Massachusetts-based Apellis Pharmaceuticals (APLS) is engaged in developing treatments for a broad range of diseases. It recently won FDA approval for its drug EMPAVELI, which is designed to treat adults with paroxysmal nocturnal hemoglobinuria (PNH). The company has several drug candidates and continues to expand its pipeline.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

Let’s take a look at the company’s latest financial performance, corporate developments, and risk factors.

Apellis Pharmaceuticals’ Q2 Financial Results

Following the FDA’s approval for the EMPAVELI drug in May, Apellis Pharmaceuticals went on to generate $0.6 million in net product revenue in Q2. The consensus estimate for revenue was $0.81 million. Notably, the company did not generate any product revenue in the same quarter last year.

Apellis posted a loss per share of $2.72 compared to a loss per share of $1.57 in the same quarter last year. The consensus estimate called for a loss per share of $1.70. The company ended Q2 with $599 million in cash & cash equivalents. (See Apellis Pharmaceuticals stock charts on TipRanks).

Apellis Pharmaceuticals’ Corporate Developments

In addition to the FDA’s approval for the sale of EMPAVELI in the U.S., another key milestone during Q2 was the advancement of the development of Apellis’ various drug candidates.

Furthermore, the company announced a research collaboration with Beam Therapeutics (BEAM). The companies plan to partner on six research programs aimed at discovering new treatments for diseases that affect the brain, liver, and eye.

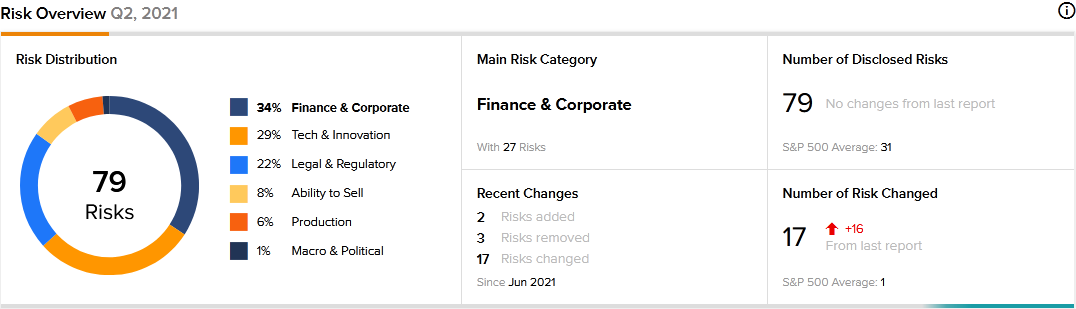

Apellis Pharmaceuticals’ Risk Factors

The new TipRanks Risk Factors tool reveals 79 risk factors for Apellis Pharmaceuticals. Since December 2020, the company has updated its risk profile to introduce two new risk factors.

In a newly added risk factor under the Finance and Corporate category, Apellis cautions that commercializing EMPAVELI may run into some challenges that could lead to massive losses for the company. It says that it has made significant investments in preparing the salesforce for EMPAVELI. Therefore, if the commercial launch of the drug is unsuccessful, its investment in its salesforce would be lost if it is unable to reposition the sales team. The company says that the inability of its sales team to access and educate physicians on the benefits of EMPAVELI over alternative treatments is one reason that could cause the drug’s commercial launch to fail.

Apellis tells investors in a newly added Legal and Regulatory risk factor that it expects its operating results to fluctuate significantly on a quarterly and yearly basis. The company says that it does not have significant experience in commercial operations. Therefore, it may encounter unexpected expenses, delays, and other challenges as it embarks on commercializing its recently approved EMPAVELI drug.

Finance and Corporate is Apellis’ top risk category, accounting for 34% of the total risks. That is above the sector average at 29%. Apellis’ shares have gained about 9% since the beginning of 2021.

Analysts’ Take

Jefferies analyst Chris Howerton recently initiated coverage of Apellis stock with a Buy rating and a price target of $74. Howerton’s price target suggests 18.17% upside potential.

The analyst believes that EMPAVELI could be a huge commercial success, estimating its sales potential to be more than $4 billion.

Consensus among analysts is a Strong Buy based on 11 Buys and 1 Hold. The average Apellis Pharmaceuticals price target of $81.22 implies 29.70% upside potential to current levels.

Related News:

A Look at Twist Bioscience’s Corporate Developments and Risk Factors

Campbell Soup Q4 Results Top Estimates

What Does Fulgent Genetics’ Newly Added Risk Factor Tell Investors?