Since its founding in 1963, Comcast Corporation (CMCSA) has been one of the world’s most dominant telecommunications and media companies. Offering investors a range of revenue streams, extending from high-speed internet services to content creation and distribution, the company recently posted some solid results. With record revenues, strong cash flow, and steady shareholder returns, the trajectory will encourage many, but not Charlie Munger.

However, investment goblins are lurking beneath Comcast’s shiny exterior, the most notable of which is the lack of a competitive advantage. Charlie Munger, the legendary investor and longtime partner of Warren Buffett, has always believed that firms must possess durable advantages that protect them from competitors. The value of a castle is ultimately determined by the value of its moat. Comcast’s moat has dwindled to a rivulet while a band of cordless competitors ride over the hill to sack the castle.

I suspect issues in the company’s financials and operations could lead to significant challenges over the next few years. As a result, I’m somewhat bearish on the shares and would recommend caution for potential investors.

Diving Deeper into Comcast

Companies like Comcast, with an enormous range of products and services, can often be challenging to analyze. However, breaking the firm into three key segments makes it slightly more straightforward to map out the future and likely next steps for the share price.

The Connectivity & Platforms division encompasses the Xfinity brand’s broadband, video, and wireless services, making up a large proportion of overall revenues. Media operations, mainly through NBC, include the firm’s cable networks, film production suite, and Peacock, the company’s move to enter the streaming industry. The third segment, Content & Experiences, which includes media giant Sky and Universal theme parks, has shown strong growth in recent years despite being vulnerable to changing consumer preferences.

The balance sheet remains relatively solid, with debt levels under control at a 2.3x net leverage and heavy investment in returning shareholder capital over the last year, with $8.6 billion in buybacks and $4.8 billion in dividends, with this expected to rise further in 2025, an impressive 17th consecutive increase.

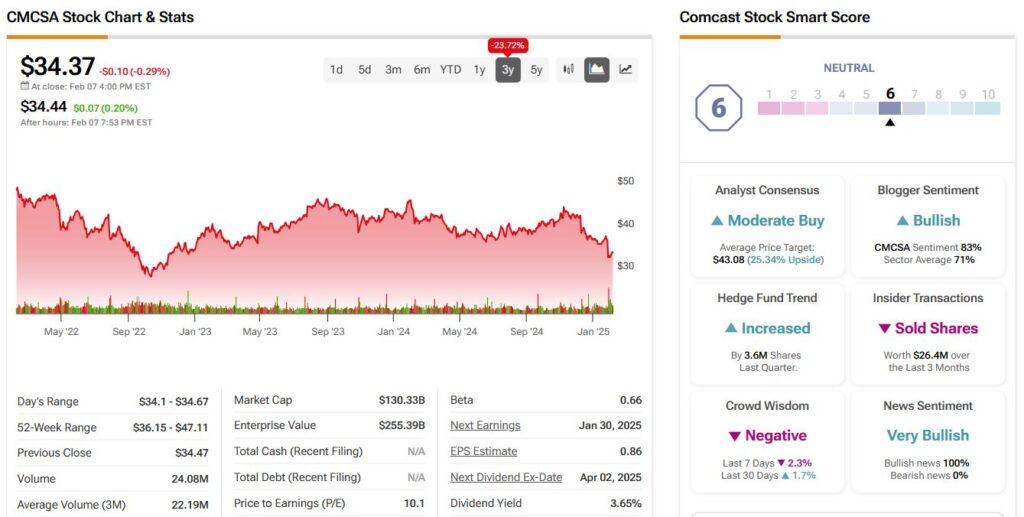

Despite this resilience and diverse incomes, many will suggest that the company’s core is too reliant on the U.S. Internet market, leveraging cable infrastructure while satellite technology continues to develop. Broadband subscriber losses of 139,000 in Q4 suggest this is well underway and could be a growing concern for investors, potentially reflected in the 20% drop in the share price over the last year.

Mixed Bags Spell Mixed Future for Comcast

The latest earnings report was a somewhat mixed bag for investors. As I noted, subscriber losses will be disappointing for the critical broadband market, but with a 2% increase in overall revenues, management may be pretty happy with stable growth. Adjusted EPS also beat expectations, and free cash flow allows management to reward shareholders and consider new opportunities.

While management may look to offset the losses in broadband subscribers with price hikes, attrition rates remain challenging. If markets become increasingly skeptical that this trend can reverse, then it could be hard to see any type of recovery in the share price over the near term.

Competition is likely one of the key reasons for this loss. With so many excellent services out there, customers have more choices than ever for how to spend their money, both in terms of infrastructure and entertainment. Fiber providers such as AT&T and Verizon are rapidly moving in on the company’s turf, building out infrastructure with far superior speed and reliability to traditional cable broadband. Comcast risks being left behind as the market evolves without significant investments in this technology. This is especially true as regulators push to expand the broadband landscape, potentially adding more competition and further challenges to the company’s pricing power.

Charlie Munger may have been right after all.

Looking at the streaming category, Peacock has shown some decent subscriber growth, up 16% in a year to 36 million. However, competitors such as Disney (DIS) and Netflix (NFLX) blow it away in scale and ambition, and the platform is still unprofitable, making it a challenging area for further investment. If the platform cannot turn this around soon, it may be forced to reconsider, potentially limiting the company’s reach in the fast-moving media landscape.

Strong on the Outside, Weak on the Inside Comcast Valuation

Of course, a company with an uncertain future can be an excellent investment if management can build a working strategy, but I’m not yet convinced. Despite a P/E ratio of just 10.1, there is no guarantee that the share price is in bargain territory yet. The dividend of 3.65% will turn a few heads, but I’d be concerned about focussing too much on income if the share price continues to slide over the coming years.

A discounted cash flow (DCF) calculation puts the fair value of the share price at about $62, an impressive 84% higher than the current level, but I fear this scale of upside in the market. Investors are unwilling to buy into a company that is so much lower than a basic fair value calculation, which suggests a lot of uncertainty is reflected. It can be challenging to shift unless the company can reinvent itself.

Is Comcast (CMCSA) Stock a Buy or a Sell?

On TipRanks, the CMCSA stock carries a Moderate Buy consensus rating based on 11 Buy, 11 Hold, and zero Sell ratings over the past three months. CMCSA’s average price target of $43.08 per share currently implies a 25.3% upside potential from current levels.

Although Wall Street’s price target could take a while to reach, we could see many more downsides before a protracted rally.

I’d be watching the broadband losses to indicate the next move. If management can turn the tide around and boost subscribers across services and platforms, this sector giant could still have plenty of good years ahead. However, if the more dynamic and technologically advanced companies can move in, its days could be numbered.

Comcast at a Crossroads

CMCSA is a global media powerhouse that provides broadband, wireless, and video services and produces, distributes, and streams entertainment, sports, and news worldwide. The company remains a giant in the sector, with enormous cash flow and appealing dividends.

However, the foundation of its success, namely in broadband, clearly shows a few cracks. The market has shown a healthy dose of skepticism in recent years with the firm, so while many will like what they see in the latest report, I’d encourage some caution going forward.

If Charlie Munger is correct about competitive advantage, then Comcast is the last stock investors should consider right now. Until the company can demonstrate a clear path to stabilizing its traditional segments and turning more innovative platforms such as Peacock into profit-makers, I imagine the risks will outweigh the rewards. Moreover, Comcast’s empire crumbles as content production and consumption are democratized simultaneously. The rivulet cannot stop the torrent.

I’m staying firmly bearish and recommend shareholders trim their positions while potential new investors are advised to take a neutral stance until strong catalysts emerge.

Questions or Comments about the article? Write to editor@tipranks.com