Over the past few years, I’ve consistently praised Meta Platforms (META) as my top stock pick, writing numerous articles on its remarkable upside potential. Even as the stock soared to new highs, I repeatedly argued it remained undervalued given its underlying growth prospects.

Meta remains my largest holding today, and its latest earnings report has only reinforced the conviction behind my Buy rating. The social media giant blew past analyst estimates a week ago, forcing Wall Street to reprice its valuation. Yet fundamentally, nothing has changed, as Meta’s growth story remains as strong as ever.

In fact, I believe that $1,000 per share is much closer than most investors realize.

In all fairness, many analysts have been bullish on META for a considerable time. Whenever rampant stocks reach for all-time highs consistently, the natural inclination is to expect a sell-off at some point, with the worst fears of buying the high (or selling the low) always lingering in the back of investors’ minds. META hasn’t seen a lower low since early 2023, and its climb higher is set to continue.

Meta’s Exceptional Growth Story Continues

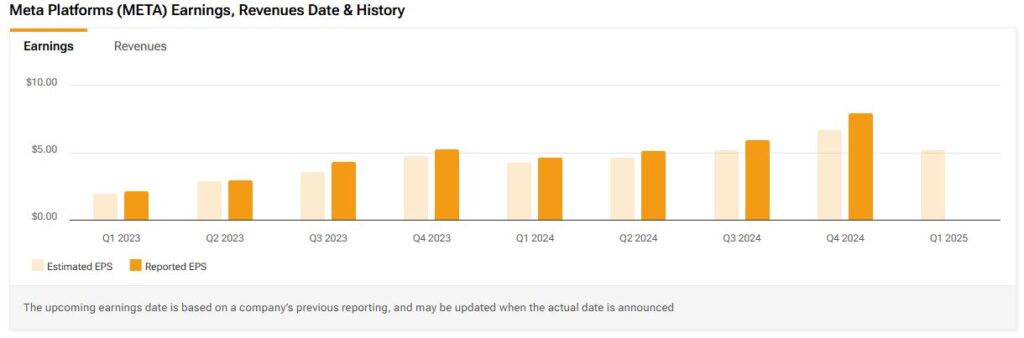

META wrapped up its FY2024 with another quarter marked by broad operational excellence. Revenues hit a record of $48.39 billion, celebrating a 21% increase year-over-year and topping expectations by $1.4 billion. This top-line growth, which even registered an acceleration compared to the prior quarter’s result of 18.9%, was again supported by excellent growth across Meta’s KPIs. Specifically, its Daily Active People (DAP) metric expanded to a record 3.35 billion, up 5% year-over-year. Further, there was a notable boost in ad impressions and pricing power, with the company delivering 6% more ads year-over-year, while the average price per ad climbed by an outstanding 14%.

Therefore, these results signal a strong demand for Meta’s advertising services besides maintaining exceptional user engagement and attracting new clientele (even with nearly half the globe signing into a Meta app daily). Management credited steady improvements in AI-driven ad targeting, which, in turn, translated into higher conversion rates for advertisers. Meta’s investment in advanced ad-ranking models powered by machine learning continues to pay off because they improve personalization and boost businesses’ return on ad spend.

Another strong theme has been Meta’s push into AI-generated content and automated ad optimization tools, particularly its Advantage+ suite. Advantage+ shopping campaigns alone have reached an annual revenue run rate of over $20 billion, growing at an impressive 70% year-over-year. From where I stand, I like that AI isn’t a marketing buzzword for Meta but a very real, foundational part of the business that makes its massive capital expenditure commitments worthwhile.

Ever-Surging Profitability and Expanding Margins

As thrilling as it was to see META’s top-line surging, its bottom-line growth was much more impressive. In Q4, operating income hit $23.4 billion, reflecting a 48% operating margin and a notable margin expansion from last year’s 41%. We can attribute this to several factors, including economies of scale, reduced legal expenses, and more efficient AI-powered ad delivery.

Thus, net income for the quarter came in at $20.8 billion, up 49% from the prior year, while EPS hit $8.02, a 50% year-over-year increase. The quarter, therefore, pushed META’s full-year EPS to $23.86, which I find pretty mindblowing, considering how mature of a business META should be by now. Further, these results totally shatter the old narrative pushed by the bears that META’s profitability might be at risk due to heavy investments in AI and Reality Labs.

Meta’s Cheap Valuation and Wall Street’s Mispricing

Despite this surge in profitability, I continue to view META stock as cheap relative to its overall growth trajectory. For starters, Wall Street’s current consensus estimates for FY2025 project only 6% EPS growth, which makes little sense given the company’s momentum. Based on management’s outlook and current trends, I estimate that META’s EPS can grow by at least 12% this year compared to 2024’s $23.86, which would amount to roughly $26.72.

Meta is trading at just 26x my projected 2025 EPS at its current share price. This is an extremely low multiple for tech behemoth that has compounded EPS at a 36% CAGR over the past decade. This is especially true today, as AI-powered monetization is comfortable driving higher ad engagement. Along with operating efficiencies boosting margins higher, I believe META deserves to trade at a much higher valuation multiple. A reasonable, in my view, re-rating to even a low-30s P/E multiple would indicate a significant upside. Hence, if the market starts pricing to the full extent of META’s AI-driven growth and its dominant position in digital advertising, we could see its stock trade well above $1,000 per share sooner than expected.

Is META Stock a Good Buy?

Despite the stock’s prolonged rally, analysts remain optimistic about META’s investment case. Over the past three months, Meta Platforms has gathered 44 Buy, three Hold, and just one Sell ratings, forming a Strong Buy consensus on Wall Street. Currently, META stock carries an average price target of $755.26 per share, implying a 7.25% upside potential from current price levels.

META’s Rally is Just Getting Started with $1,000 in Sight

I remain convinced Meta’s growth story is far from over. Its AI-powered ad capabilities, expanding margins, and upward user base and engagement trajectory position it for continued success. At the same time, its valuation multiples still fail to reflect its overall potential. Therefore, the path to $1,000 per share seems quite realistic to me, which is why META stock remains, by far, my largest holding.

META’s relentless climb since its recent lows in 2022/23 is no fluke. It demonstrates the company’s solid fundamentals and consistent innovations to keep it competitive in a busy marketplace. Despite setting record highs, the stock remains relatively undervalued. While some fear a pullback is just around the corner, META’s earnings strength and market adoption rates suggest otherwise. The path to $1,000 per share seems less like a case of if and more like a case of when.

Questions or Comments about the article? Write to editor@tipranks.com