As we approach the end of 2024, the year has been defined by a strong bull market, continuing the momentum that began last year, driven by trends in Artificial Intelligence (AI), consumer spending, and the impact of the election year. The optimism surrounding AI, combined with technological innovations and sector advancements, has propelled the performance of major ETFs like the SPDR S&P 500 ETF Trust (SPY) and Invesco QQQ ETF (QQQ). Also, some mega-cap stocks (companies valued over $200 billion) have exceeded growth expectations. However, not all market giants have been able to keep pace.

Confident Investing Starts Here:

- Easily unpack a company's performance with TipRanks' new KPI Data for smart investment decisions

- Receive undervalued, market resilient stocks right to your inbox with TipRanks' Smart Value Newsletter

In this article, we will analyze the biggest winners and losers among the mega-caps of 2024 using TipRanks’ screener, examining the factors that have either fueled or hindered their results throughout the year.

The Top 3 Biggest Gainers

Among the three main mega-cap stocks, the podium is dominated by the leading chipmakers worldwide, who have been largely responsible for driving the broad market’s strong performance throughout the year.

1. NVIDIA Corporation

Arguably one of the most discussed and significant stocks of the moment, Nvidia (NVDA), based in Santa Clara, California, has seen its market capitalization exceed $3.2 trillion. Its shares have surged by 174.1% year-to-date.

As the global leader in graphic processing units (GPUs) and AI computing, Nvidia achieved a remarkable 152% year-over-year revenue growth this year. Looking ahead, its revenues are projected to grow by an additional 51% in Fiscal 2026.

Currently, Nvidia is rated as a Strong Buy, with 37 out of 40 analysts covering the stock maintaining a bullish outlook. The average price target stands at $177.14, indicating an upside potential of 34.2%.

2. Broadcom Inc.

With the second-best performance of the year among mega-caps, the Palo Alto, California-based chipmaker Broadcom (AVGO), with a market capitalization exceeding $1.16 trillion, has risen 132.8% year-to-date.

Broadcom supplies essential chips for data centers, enterprise networking, and 5G infrastructure, with approximately 20-25% of its total revenue coming from Apple (AAPL). The company provides key components for Apple’s devices, including Wi-Fi and Bluetooth chips. Over the course of the year, Broadcom saw 44% year-over-year revenue growth, and projections for next year suggest a further 19% growth in revenue.

Among Wall Street analysts, Broadcom is rated a Strong Buy, with 23 out of 26 analysts maintaining a bullish outlook on the stock. However, the average price target is $228.09, indicating a potential downside of -8.76%.

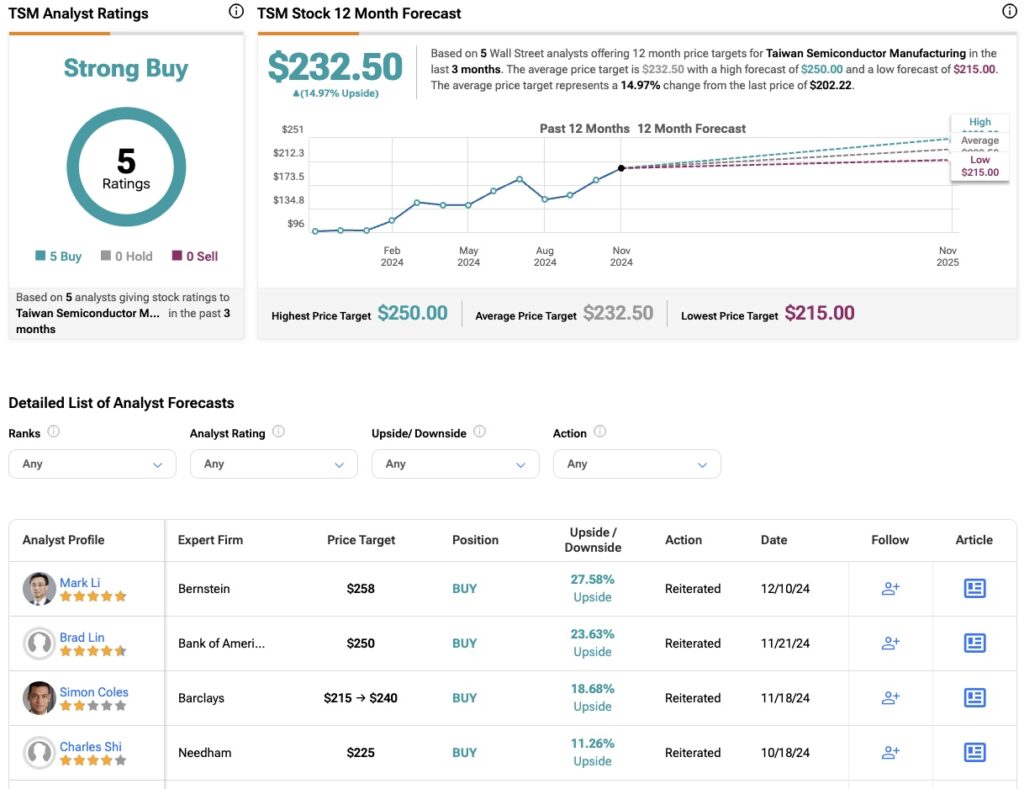

3. Taiwan Semiconductor Manufacturing Company (TSMC)

Taiwan Semiconductor Manufacturing Company (TSM), based in Hsinchu City, Taiwan, completes the podium with an impressive 101% gain year-to-date, now valued at $1.04 trillion. The company’s broad semiconductor portfolio, which spans high-performance computing, smartphones, and consumer electronics, has benefited significantly from the strong demand driven by AI trends. As a result, TSMC achieved 23% year-over-year revenue growth and is projected to see an additional 25% growth in Fiscal 2025.

The consensus among analysts points to further upside potential for TSMC. The company is rated a Strong Buy, with all five analysts covering the stock maintaining a bullish outlook. The average price target is $232.50, implying an upside potential of 14.97%.

The Top 3 Worst Performers

Although 2024 has seen a significant market rally in major indexes, not all companies have performed well. Among the biggest underperformers among mega-caps this year are two well-known technology companies and a major pharmaceutical company.

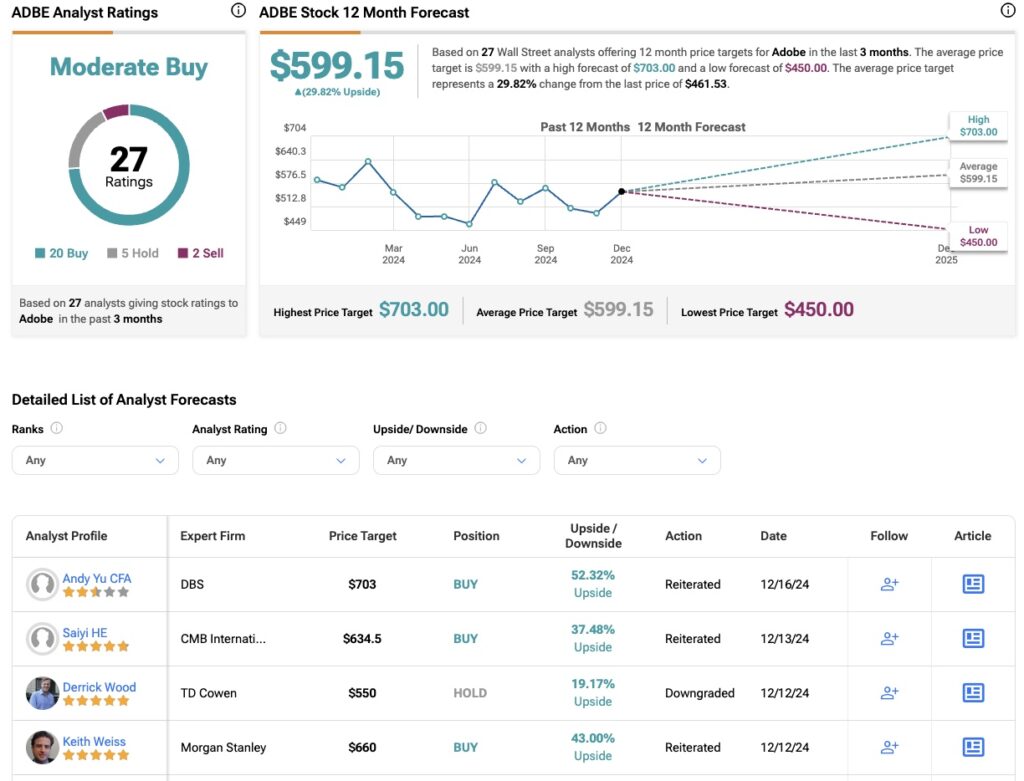

1. Adobe Inc.

Starting with Adobe, the San Jose, California-based software company has seen its market value drop by 20.4% so far this year, now standing at $203.17 billion. One of the main reasons for this underperformance has been Adobe’s inability to maintain strong growth rates amid the rising demand for AI. While revenues grew 11% year-over-year, this was somewhat disappointing compared to 10.2% growth in 2023.

Moreover, the company’s more cautious outlook, with revenues expected to grow by just 9.5% in Fiscal 2025, has added to the negative sentiment. This suggests that Adobe’s business may be reaching a more mature phase.

Even so, the consensus on Wall Street remains relatively positive, with 20 out of 27 analysts recommending a Buy. The average price target is $599.15, indicating a potential upside of 29.82%.

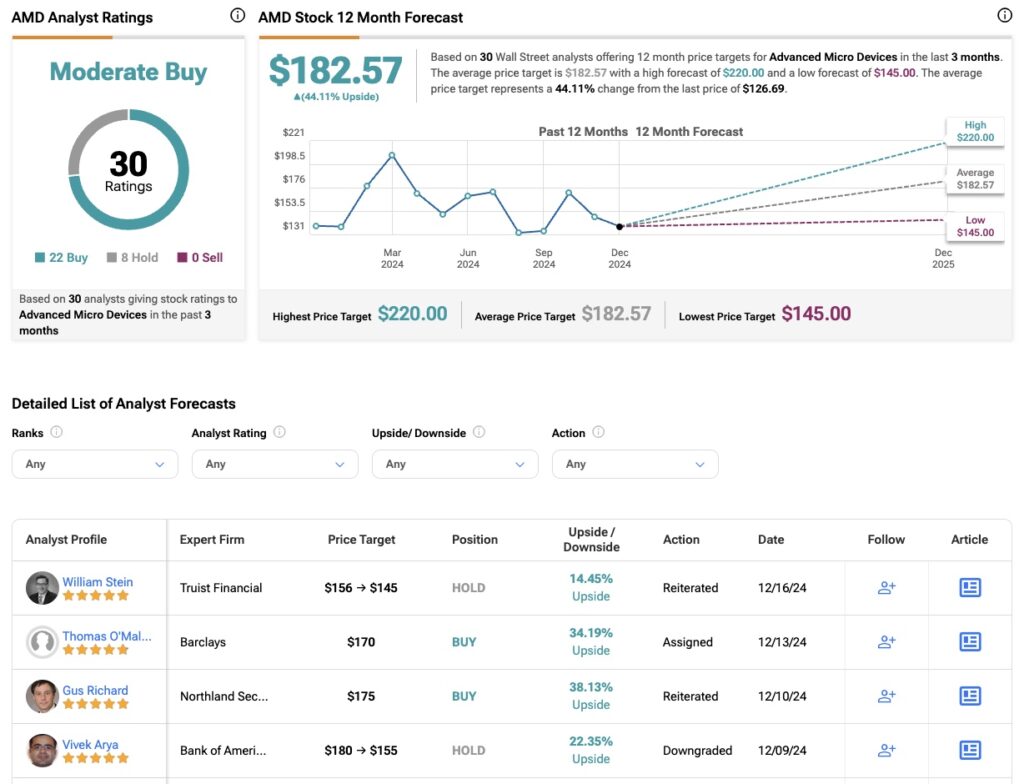

2. Advanced Micro Devices

In second place is Advanced Micro Devices (AMD), the chipmaker giant based in Santa Clara, California. The company’s value has dropped by 8.5%, bringing its market capitalization to $205 billion. Despite strong demand for AI-related products, AMD has struggled due to a combination of industry and company-specific factors. The key challenge has been Nvidia’s dominance in the AI chip market and Intel’s (INTC) recovery in the CPU space, both of which have impacted AMD’s profitability.

As a result, AMD’s revenues grew 9.9% year-over-year, marking a significant slowdown from the impressive growth streak between 2020 and 2022, when year-over-year growth ranged from 45% to 68% in 2021. Looking ahead, growth for Fiscal 2025 is projected to see a more robust growth rate of 27%.

Nevertheless, Wall Street remains generally optimistic about AMD, with a Moderate Buy rating. 22 out of 30 analysts recommend buying the stock. The average price target is $182.57, suggesting a potential upside of 44.11%.

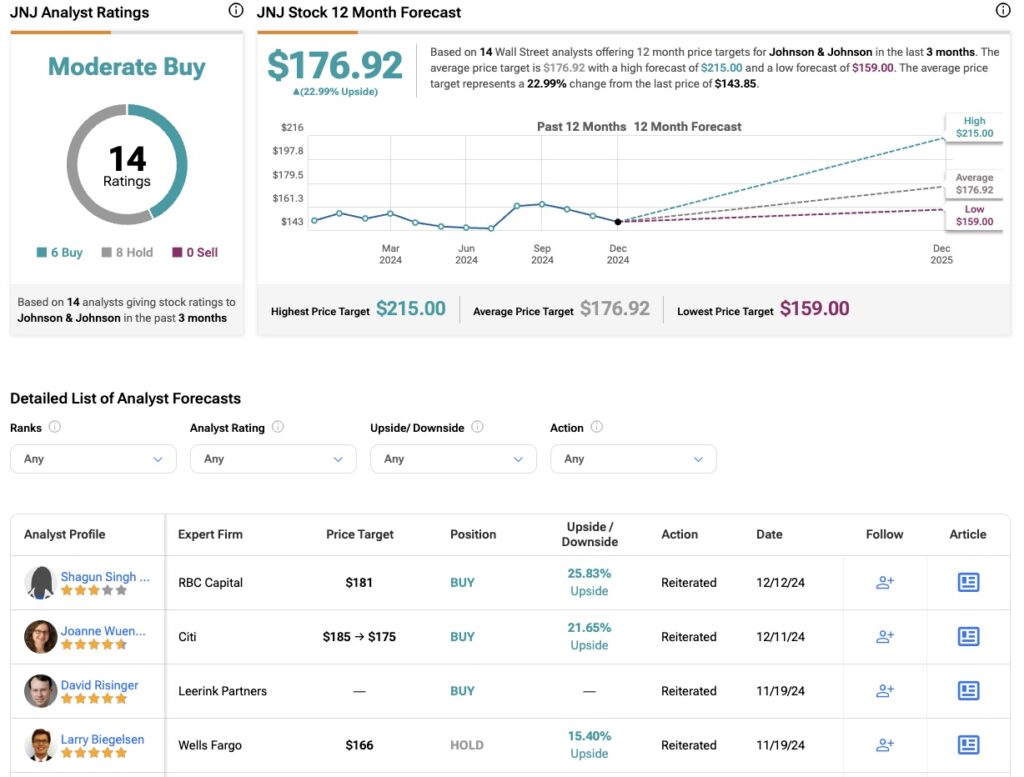

3. Johnson & Johnson

Rounding out the list is Johnson & Johnson (JNJ), the pharmaceutical giant based in New Brunswick, New Jersey. The company has underperformed this year, with a decline of around 7.2%, bringing its market capitalization to $346.3 billion. One of the primary reasons for this underperformance is slower growth in key segments, such as pharmaceuticals and surgical robots. Johnson & Johnson reported a modest 4.7% year-over-year revenue growth and is expected to see just 2.9% growth in Fiscal 2025.

The sharper decline since October can be attributed to bearish sentiment in the healthcare sector, driven by uncertainty over future policies. This uncertainty stems from speculation about potential changes in leadership at the Department of Health and Human Services (HHS). Additionally, concerns about elected President Trump’s influence on healthcare policy, particularly his support for alternative health approaches and vaccine skepticism, have further weighed on investor sentiment.

In light of these challenges, the consensus among analysts is somewhat mixed. J&J is rated as a Moderate Buy, with only six out of 14 analysts being bullish on the stock. The average price target is $176.92, implying an upside potential of 22.99%.

Looking for a trading platform? Check out TipRanks' Best Online Brokers guide, and find the ideal broker for your trades.

Report an Issue