Chevron (NYSE:CVX) and Exxon Mobil (NYSE:XOM) are two renowned giants in the oil sector, attracting dividend-focused investors. As is customary in the oil industry, fluctuations in oil prices significantly influence the financial results of these companies, often impacting their dividend payouts. While I maintain a bullish outlook on both, a closer examination of their dividend yields, growth prospects, financial robustness, and business models may suggest that Chevron currently stands out as the superior choice for dividend-seeking investors.

Dividend Yield: Chevron Takes the Lead

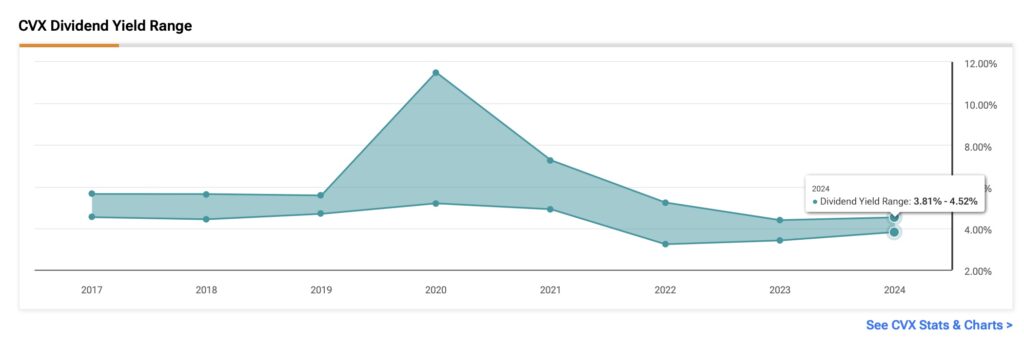

For investors seeking income stocks, dividend yield is a critical metric, indicating the ratio of dividend payments per share to the company’s current stock price. Essentially, it shows investors what they receive in dividends relative to the market value of the stock. When comparing Chevron and Exxon Mobil, Chevron currently offers a yield of 4.04%, whereas Exxon Mobil’s yield stands at 3.36%. Both yields are appealing, though, as they surpass the rate of the PCE inflation.

Leaving aside 2020 and 2021, when the logistical disruptions of the pandemic caused a sharp spike in oil prices and resulted in huge profits for oil companies, Exxon Mobil had a higher yield compared to its peer over the past five years. This higher yield from 2020 to early 2023 can be attributed to Exxon Mobil’s slightly stronger growth profile during that period.

However, the tables have turned recently, with Chevron consistently reporting a higher yield throughout 2023 and 2024, although the difference is marginal.

Overall, while the competition remains close, Chevron has now taken the lead in dividend yield, albeit historically, Exxon Mobil has held a slight advantage in this metric.

Dividend Growth: Chevron Wins Again

When examining dividend growth, which is as crucial as dividend yield, the comparison between Exxon Mobil and Chevron from May 2020 to May 2024 reveals significant differences. Exxon Mobil increased its quarterly dividend by approximately 9.2%, whereas Chevron achieved a robust growth of 26.3% during the same period.

This disparity in dividend growth can be attributed to Exxon Mobil’s historically aggressive investments in new projects, resulting in higher capital expenditures. In contrast, Chevron has maintained a more conservative approach to capital expenditures, prioritizing a balanced and less risky balance sheet.

At the risk of oversimplifying the analysis, assuming unchanged share prices, if Chevron maintains a similar growth rate over the next four years, its dividend yield could potentially reach 5.1%. Meanwhile, Exxon Mobil, with its current growth rate of 9%, would see its yield increase to 3.6% under the same conditions.

Financial Robustness: Exxon Mobil Wins This Time

When assessing a company’s ability to sustain dividends and grow them above inflation, financial robustness becomes crucial, focusing on metrics like free cash flow generation and the strength of its balance sheet.

In 2023, Chevron generated $20.4 billion in free cash flow, which was less than half of what it generated in 2022 due to the sharp rise in oil prices. Despite this, the free cash flow generated was 79% higher than the total dividend payments made over the past year. Analysts project a 1% decline in EPS for Chevron in 2024, ensuring at least a stable dividend payment despite the uncertainty surrounding the influence of volatile oil prices on distributions.

On the other hand, Exxon Mobil appears to be in a stronger position. Last year, the company reported $33.45 billion in free cash flow, which was 124% higher than the $14.93 billion paid out in dividends. This means that even if FCF generation declines due to oil price volatility, the company may still have plenty of cash available for distributing dividends.

Looking at its balance sheet, Chevron carries net debt of $15.5 billion, representing approximately 5.9% of its total assets. In contrast, Exxon Mobil’s $7.1 billion in net debt accounts for only 1.8% of its total assets.

While Chevron’s financial strength is solid and not far behind Exxon Mobil’s, the latter holds a clear advantage in this comparison. Nevertheless, both companies demonstrate strong dividend coverage and maintain robust balance sheets, which should support attractive dividend payouts.

Business Model Stability: Exxon Mobil Wins One More Time

Exxon Mobil and Chevron have distinct revenue structures. Exxon Mobil’s revenue comes from various sources, making it more diversified. The majority (around 80%) stems from energy products. However, Upstream operations contribute about 7% of total revenues, same as chemical products, and specialty products 6%. This diverse portfolio provides stability for Exxon Mobil, as it offers a cushion against sector fluctuations.

In contrast, Chevron’s revenue is simpler, with about 25% coming from upstream activities like exploration and drilling and a significant 75% percent from downstream activities such as oil and gas refining. A silver lining to this setup is that the reliance on downstream activities may benefit Chevron during high-demand periods for refined products.

Are CVX and XOM Stocks Buys, According to Analysts?

Wall Street shows bullish sentiment towards both Chevron and Exxon Mobil, though with varying degrees of optimism for each.

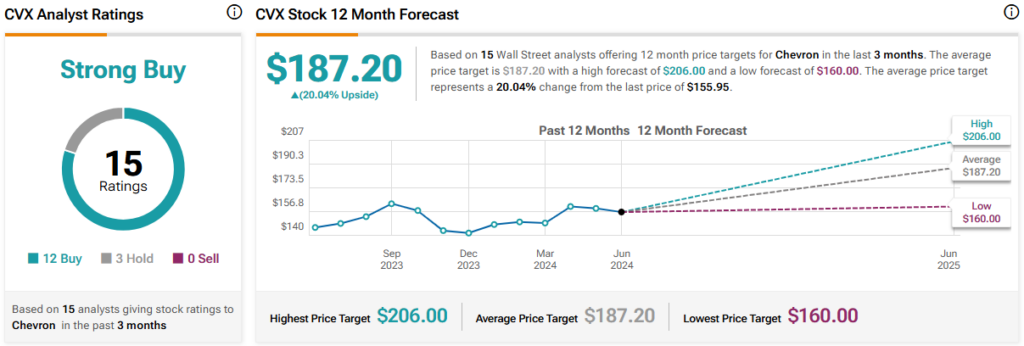

The consensus among Wall Street analysts regarding CVX is a Strong Buy. This is based on 12 Buys and three Hold ratings assigned in the past three months. The average CVX stock price target is $187.20 among 15 analysts, implying upside potential of 20%.

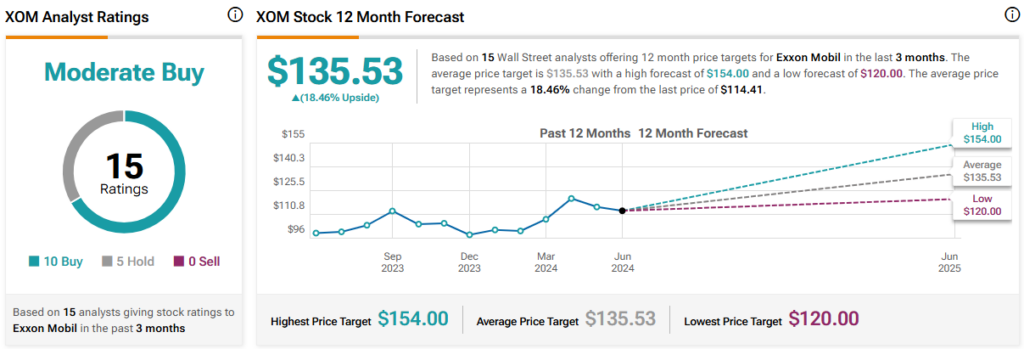

Regarding Exxon Mobil, the consensus is a Moderate Buy. Five analysts have rated Exxon Mobil as a Hold, while the remainder are bullish. The average Exxon Mobil stock price target among these 15 analysts is $135.40, suggesting upside potential of 18.5%.

The Takeaway

While I believe both Chevron and Exxon Mobil are strong dividend stocks suitable for any portfolio, Chevron currently appears to be in a stronger position. This belief is supported by Chevron’s history of more aggressive dividend increases and its robust financial strength, although not necessarily vastly inferior to Exxon Mobil’s.

Additionally, Exxon Mobil’s pricing model appears to offer more stability compared to Chevron’s, even though Chevron may perform better during periods of high demand for refined products.