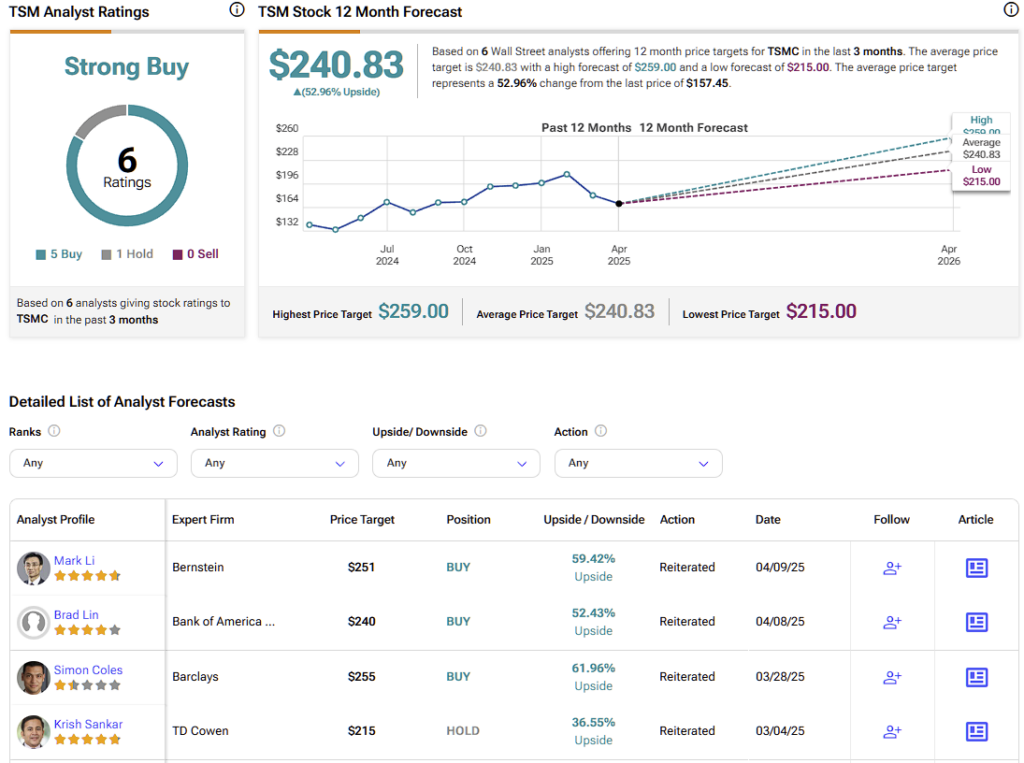

On Wall Street, the sentiment around TSMC remains strongly positive. The stock currently holds a consensus Strong Buy rating, with five analysts rating it a Buy, one assigning a Hold, and none suggesting a Sell. The average TSM price target is $240.83, implying a 53% upside from current prices.

I am maintaining my price target of $237.50, based on a 25x price-to-earnings multiple applied to projected earnings per share of approximately $9.50. This forecast supports the case for more than 50% upside.

True Bellwether in the AI Era

TSMC’s current share price does not reflect its long-term earnings potential or its unique role at the center of the global AI revolution. The company is unmatched in its ability to deliver high-performance chips that power everything from generative AI to data center accelerators. Its long-term contracts, booked capacity, and customer lock-in give it a level of visibility few peers can match.

While macroeconomic and geopolitical headlines can create short-term volatility, TSMC’s earnings trajectory remains intact. The blowout 42% year-over-year revenue growth in Q1 clearly signals that AI-driven demand is not just a theme—it is translating into actual financial outcomes.

For long-term investors willing to look past near-term noise, TSMC represents an opportunity to own a core player in one of the most transformative technological shifts in decades. I see the recent pullback as an opportunity in disguise—one that offers an attractive entry into a high-quality compounder with years of growth still ahead.