Shares of top video streaming firm Netflix (NASDAQ:NFLX) have nearly recovered all of the ground lost after pandemic tailwinds started fading in late 2021 and early 2022. The implosion saw NFLX stock shed 75%, while the rally off the lows of June 2022 has seen 270% in gains. However, I’m still bullish on the stock, and I believe Netflix looks primed for higher highs in the second half of this year as it incorporates new technologies, content types, and impressive ad strength to keep the good times rolling.

Undoubtedly, the economic reopening from COVID-19 was a painful time to be caught hanging onto Netflix stock. Amid the carnage in the stock, Netflix seemed unworthy of joining the likes of the mega-cap tech stars from FAANG, all of which are now part of the Magnificent Seven.

Further, when Reed Hastings left the CEO’s office, there were signs of smoke, but the smoke had since cleared up. The company has been a force in the ad business with a content strategy that’s allowed it to stay ahead of streaming peers. Until now, there hasn’t been a worthy rival to replicate Netflix’s profound success. And I’m not sure if there ever will be as many streamers moving forward with what appears to be a “year of efficiency.”

Netflix Is Still the King of Streaming Value for the Masses

At this point in the inflationary surge, consumers have shown that they’re not afraid to take their money elsewhere if price hikes don’t also accompany more or better video content. For streamers, that perceived value is likely in the form of content spending. Netflix not only has the ability to create binge-worthy content, but it seems to have a wide enough breadth of content such that just about anybody is bound to find something they simply need to watch.

Whether Netflix subscribers are horror fans, documentary buffs, psychological thriller enjoyers, comedy lovers, epic film viewers, cartoon spectators, or reality TV show couch potatoes, Netflix seems to have more than enough to cater to the masses. Given each household has individuals with their own tastes, it only makes sense for a streamer to cover as many viewers as possible. Indeed, Netflix has all bases covered when it comes to content categories, something that many of its top peers have simply lacked.

For instance, Disney’s (NYSE:DIS) streaming platform Disney+ seems to be a hit with younger audiences for its massive library of family-friendly content. But beyond cartoons and prototypical Disney musicals, there just isn’t as much covered from a categorical standpoint. Moving ahead, Disney needs to better cater to other demographics if it wants to achieve Netflix-like success.

Of course, rolling Hulu (or Star in Canada) into the Disney+ package changes things a bit, but I think it’s safe to say Disney has a lot of work to do if it wants to seriously put a dent in Netflix’s thick armor. The good news for Disney is that FX’s Shogun series is certainly a big step in the right direction. If Disney can lean more heavily on FX while potentially catering to adult audiences with the Star Wars franchise (the Andor series was quite gritty), perhaps Disney has the assets it needs to land a hook straight to Netflix’s chin.

Apart from Disney, though, I’m not sure if there’s a real credible threat to Netflix out there anymore — not while some struggle with debt and cash bleed. When you’ve got so many streamers with ugly balance sheets, the balance (forgive the pun) between investing in keeping subscribers happy and managing financial frailties starts to become like walking on a tightrope.

Indeed, Netflix doesn’t have the same problem as many of its rivals, some of whom may have thought getting into streaming would lead them on the yellow brick road. The company has a whopping $24.2 billion in content obligations to be spent on originals, a figure that will be hard for rivals to keep pace with.

Netflix’s Peers Are Crumbling Under the Financial Pressure

Netflix has total debt of $16.5 billion, which is far less than its peers that are a fraction of its size. At writing, fellow streamer Warner Bros. Discovery (NASDAQ:WBD) has $42.6 billion in debt on its balance sheet. Such a mountain of debt needs to be repaid sooner rather than later before financial pressure becomes uncontrollable. Unfortunately, there may be few options other than chipping away at the mountain, even if it means losing subscribers to Netflix for the time being.

Netflix’s magic formula (consistent content pipeline and personalized recommendations) has helped it stay ahead in a cutthroat industry. Maintaining a healthy balance sheet has also helped a great deal, allowing the firm enough flexibility to invest in areas where its rivals haven’t or can’t due to their hefty financial burdens. As some of Netflix’s top rivals begin to ease their foot off the pedal to stop the streaming of cash from their hands, perhaps Netflix will have ground to run farther ahead of its peers.

Whether it’s through adding gaming and live sports to the mix or better utilizing the company’s trove of subscribers to improve upon the personalization factor, it’s clear that Netflix plays chess while its foes play checkers. So, as some of Netflix’s rivals backtrack on their ambition, Netflix seems to be going full speed ahead with its coming Mike Tyson vs. Jake Paul event, a pricy event that many of its peers simply cannot afford at this juncture.

Netflix’s latest first-quarter showing was outstanding. Revenue surged 15% year-over-year to $9.4 billion, while earnings per share of $5.28 blasted past the $4.52 estimate. With 9.3 million subscriber adds for the quarter, it seems like there’s more to Netflix than just the password-sharing crackdown. It produces lots of content and spreads it efficiently across categories.

Is NFLX Stock a Buy, According to Analysts?

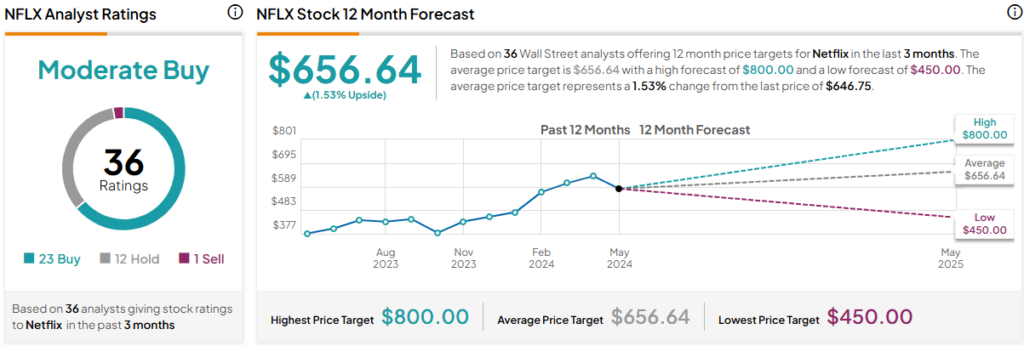

On TipRanks, NFLX stock comes in as a Moderate Buy. Out of 36 analyst ratings, there are 23 Buys, 12 Holds, and one Sell recommendation. The average NFLX stock price target is $656.64, implying upside potential of 1.5%. Analyst price targets range from a low of $450.00 per share to a high of $800.00 per share.

The Bottom Line on NFLX Stock

Undoubtedly, it was supposed to be Netflix’s throne to lose. However, moving ahead, Netflix looks poised to inflict pain on some peers who may be unable to keep up in the expensive and “churny” world of streaming. Its strong balance sheet, deep library of content spanning numerous categories, and smart managers will allow Netflix to grow as it puts many of its younger rivals on the ropes.