Global organizational consulting services provider Korn Ferry (KFY) operates through four segments — Consulting, Digital, Executive Search, and Recruitment Process Outsourcing & Professional Search. Let us take a look at the company’s financial performance, along with the new risk factors declared by the company in its latest filing.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

Buoyed by the recovery from the COVID-19 pandemic, Korn Ferry’s fee revenue jumped 26% year-over-year to $555.2 million in Q4. Along with this record revenue, the company registered an all-time high EBITDA at $112.8 million in Q4, implying an EBITDA margin of 20.3%.

Additionally, Korn Ferry also bumped up its quarterly dividend by 20% to $0.12 per share. The dividend is payable on July 30 to shareholders of record on July 6. (See Korn Ferry stock chart on TipRanks)

Looking ahead to Q1, Korn Ferry estimates fee revenue to be in the range of $535 million to $555 million. It expects diluted earnings per share to be between $1.04 and $1.14.

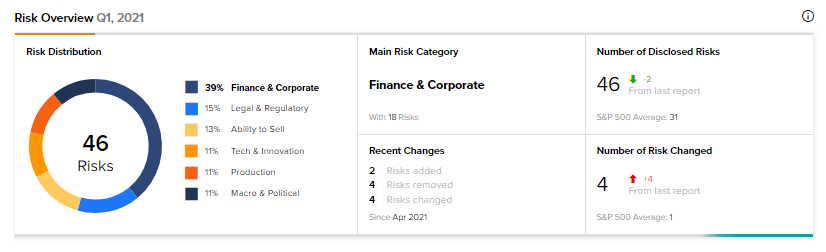

Korn Ferry Risk Factors

According to the new Tipranks Risk Factors tool, Korn Ferry’s main risk category is Finance & Corporate, which accounts for 39% of the total 46 risks identified for the stock. The next two major risk factor contributors are Legal & Regulatory and Ability to Sell at 15% and 13%, respectively. Since April, the company has added two new risk factors and removed four risk factors.

The company has added the new risks in the Legal & Regulatory category. It operates in different geographies and is subject to varied government regulations, which are complex in nature and may change over time and become more stringent. Future changes in legislation or macro policies may affect it adversely.

Further, Korn Ferry’s Digital services vertical and an increase in overall use of technology exposes the company to data privacy and cybersecurity laws across different countries, which may constrain its ability to pursue business opportunities.

Laws and regulations as well as investors’ expectations regarding the environment and climate change are evolving and this may increase the efforts and expenses needed to comply with these obligations.

Compared to a sector average Finance & Corporate risk factor of 35%, Korn Ferry is at 39%, indicating that owning the stock is risky versus the broader sector.

Following Korn Ferry’s Q4 performance, Robert W. Baird analyst Mark Marcon reiterated a Buy rating on the stock and increased the price target to $89 (32.5% upside potential) from $78.

Marcon said, “Beyond the global recovery, Korn Ferry is well-positioned to capitalize on several long-term opportunities, including boomer retirements, acceptance of flexible work models, and D&I/ESG. Additionally, the company has an opportunity to materially expand margins over the course of the next cycle.”

Based on 2 Buys and 1 Hold, consensus on the Street is a Moderate Buy. The average Korn Ferry price target of $80.67 implies 19.8% upside potential. Shares are up 143.9% over the past year.

Check out the Risk Word Cloud feature from our Risk factor tool, which highlights the most common risk factor phrases from Korn Ferry’s most recent filing, along with the most used phrases.

Related News:

TELUS International Snaps Up Playment

ChampionX Completes Acquisition of Scientific Aviation; Street Says Buy

Alpine Immune Announces Equity Offering Totaling $75M