PayPal (PYPL) stock has been at the forefront of financial technology for decades. Since the days of the infamous ‘PayPal Mafia’, which launched the careers of some of the most influential people in business, including Elon Musk, Peter Thiel and Reid Hoffman, the company has evolved significantly. Despite growing competition, the company is demonstrating that it can navigate an increasingly complex financial world, making me bullish that the great run seen in 2024 can continue in the year ahead.

Confident Investing Starts Here:

- Easily unpack a company's performance with TipRanks' new KPI Data for smart investment decisions

- Receive undervalued, market resilient stocks straight to you inbox with TipRanks' Smart Value Newsletter

PayPal at a Glance

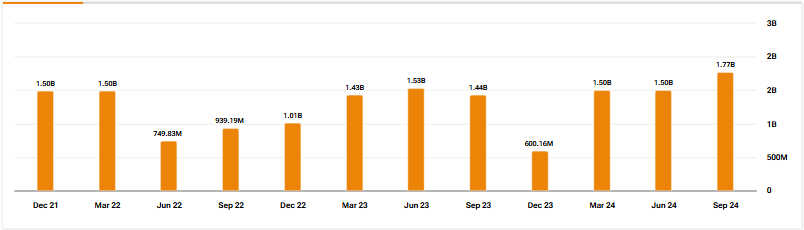

Since its founding in 1998, the company has been one of the key players in building out digital payment systems and now operates as an established platform across branded checkouts, peer-to-peer transactions, and unbranded card processing. With over 430 million users, and Q3 2024 total payment volume of $422 billion, it’s now a critical part of the domestic and international financial ecosystem.

My bullish perspective on PYPL stock is supported by some impressive trends in management’s latest release, with steadily increasing revenues, 22% growth in earnings per share (EPS), and free cash flow up 31% and now at $1.45 billion. With competition moving in from multiple angles, management is clearly looking to strengthen the balance sheet, with some aggressive moves to buy back shares and capture value as the company matures.

Shares outstanding were reduced in 2024 by 7%, with $5.4 billion in stock repurchases. Admittedly, this could have been used for further innovation or for moving into new markets, but I don’t mind seeing management seizing an opportunity when markets might be undervaluing the company, even after a healthy rally.

A Lasting Moat

There is no shortage of competition in the digital payments space, but I think PayPal has some major advantages. While Apple Pay (AAPL) clearly offers seamless integration with the iOS system, and Shopify Payments (SHOP) link with established merchants, I think PayPal can offer more across the full range of customer and business finance.

With customer offerings beyond the well-established branded checkout systems, to peer-to-peer payments, and innovative financing including buy-now-pay-later (BNPL), the platform can offer much more than just processing transactions. Links to other markets such as cryptocurrencies, managing subscriptions, as well as emerging partnerships with brands demonstrate there is plenty of potential still out there for scaling the ecosystem.

Despite the company being one of the more established in the sector, the commitment to ongoing innovation shouldn’t be underestimated. As more agile start-ups push for market share, PayPal has been able to rollout a range of new tool and system solutions to fend off this threat for now. One I see as being a major win is Fastlane, a guest checkout solution developed by partners to simplify the checkout process, and personalize the experience regardless of the vendor.

Capabilities and Valuation

As well as innovating new products, I’m impressed by the scale of development in some of PayPal’s most popular ones. Where Venmo was once a fairly basic transaction provider, it now enables merchant payments through the launch of the Venmo debit card, competing directly with traditional banks. This pivot towards personal finance opens up enormous opportunities for enabling investing across a range of assets, omnichannel spending through PayPal Everywhere, and rewards to build lasting connections with users.

The scale of this market has been reflected in the share price of late, partially offsetting the sharp decline seen in 2021 as interest rate hikes began. Despite a 45% return in 2024, the shares are still 22% below where they were five years ago. I see this as the company maturing from a hyper-scale growth company to a more established firm in the fintech space.

Many investors will consider fintech companies as having generally large valuation metrics, but PayPal’s price-earnings (P/E) ratio is only slightly above the sector median at 21.7. I think it’s worth noting this is below many of the more traditional payment providers, with potentially fewer capabilities for further monetization and innovation.

I think there is still plenty of upside ahead for the company, with the P/S ratio well below historical averages at just 2.77. With this as high at 14.52 in 2021, the market has potentially now repriced the company, and may be underrepresenting the scale of opportunity ahead.

Is PYPL Stock a Buy?

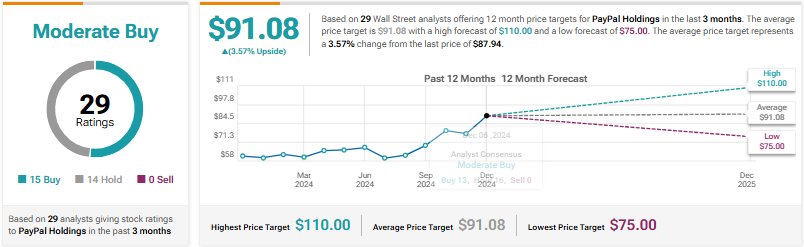

Wall Street seems to share a fairly cautious but optimistic view of the company, with a balance of Buy and Hold ratings going forward. This largely makes sense with an average price target of $91.08 only 4% above current levels.

Potential Risks for PayPal

Despite these inherent strengths, there are plenty of risks with PYPL stock for investors to consider. Regulatory pressures are ever-present as the firm continues to expand across new international markets. Complying with some of these complex legal protections, such as Europe’s General Data Protection Regulation (GDPR), is a major challenge. Working with emerging financial regulation in the cryptocurrency space and other dynamic opportunities are also likely to require some close focus over the next decade.

As established as the company is, there may also come a point where customer acquisition becomes a real challenge. To some degree, this is already underway, with only 1% growth in the last year. As long as revenues and earnings continue to grow, this may be less of an issue, but markets will be looking far into the future, and a slowdown in this metric could easily lead to a decline in guidance.

With pricing pressures from competitors, and an economy dealing with interest rate changes, a challenging inflation dynamic, and volatile consumer spending, management will need to be careful how any future changes are rolled out. Any negative trends in payment volume or usage could again lead to a change in investor confidence.

Conclusion

Overall, I’m bullish on the next few years for PayPal and its stock. The company is no stranger to uncertainty, having negotiated plenty of challenging markets and events throughout its history. But, with an innovation-led approach and improving balance sheet, I think there’s a lot to like here. Of course, there are challenges around regulation and competition, but with an enormous user base, and the agility to enter new markets and build partnerships, I see management having all it needs to succeed.