It would be easy to brush design software leader Autodesk (ADSK) aside as a comparative unknown, but whether you’re familiar with the company or not, it still posted a winner with its latest earnings report. The news was an all-around win sufficient enough to send the company’s shares up in after-hours trading on Wednesday.

Confident Investing Starts Here:

- Easily unpack a company's performance with TipRanks' new KPI Data for smart investment decisions

- Receive undervalued, market resilient stocks straight to you inbox with TipRanks' Smart Value Newsletter

Autodesk posted adjusted earnings of $1.65 per share, which handily beat analysts’ estimates calling for $1.57 per share. Revenue also came out ahead of projections. While the consensus called for $1.22 billion in revenue, Autodesk posted $1.24 billion.

The last 12 months for Autodesk shares were on a fairly steady decline. At least, until recently. This time last year, Autodesk shares were up over $342 per share. The value slipped going into September but saw a rally in mid-October that saw shares ultimately hit just over $329.

The rally lost steam in mid-November and began a slump that lasted all the way to mid-June. That was when the company hit $164. Another rally followed, and now, the company is challenging $230 per share in Wednesday’s after-hours session.

It was a win for Autodesk no matter how you slice it, but can Autodesk keep its streak alive? A look at the conditions and Autodesk’s prospects suggests something of a dim picture. Thus, I stand at neutral on Autodesk, a company with a great product line geared toward a target market that’s likely to come under heavy fire with an economic downturn.

Investor Sentiment is a Little Mixed for ADSK Stock

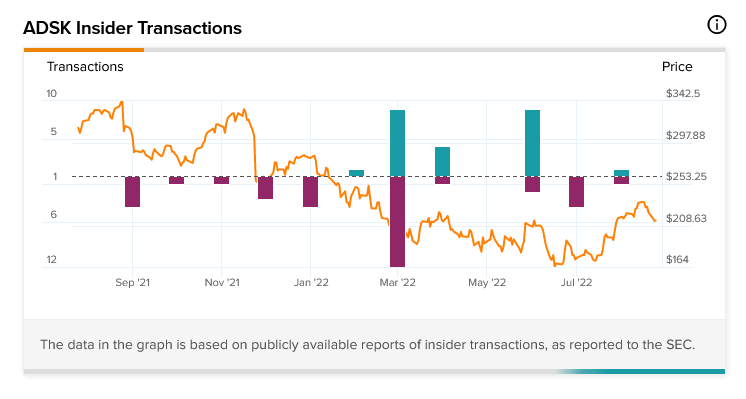

Analyst enthusiasm aside, there are some clear signs of concern coming out of the investor sentiment metrics around Autodesk. Currently, Autodesk has a 7 out of 10 Smart Score on TipRanks. That’s the highest level of neutral and suggests a somewhat better than even chance that the company will ultimately outperform the broader market. Despite this, however, insider trading is heavily sell-weighted. In the last three months, insiders sold $311,200 worth of Autodesk shares.

However, there’s one key point worth considering here. Yes, insiders sold off a larger quantity than they bought in aggregate, but more insiders bought in the last three months than sold. Autodesk saw 10 buy transactions but just seven sell transactions.

A look at the last 12 months suggests a larger problem in the making. Sell transactions led buy transactions by 33 to 24. While sellers are leading buyers by about three to two, the latest figures are increasingly buy-weighted. In fact, the buying activity started in earnest around January, when the company was into its big leg down ahead of the June recovery.

A Solid Win, but an Encore is Uncertain for ADSK Stock

Here’s the problem in a nutshell with Autodesk. It had a great quarter. There are no two ways about that. It beat estimates on every front, but the problem is, can it keep going? Certainly, there are those who see a path to victory here, and they’ve got a solid rationale. For instance, one report points out that the company’s share price has already been beaten down pretty heavily as a result of the general tech meltdown.

It also notes that the company’s subscription-heavy business model gives it a nice source of recurring income. Plus, that recurring income has already proven durable in the past. To top it off, its extensive product portfolio gives it an edge in diversification.

These are all perfectly valid points, but there’s a problem; none of these points were really proven during an economic downturn. Subscriptions do tend to be durable. After all, 78% of adults paid for a subscription service in the U.S. last year.

A subscription that has a direct impact on business operations is likely to be one of the last expenses thrown over. That’s particularly true in the case of low-cost subscriptions. If there’s a $500 per month subscription and a $1 million capital budget, where do the most savings lie? Canceling the subscription? Or cutting the capital budget by 10%?

Those are strictly hypothetical numbers, of course, but the value of a subscription backed up by sheer inertia is likely to keep a subscriber in the fold, except for when money is particularly tight. Then, even that modest subscription fee may not hold out.

Autodesk is working to prevent this, however, by changing its subscription basis. The company is introducing “Flex Tokens,” which allows customers to budget their use of Autodesk services by buying a block of time on these platforms.

Further, Autodesk is stepping up its connection to customers by offering training programs. That’s likely to prove a smart move; trainers tend to be respected in their fields. The old adage about those who can’t do, teach, usually doesn’t apply in a field like this, and should those respected trainers promote their own products in the process, it’s just good business.

However, there are also troubles emerging. Autodesk has been cutting back on features in its products. Now, Autodesk is removing local simulations, regardless of what license tier is involved. There can be something to be said for simplifying a product, but simplification can strike customers as a bad deal if the simplification allows less to get done.

Is Autodesk Stock a Buy or Sell?

Turning to Wall Street, Autodesk has a Strong Buy consensus rating. That’s based on 13 Buys and two Holds assigned in the past three months. The average Autodesk price target of $259.07 implies 20.82% upside potential. Analyst price targets range from a low of $220 per share to a high of $290 per share.

Conclusion: Paths to Victory and Calamity for ADSK Stock

There is absolutely a case for Autodesk to succeed. The problem, however, is that there’s almost an equal case for Autodesk to not succeed. If the subscription model has sufficient value and inertia behind it, then it will likely come out the other side. That assumes that its client companies will at least pursue the status quo for a while. Autodesk’s training efforts should cement its brand in customers’ minds as a valuable source of information and insight as well as products.

Throw in the fact that Autodesk is trading just inches above its lowest price targets, and there’s plenty of upside to help sweeten the pot.

However, there are significant problems, too. If enough companies fold or cut back during the economic downturn, that’s going to hit Autodesk where it hurts. The reduction of features doesn’t exactly help. Insider trading isn’t exactly looking for a home run, either, though the resurgence of buying could prompt optimism.

So, with almost equal cases for win and loss before us, I stand neutral on Autodesk. It might deliver a big success. It might crash and burn. With no clear winner ahead, I’ll stay off the trail altogether.