The iconic athletic brand Nike (NKE) has faced significant challenges this year, severely underperforming the broader market due to macroeconomic pressures, increased competition, and a lack of innovation under its previous management team. As Nike approaches the release of its Fiscal Q2 earnings on December 19th, I have a neutral outlook on the stock. Much of my caution aligns with the bearish sentiment from analysts who have lowered their expectations, acknowledging that any potential turnaround for Nike is likely to resemble a “marathon” rather than a “sprint.”

In this article, I will outline the reasons behind Nike’s struggles in recent years, what to expect for its Fiscal Q2 results, and why, despite trading at its lowest valuations in the past three years, it’s still prudent to exercise caution.

What Is Behind Nike’s Lackluster Performance?

Before diving into why I maintain a neutral stance on Nike, it’s important to understand the reasons behind the company’s disappointing performance in recent years. Over the past five years, Nike’s stock has fallen by 21.5%, and in 2024 alone, NKE shares are down nearly 28% year-to-date.

Let’s start by examining Nike’s growth metrics. Over the past three years, the company has grown its top line at a modest compound annual growth rate (CAGR) of 2.7%. Meanwhile, its operating profit (EBIT) has contracted at a CAGR of -5.7% during the same period. One of the key challenges has been intensifying competition, with rivals like Hoka, On (ONON), and Lululemon (LULU) gaining market share and eroding Nike’s position.

Under former CEO John Donahoe, Nike focused heavily on its direct-to-consumer (DTC) strategy but struggled to maintain strong relationships with its wholesale partners, including Foot Locker (FL) and department stores. This shift to a DTC model has hurt the company’s performance, as these relationships have historically been vital to Nike’s growth.

Additionally, Nike currently trades at a forward P/E ratio of 28x, compared to the industry average of 18x. While this is the lowest multiple the company has seen in three years, it still trades at a premium to the industry despite struggling to meet the growth expectations that typically justify such valuations. This discrepancy adds a layer of concern among investors.

Nike’s Q2 Sentiment Remains Cautiously Pessimistic

As Nike prepares to report its November quarter earnings on December 19th, I remain cautious on the stock due to the prevailing bearish sentiment leading up to the earnings release. Over the past month, three analysts have lowered their price targets for Nike, reflecting concerns that the company’s turnaround may take longer than initially anticipated.

In terms of projections, all analysts covering the stock have revised both revenue and EPS expectations downward for Fiscal Q2, as well as for Fiscal 2025, which ends in May. For Fiscal Q2, analysts expect Nike to report EPS of $0.65, representing a 37% decline compared to the same quarter last year. On the revenue side, Nike is projected to generate $12.18 billion, a year-over-year decrease of 9%. These figures are certainly concerning.

However, there is some optimism in the longer term, as analysts forecast revenue and EPS growth returning in Fiscal 2026, with projected increases of 4.6% in revenue and 16.5% in EPS.

What Nike Is Doing to Turn Things Around

Despite my neutral stance on Nike, the company has been actively seeking drastic measures to turn its business around as quickly as possible. One of the most significant changes has been the appointment of Elliott Hill as CEO, replacing John Donahoe. Hill, who began his career at Nike as an intern 35 years ago, now faces the challenging task of overhauling the company’s strategy. This includes changes to the product development cycle and rebuilding relationships with wholesalers, a process that typically takes time to yield results.

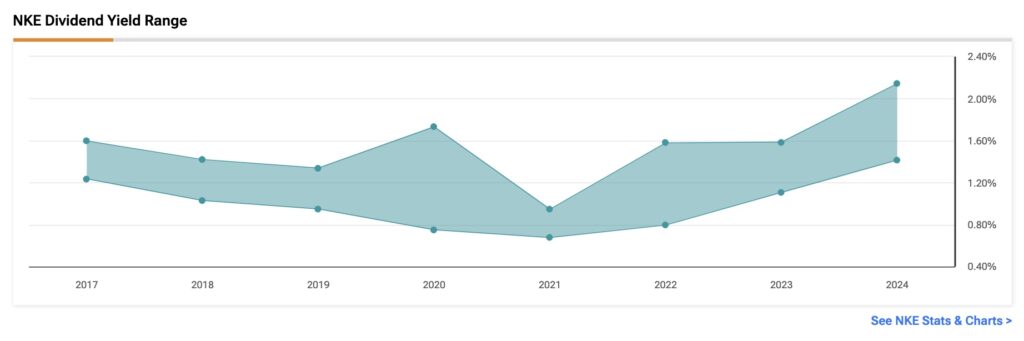

In addition to leadership changes, Nike has been focused on increasing shareholder returns in an effort to restore market confidence. The company has a strong track record of raising dividends, having increased its dividend payout for 22 consecutive years. In Fiscal Q1, Nike announced $558 million in dividends, marking a 6% increase from the previous year. At the same time, the company repurchased $1.2 billion in shares as part of its ongoing four-year, $18 billion buyback program.

Currently, Nike offers a dividend yield of 1.88% and a buyback yield of 3.7% over the trailing twelve months. These efforts reflect the company’s commitment to enhancing shareholder value, even amid its ongoing struggles.

Is Nike Stock a Buy, Sell, or Hold?

According to TipRanks, the consensus rating for NKE is a Moderate Buy. Out of 28 analysts covering the stock, 15 give a Buy rating, while 13 maintain a Hold stance. The average price target for NKE is $90.81, implying an upside potential of 18.33% from its current price.

According to TipRanks, the consensus rating for NKE is a Moderate Buy. Out of 28 analysts covering the stock, 15 give it a Buy rating, while 13 maintain a Hold stance. The average NKE price target is $90.81, implying an upside potential of 18.33% from its current price.

Conclusion

I have a Hold stance on Nike ahead of its Fiscal Q2 earnings, due to a largely negative outlook driven by a series of execution failures and an inability to adapt to macroeconomic conditions. While I believe that Nike, under new management, will eventually experience a turnaround, the key question is how long it will take. At this point, I don’t see any clear indicators in the upcoming quarter that would provide an answer.

Therefore, I would wait for stronger evidence of improvement in both the top and bottom lines before adopting a more optimistic view on Nike, even though current valuations are at their lowest level in the past three years.