Kimco Realty (KIM) is an American real estate company. It owns and operates shopping centers and other mixed-use properties.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

Let’s take a look at Kimco’s latest financial performance, corporate developments, and risk factors.

Kimco Realty’s Q2 Financial Report

The company reported revenue of $289 million for the second quarter of 2021. That compared to revenue of $238.9 million in the same quarter last year and exceeded consensus estimates of $272 million. Funds from operations (FFO) per share of $0.34 improved from $0.24 a year ago and beat consensus estimates of $0.31.

Kimco ended the Q2 with $2.2 billion in liquidity, including $2 billion under a revolving credit facility. The company plans to distribute a dividend of $0.17 per share on September 23. (See Kimco Realty stock charts on TipRanks).

Kimco’s Corporate Developments

In August, Kimco completed the acquisition of Sun Belt shopping center owner and operator Weingarten Realty Investors in a cash and stock transaction. The deal was announced in April. Kimco said the merger will enable it to create significant value for its investors. It expects to incur between $50 million and $60 million in merger-related costs in the Q3.

Kimco plans to raise $500 million through an equity offering. It intends to use the money from the offering for general corporate purposes, including acquisitions, funding development costs, and reducing outstanding debt.

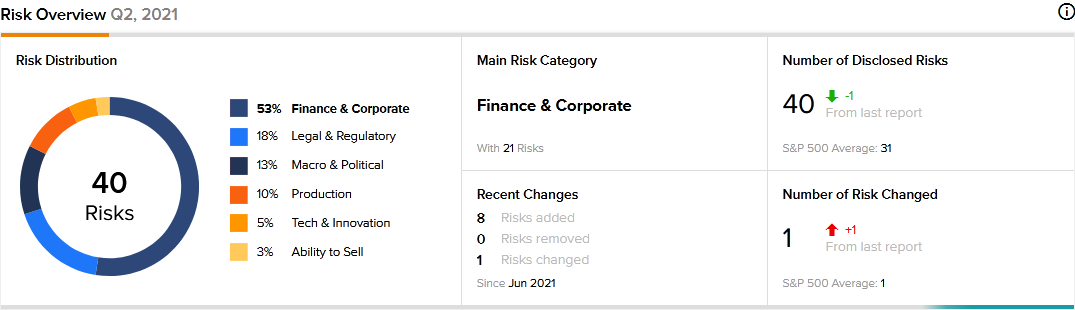

Kimco’s Risk Factors

The new TipRanks Risk Factors tool shows 40 risk factors for Kimco. Since Q4 2020, the company has updated its risk profile with eight new risk factors. All of the additional risk factors fall under the Finance and Corporate category and relate to the Weingarten acquisition.

Kimco tells its shareholders that the merger may dilute their position. It says that on closing the merger, its existing shareholders will own 71% of the combined company, while Weingarten shareholders will own 29%. As a result, legacy Kimco shareholders may have less influence over the company’s decisions than they did before the merger.

Kimco cautions investors that the merger will increase its debt and that it will incur substantial merger-related expenses to integrate Weingarten. As a result, the company said it could have fewer funds for working capital, development projects, and cash for distributions.

Further, Kimco tells investors that it may be unable to integrate Weingarten successfully or within the expected timeframe. As a result, it may not achieve the anticipated benefits of the merger.

Finance and Corporate is Kimco’s top risk category, accounting for 53% of the total risks. That is below the sector average at 58%. Kimco’s shares have gained about 40% since the beginning of 2021.

Analysts’ Take

Barclays analyst Anthony Powell recently initiated coverage of Kimco stock with a Buy rating and a price target of $27. Powell’s price target suggests 27.84% upside potential. The analyst noted that despite COVID-19 challenges and retail shifting online, shopping center leasing demand has been strong as traffic to shopping centers has rebounded to 2019 levels.

Consensus among analysts is a Moderate Buy based on 7 Buys and 4 Holds. The average Kimco Realty price target of $24.20 implies 14.58% upside potential to current levels.

Related News:

Pebblebrook Hotel Sells Villa Florence San Francisco for $87.5M

Wells Fargo Fined $250M for Not Paying Back Wronged Customers

What Can Investors Learn from Invitae’s Newly Added Risk Factors?