Texas-based Western Midstream Partners (WES) operates midstream energy assets. Its business includes gathering and transporting natural gas and crude oil.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

Let’s take a look at the company’s latest financial performance, corporate developments, and risk factors.

Western Midstream Partners’ Q2 Financial Results and 2021 Guidance

The company generated revenue of $719.13 million in Q2 2021, compared to revenue of $671.76 million in the same quarter last year. It posted EPS of $0.55, compared to $0.60 a year ago, and consensus estimates of $0.57. (See Western Midstream Partners stock charts on TipRanks).

Western Midstream Partners’ remaining free cash flow in Q2 after making a distribution to shareholders was $246.8 million. It ended Q2 with $305.57 million in cash. The company’s capital expenditure in Q2 was $84 million. It expects full-year 2021 capital expenditure to be in the range of $275 million – $375 million.

Western Midstream Partners’ Corporate Developments

The company entered into a long-term agreement with Crestone Peak Resources for gas gathering and processing. As a result, Crestone dedicated all of its 74,000 acres in Watkins to Western Midstream Partners. Crestone plans to dedicate 148,000 additional acres in the future.

Western Midstream Partners’ Risk Factors

The new TipRanks Risk Factors tool reveals 50 risk factors for Western Midstream Partners. Since Q4 2020, the company has updated its risk profile with one new risk factor under the Production category.

Western Midstream Partners tells investors that there could be a significant increase in inflation in the U.S. economy, caused in part by government stimulus in response to the COVID-19 pandemic. The company noted that the pandemic has brought uncertainty to the global economic outlook. It cautions that a significant increase in inflation would drive up its costs for labor and materials, which would in turn adversely impact its profitability and cash distribution to shareholders.

The majority of Western Midstream Partners’ risk factors fall under the Finance and Corporate category, with 52% of the total risks. That is above the sector average of 37%. WES stock has gained about 43% since the beginning of 2021.

Analysts’ Take

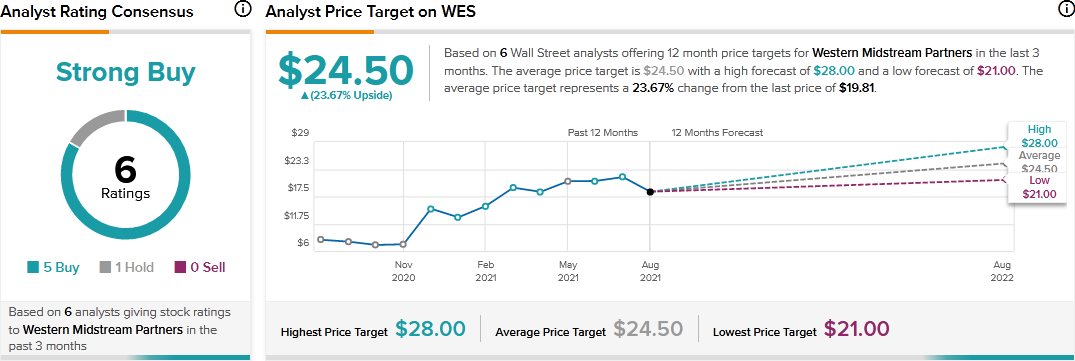

Following Western Midstream Partners’ Q2 report, RBC Capital analyst Elvira Scotto reiterated a Hold rating on WES stock with a price target of $21. Scotto’s price target suggests 6.01% upside potential.

Consensus among analysts is a Strong Buy based on 5 Buys and 1 Hold. The average Western Midstream Partners price target of $24.50 implies 23.67% upside potential to current levels.

Related News:

A Look at FS KKR Capital’s New Risk Factor After FSKR Merger

WM Technology Snaps Up Sprout; Shares Jump

FuelCell Posts Strong Q3 Results