DocuSign, Inc. (DOCU) shares jumped 5.3% to close at $274.43 on June 18, following an upgrade from Wedbush analyst Daniel Ives.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

DocuSign is a cloud-based electronic signature solutions platform that helps companies and individuals manage electronic agreements. (See DocuSign stock chart on TipRanks)

Through its platforms, DocuSign Agreement Cloud and DocuSign Notary, the company provides end-to-end solutions for all types of agreements on practically any device, from almost anywhere, at any time.

DocuSign has found a massive pull forward owing to the pandemic, as businesses are compelled to fast-track their transition to convenient and economical digital platforms, compared to slow and expensive traditional, paper-based agreement processes.

In its latest quarter ending April 30, DocuSign added its millionth customer to the DocuSign platform, with customers ranging from small businesses to large Fortune 500 organizations.

The company recorded better-than-expected revenue and earnings in the first quarter and provided upbeat guidance for the second quarter and full Fiscal year 2021.

For Q2 and FY21, the company projects revenue to fall in the range of $479 – $485 million and $2.03 – $2.04 billion, respectively. Street estimates for the same are pegged at $473.68 million and $1.98 billion.

Analyst’s View

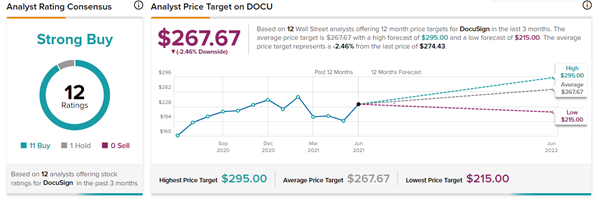

Following the Feds latest statement on monetary policy, Ives reiterated a Buy rating on the stock and lifted the price target to $290 (from $260), implying 5.7% upside potential to current levels.

Ives believes the Fed’s statement is “very bullish” for tech stocks and stated that in his view, the digitization of the consumer and enterprise ecosystem is still in the nascent stages of capturing a $2 trillion market opportunity over the next decade.

Ives said, “With the DocuSign Agreement Cloud as well as its CLM offering (SpringCM) providing many additional use cases beyond just signing a contract, DocuSign is continuing to expand throughout the entire deal process which is a major differentiator in this environment.”

Ives believes that DOCU is in a “sweet spot” and will benefit from continued momentum as an increasing number of customers turn towards digitization for their E-Signing and other agreement-related needs.

With 11 Buys and 1 Hold, DocuSign has a Strong Buy consensus rating. The average DocuSign analyst price target of $267.67 implies 2.5% downside potential to current levels. Shares have gained 63.1% over the past year.

Related News:

GE Announces Date of 1-for-8 Reverse Stock Split, Declares Regular Quarterly Dividend

ArcelorMittal Offloads Cliff’s Remaining Shares; Rewards Shareholders with $750M Share Buyback

U.S. Steel Provides Upbeat Q2 Guidance; Shares Plunge on Worries of Increased Metal Supply