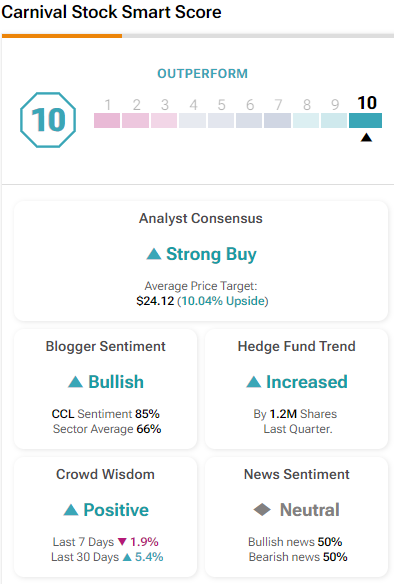

Carnival Corporation (CCL), a company that operates in the cruise ships industry, has a perfect rating of 10 on TipRanks’ Smart Score, reflecting strong analyst ratings, bullish blogger sentiment, and increased Hedge Fund activities. The company also possesses positive technical indicators and growing EPS. Additionally, CCL stock has climbed more than 60% in the past year, riding the wave of positivity surrounding the firm after its impressive return to profitability post-pandemic lows. Of course, this grand comeback coincides with the returning demand for cruise vacations after two years of ongoing lockdowns.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

However, a daunting debt load lurks beneath the surface of many investors’ optimism, threatening to rain on the parade. Carnival’s substantial debt of over $30 billion is a significant concern despite all the good vibes. Therefore, CCL seems to be a conflictual stock.

Our writer at Tipranks, Nikolaos Sismanis, has written extensively on CCL, and you can read about it right here.

Let’s examine three talking points on CCL and its conflicted situation:

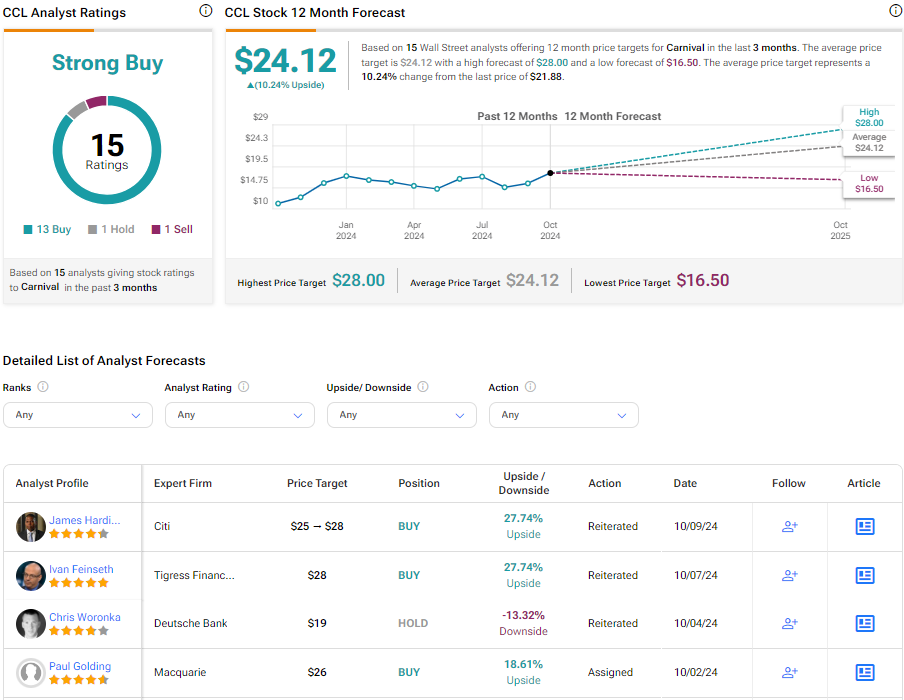

- Impressive Recovery and Profitability: Carnival Corporation has staged a grand comeback, rallying over 60% in the past year. The company’s return to profitability has allowed for this surge, with Carnival recording a net income of $1.7 billion in its most recent fiscal Q3, showcasing its resilience and effective strategy. The company forecasts its full-year 2024 adjusted EBITDA to exceed $6 billion, surpassing its pre-pandemic levels. This turnaround is by no means a small feat and has led to a Strong Buy consensus rating from Wall Street analysts, reflecting confidence in Carnival’s operations.

- Daunting Debt Load: Now for something entirely in opposition to the above, Carnival’s substantial debt load remains a concern despite its strong operational performance. The company had to raise over $19 billion in capital during the pandemic to cover its cash burn, resulting in a net debt of over $30 billion. While Carnival is generating record revenues and expected free cash flow of $2.7 billion this year, it will take years of disciplined deleveraging to bring its debt back to mitigating levels. This heavy debt burden limits its ability to reinvest in growth or return value to shareholders.

- Attractive Valuation and Long-Term Potential: This is where the conflicted reality of the company truly collides. On the one hand, Carnival’s stock trades at an attractive valuation, with a price-to-earnings ratio of 15.4x this year’s expected earnings and 12.1x next year’s estimate, meaning there’s room for further upside. However, the company’s heavy debt and the need for significant cash flow to service this debt limit its long-term growth potential. While the stock appears undervalued, much of Carnival’s future cash flow will likely be put toward debt repayment.

What Is the Price Target for CCL?

CCL is a Strong Buy on Wall Street, with 13 Buys, One Hold, and One Sell. The average price target for CCL stock is $24.12, reflecting a 10.24% upside.

Conclusion

While Carnival Corporation has demonstrated an impressive recovery with the return of cruise ship vacation demand, prompting good vibes all around, its $30 billion debt load is hovering above and presents a major challenge for the company’s finances. The stock’s attractive valuation and Strong Buy consensus rating from analysts highlight its potential. Still, its long-term growth prospects are in question, creating conflicting conditions for the company and investors.