After rising nearly 40% over the last 12 months, Costco (COST) stock has once again outperformed the broader market. It’s essentially a defensive stock that trades at growth-stock multiples. My bullish thesis on Costco remains strong going into 2025, thanks to its unique strategy that combines recurring revenue with stable profits from a highly loyal customer base.

Costco’s members are incentivized to buy in bulk at low prices, which helps drive the company’s continued success. With this strategy working so well, and Costco likely to weather any macroeconomic storm better than most other stocks, I see no reason for the bullish sentiment around COST stock to fade, despite its high valuation.

Costco’s Recipe for Success

My bullish view on Costco stock is driven by its low-margin, high-volume business, with membership fees driving profits. The membership model does more than just lock customers in. It creates a psychological trigger that encourages shoppers to visit more often to “get their money’s worth.” But what really sets Costco apart is how it has turned this model into a rare case of recurring revenue outside the technology industry. That said, this success only works because Costco executes its volume and pricing strategy better than just about any other retailer.

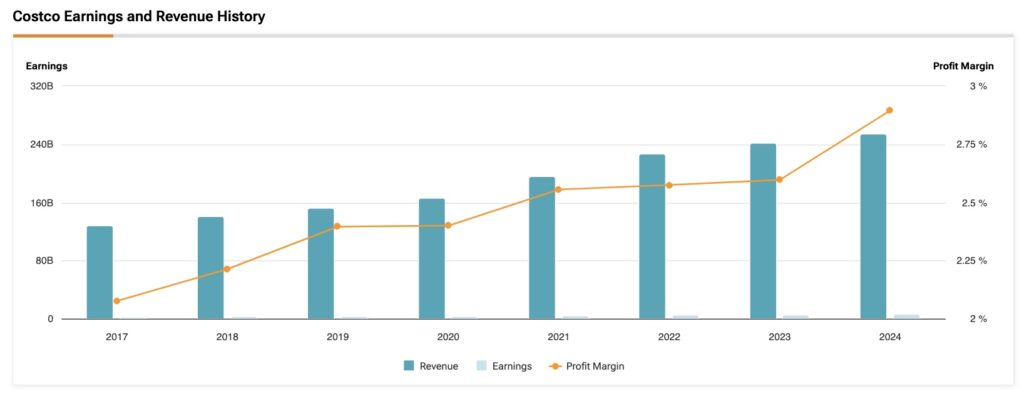

Now, let’s dive into Costco’s recent numbers. In its Fiscal year 2024 (which ended last September), Costco reported $254.4 billion in revenue and $9.2 billion in operating income, resulting in an operating margin of 3.6%. However, what’s key here is that $4.8 billion of that revenue came from membership fees, which, in theory, come with near-zero cost to the business—meaning virtually all of it is profit. Roughly 52% of Costco’s operating income comes directly from membership fees.

In short, Costco runs a remarkably sustainable, predictable, and profitable business. It can offer bulk merchandise at unbeatable prices, while still managing to keep slim operating margins (just 1.6% on sales) — all thanks to its membership fees.

A Defensive Favorite

Costco’s business model has made it a favorite among bulls, especially because of its defensive qualities. The company has managed to deliver stable profits even during tough macroeconomic conditions, despite low growth rates in certain periods.

Take Costco’s performance since 2019. Before the Covid-19 pandemic, Costco’s shares delivered an impressive 30.5% annual return, compared to just 13.4% for the S&P 500 (SPY) index. Even more notable is that Costco has maintained a low Beta of 0.79 over the past five years, meaning its stock has been relatively stable and less volatile than the broader market.

Looking at some risk and volatility metrics, Costco’s standard deviation at the period stood at 21.8%, and its maximum drawdown (the largest peak-to-trough decline) was 20.3%. By comparison, the S&P 500 had a standard deviation of 17.4% over the same period. So while Costco is slightly more volatile, its overall volatility is still moderate for a large-cap stock.

Given these factors, it’s been tough for the market to turn bearish on COST stock. Even with high inflation and rising interest rates in recent years, many investors have seen Costco as a safe haven for their money.

Costco’s High Valuation

If there’s one point of skepticism in my bullish view on Costco, and likely for many other bulls as well, it is the stock’s valuation. While Costco has delivered strong returns with relatively low risk across various macroeconomic conditions, it’s been trading at growth-stock multiples despite having modest growth rates.

Currently, Costco trades at 51.2 times its forward earnings, which is 28% above its five-year average. When we factor in the expected 9.4% earnings per share (EPS) growth over the next three to five years, Costco’s PEG ratio comes in at almost 5.5 times, which is roughly five times higher than Nvidia’s (NVDA) PEG. Arguably, these multiples are justified by Costco’s growing profits from its membership fees, which boast renewal rates above 90%. However, if those rates were to decline, leading to a drop in operating profits, Costco’s stock—trading at such a high multiple—could be vulnerable to a sharp selloff.

On the flip side, based on Costco’s track record over the past five years, maximum drawdowns have never exceeded 20%, even in the most volatile economic periods.

What to Expect from Costco in 2025?

Part of my continued optimism about Costco is based on the expectation that 2025 will likely be more of the same, which would be great news for COST stock. I don’t see any significant company-specific issues or broad market trends that would discourage investors from holding the stock in their portfolios, even with its stretched valuation. Throughout 2024, especially in the first half of the year, retail stocks struggled with slower consumer demand due to elevated interest rates. Many shoppers turned to retailers focused on value and essential items, boosting demand for companies such as Costco and Walmart (WMT).

Looking ahead, the outlook suggests that this strong demand will persist, especially as lower interest rates may encourage even more consumer spending. The latest December data, covering the holiday period, shows that Costco’s comparable sales rose 10%, reaching $27.52 billion during the five weeks ending January 5. Same-store sales across all of its locations increased by 7.4% year-over-year in December. A standout was e-commerce, which jumped 34.4% year-over-year.

In my view, e-commerce could be the key driver for Costco’s better-than-expected topline growth in 2025. Fiscal 2025 sales are expected to grow 7.1% year-over-year, and if online sales continue to perform well, Costco could exceed those expectations.

Is COST Stock a Buy?

At TipRanks, Costco has a Buy rating from 17 out of 25 analysts, with the remaining eight analysts taking a neutral stance on the stock. The average price target is $1,065.04, which suggests a potential upside of 14.85% based on the current share price.

Conclusion

Costco is likely the best retailer at executing the low-margin, high-volume strategy in the world. Combined with its membership fee model, this ensures the company generates stable profits even through different economic cycles. Of course, all that comes with a high price tag, so Costco’s potential for big gains over the near-term might be limited. Still, I remain confident that Costco is well-positioned for continued success in 2025 and beyond. Holding COST stock for the long-term still makes a lot of sense, especially given its impressive track record of outperforming the market.