As the holiday shopping season begins, Abercrombie & Fitch (ANF) has reported strong resilience during a challenging retail environment. Thanks to its strength and exceptional merchandise, the brand continues to shine, marking its sixth consecutive quarter of double-digit sales growth. The company posted top-and-bottom-line results that exceeded expectations for Q3, causing the company to raise its full-year sales outlook.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

Despite this optimistic performance, investors’ high expectations left the shares underperforming in the market. A perceived slowdown in growth caused a 5% drop in the share price immediately following the third-quarter earnings announcement. The stock is relatively undervalued compared to industry peers, making it a potentially appealing option for value investors interested in exposure to retail.

Abercrombie Posts Growth and Improved Efficiency

Abercrombie & Fitch is a market-leading, multichannel specialty retailer offering clothing and accessories through five notable brands for all ages. With a strong digital presence, its operations extend to over 750 physical stores worldwide.

The company has been focused on continued expansion, investing in its digital experience and planning to open 40 new Abercrombie and 20 new Hollister stores this year. The company’s brands are witnessing a healthy growth trajectory, with all regions seeing double-digit growth. Furthermore, the inventory turns have been increasing, representing replenishment frequency within a quarter.

In the past five years, Abercrombie maintained an average of 129 days of outstanding inventory, indicating the duration its inventory remained unsold. As of the third quarter of 2022, this metric was greater than 180 days. Since then, the company has shown significant improvement, as five out of the last seven quarters reported figures below the five-year average. This trend suggests an improved efficiency in the company’s operations compared to earlier years.

Abercrombie’s Recent Financial Results

The company just announced results for Q3 of 2024. Revenue increased by 14.2% year-over-year, hitting $1.21 billion and beating analysts’ forecasts by $30 million. Growth was experienced across all regions and brands, with Abercrombie brands delivering 11% comparable sales and Hollister showing a 21% increase. This strong growth resulted in a third-quarter operating income of $179 million, a 30% rise from 2023.

The company posted a gross profit rate of 65.1%, a slight increase from the previous year. Operating expenses stood at $609 million for the quarter, a rise from $546 million in the previous year. However, as a percentage of sales, operating expenses improved to 50.4%, compared to 51.7% last year. The firm’s operating income climbed to $179 million, a considerable increase from last year’s $138 million. Non-GAAP earnings per share (EPS) of $2.50 surpassed consensus projections by $0.12.

As of the quarter’s end, the company reported total liquidity of approximately $1.1 billion, comprised of cash and equivalents of $683 million and a borrowing capacity of $500 million under the senior secured asset-based revolving credit facility. Other current assets included $56 million in current investments, while inventories were reported at $693 million.

Considering the Q3 outperformance and the positive outlook for Q4, the company has raised its full-year sales forecast. It expects net sales for the year to range from 14% to 15%, up from the previous estimate of 12% to 13%. Operating margin is anticipated to be around 15%. Meanwhile, capital expenditure is projected at approximately $170 million. Real estate activity will reflect roughly 20 net store openings – 60 new openings, 40 closures – and 60 remodels and right-sizes.

What Is the Price Target for ANF Stock?

The stock has been on an upward trend, climbing over 88% in the past year. It trades in the upper half of its 52-week price range of $72.98 – $196.99 and demonstrates ongoing positive momentum as it trades above all major moving averages. With a P/S ratio of 1.56x, it trades at a relative discount compared to the Apparel Retail industry average of 2.4x.

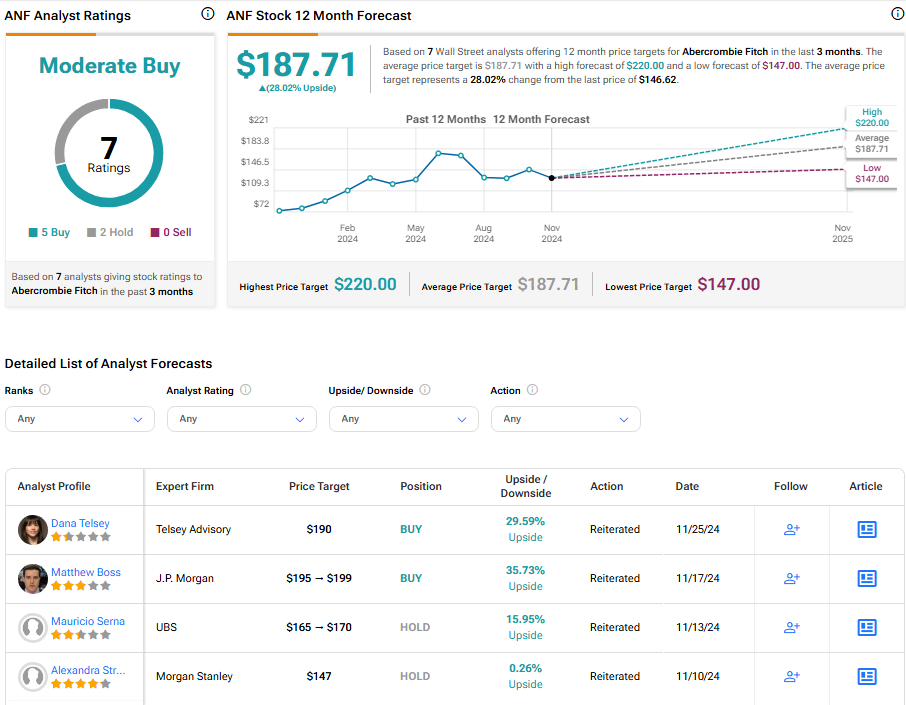

Analysts are mostly bullish on its prospects. Dana Telsey, CEO of Telsey Advisory Group, maintained an Outperform rating with a price target of $190 on the shares following Tuesday’s earnings report, noting that sales continued to accelerate, helping drive growth.

Seven analysts recommend Abercrombie & Fitch as a Moderate Buy. The average price target for ANF stock is $187.71, representing a potential 28.02% upside from current levels.

Final Analysis on ANF

Abercrombie & Fitch has shown robust growth and resilience in a challenging retail climate. Its continued focus on expansion, enhanced operational efficiency, and impressive financial results underscore its strength. While the brand’s recent share performance suggests the market has it “priced for perfection,” the stock’s relative undervaluation indicates an opportunity with further potential upside for discerning value investors.