Video game retailer GameStop Corp. (GME) is set to report its quarterly earnings results next week on March 25, and once again, the ride will be volatile. Although the company doesn’t provide any official guidance, estimates suggest that Q4 could mark the third consecutive profitable quarter, in line with the company’s goal of reaching breakeven. On the other hand, top-line losses are expected to continue, which shouldn’t surprise anyone at this point.

With GameStop remaining a highly speculative stock, a lack of clear catalysts ahead, and mixed technical signals, I believe this is a time to stay out of the GameStop trade and adopt a Hold position ahead of its earnings report.

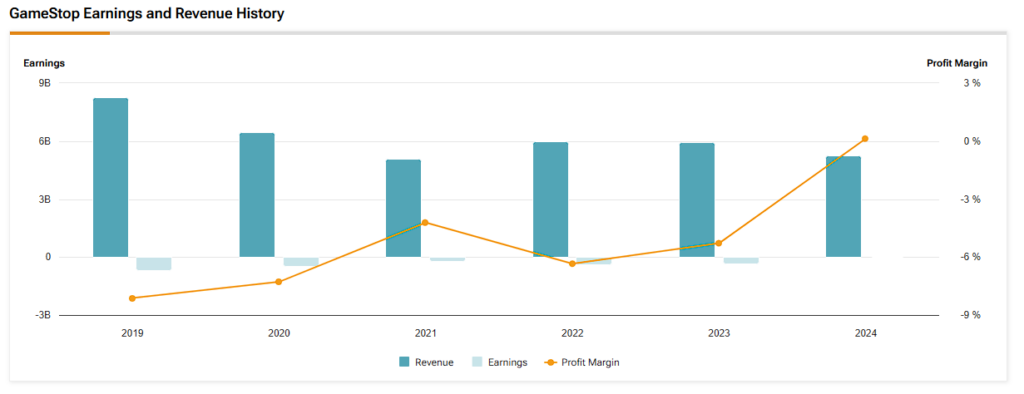

The stock has been on a roller-coaster ride for the past five years, reaching highs around $70 before collapsing and dropping to lows under $20 per share several times. All in all, GME stock is up 2,119% since 2020, demonstrating just how much potential it has always had.

Recently, the stock has slumped due to compounding factors, including online gaming, excessive overheads, and greater competition. The result has been a catastrophic sales decline since 2020. Despite GameStop’s sales decline, the company has a relatively strong balance sheet—thanks to stock dilution—and an extra cushion from short sellers since the company operating at breakeven is seen as somewhat stable. However, there are big expectations around whether CEO and major shareholder Ryan Cohen will use some of the company’s $4.5 billion cash horde to implement a turnaround story and reignite revenue growth.

Assessing GameStop’s True Value

Since becoming a meme stock, GameStop’s valuations have largely ignored the company’s fundamentals. Despite the massive cash infusion into its balance sheet in recent years through equity sales (especially in 2024 with Roaring Kitty’s return), the company’s ongoing revenue losses and breakeven margins make it hard to justify a market cap above $10 billion. There’s little clarity on how this can be turned around beyond cutting costs.

Using a reverse discounted cash flow analysis, GME’s fair market value is even more troubling than at first glance. Based on analysts’ projections for the next three years, GameStop’s revenue is expected to shrink at a CAGR of -7%. Without any new ventures beyond its declining core business, I find it hard to believe that GameStop’s operating margins will improve beyond breakeven. I estimate margins will stay at around 0.1%, which aligns with current levels. With a long-term growth rate of 2.5% and discounting cash flows at 7.5%, GameStop’s equity value would come out to around $6 billion, significantly lower than its current market cap of over $10 billion.

In other words, if GameStop’s business stays on its current trajectory over the next five years, using reasonable assumptions, the implied share price would be no higher than around $13.50—roughly 80% below its most recent price.

What to Expect from GameStop’s Earnings Next Week

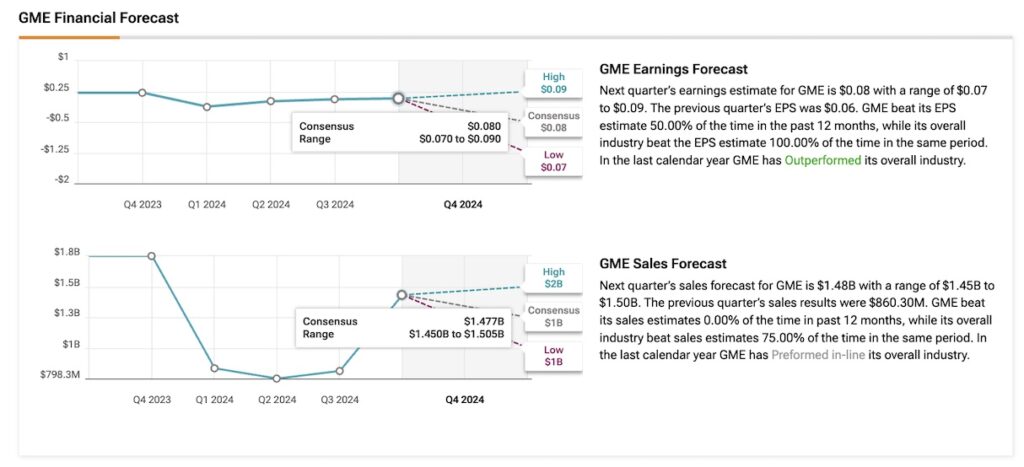

Although GameStop’s management team is known for providing minimal information with each earnings report, one of the few clear goals they’ve set is achieving profitability, primarily through super lean and frugal operations. As a result, there’s a consensus that for the current quarter, ending in January 2025 (the holiday season), GameStop could report another profitable quarter—despite declining sales.

To beat market estimates, GameStop would need to report EPS above 8 cents and revenues over $1.48 billion, implying an annual sales drop of nearly 18%. While this would certainly be bad news for any retailer, as it would mark the sixth consecutive quarter of sales losses—and double-digit declines at that—it’s important to keep the broader context in mind.

Since GameStop’s stock is heavily held by retail investors, it’s operating at breakeven. It has a significant cash balance; shorting the stock right now doesn’t seem reasonable, even if it makes sense from a valuation perspective. Additionally, while GameStop doesn’t typically host an earnings call, there’s always speculation about whether CEO Ryan Cohen will mention any initiatives to invest the company’s $4.5 billion cash war chest into something that could diversify or innovate its core business.

The most recent speculation was sparked by a photo of Ryan Cohen with MicroStrategy (MSTR) CEO Michael Saylor, which some saw as a hint that GameStop might be exploring the Bitcoin (BTC) space. A few days later, GameStop confirmed via X that it had received a letter from Strive Asset Management urging the company to adopt Bitcoin as a reserve asset. But so far, no actual initiative has materialized.

What the Charts and Options Are Showing for GameStop Stock

Given that GameStop’s business fundamentals are stable (though not exactly in a good way, but at least not deteriorating further), I don’t see any short- to medium-term catalysts that could push the stock price up or down based solely on the company’s core business.

Any potential new ventures the management team explores—like Bitcoin, for instance—are highly speculative. Rationally, they shouldn’t be the main reason for holding a long position in the stock. With that in mind, if you still believe GameStop stock is a tradeable asset, looking at technical metrics makes more sense.

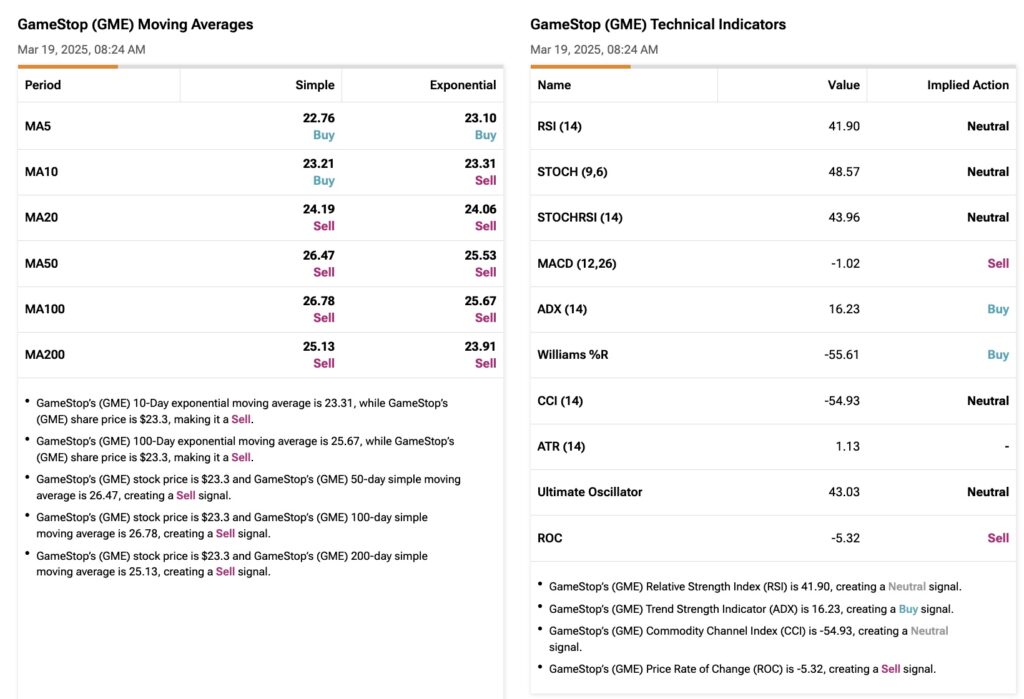

The stock trades below its long-term moving averages, signaling a bearish pattern. However, the short-term moving averages suggest the opposite, indicating some potential bullishness in the near-term trend. The RSI (Relative Strength Index), which is calculated based on GME’s price changes over the past 14 days, stands at 43. Since the RSI between 30 and 70 is considered a neutral zone, the stock is neither overbought nor oversold.

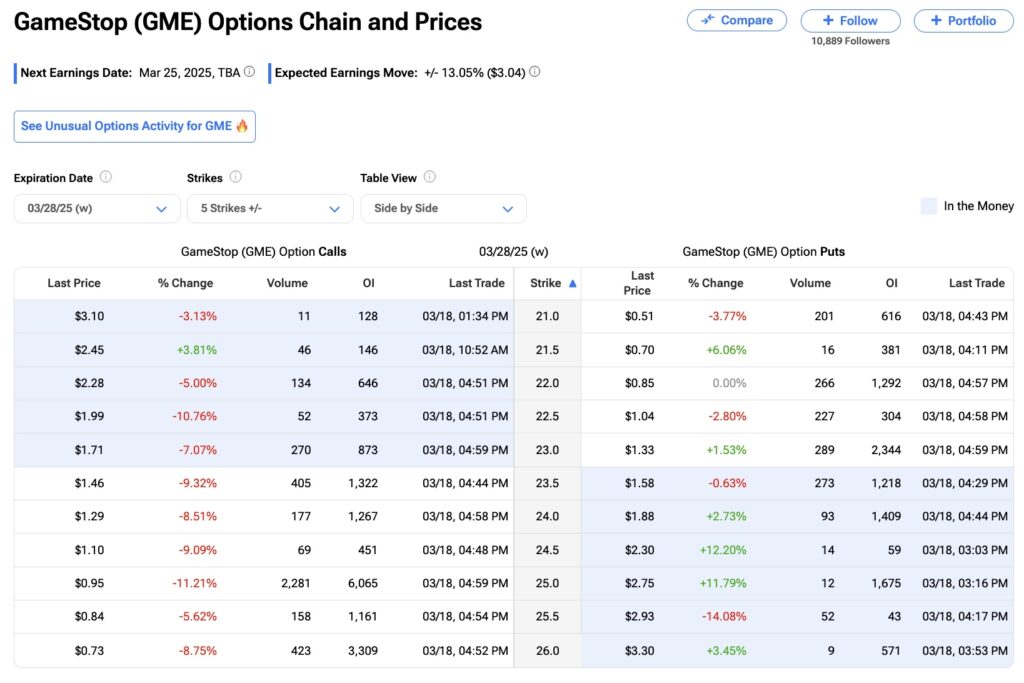

Additionally, looking at GameStop’s options chain, the at-the-money straddle calculations for options close to expiry after the earnings announcement suggest an expected earnings move of around 13%, given the cost of a call-put straddle is currently $3.04.

Is GameStop a Good Stock to Buy?

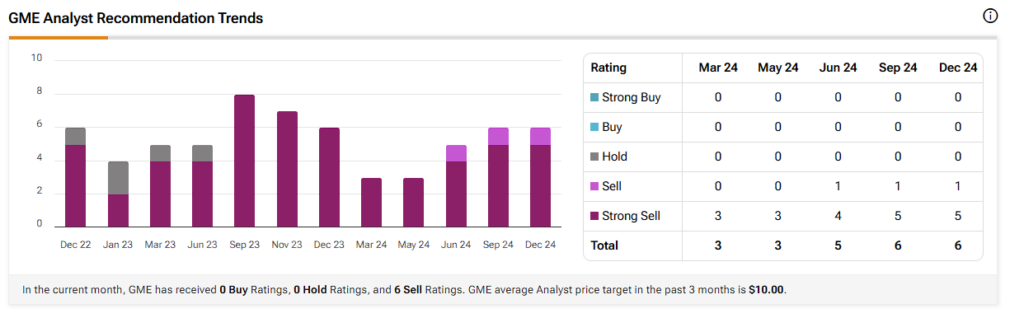

So far in March, GME stock has received zero Buy, zero Hold, and 6 Sell Ratings. The GME average analyst price target in the past 3 months is $10 per share, which implies more than a 50% decline in the company’s share price over the coming 12 months.

No Clear Triggers in Sight for GameStop

Even after the meme mania, GameStop stock remains a very difficult asset to understand. On one hand, valuations seem completely irrational, given the company’s breakeven margins and declining sales. On the other hand, the company has a lot of cash on its balance sheet and a management team that offers little clarity about what it plans to do with that cash, keeping bears uneasy about betting against it.

As a result, the stock is always surrounded by high speculation with every earnings report—not necessarily because of any changes in the top or bottom lines, but because of the possibility of a major announcement from CEO Ryan Cohen about the company’s future. With Q4 earnings just around the corner, volatility will likely play a role again. However, since there’s no clear indication of how the volatility will unfold, I believe it’s better to avoid GameStop stock for now.