Technology hardware and data storage provider Western Digital Corp. (WDC) delivered better-than-expected first-quarter results aided by strong demand for its Cloud products, continued innovation, and overall efficient execution and market penetration. However, shares plunged 10.3% in the extended trading session on October 28 as WDC’s earnings guidance fell short of expectations.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

The company reported earnings of $2.49 per share, up a whopping 283% year-over-year and significantly better than analyst estimates of $2.11 per share. (See Insiders’ Hot Stocks on TipRanks)

Additionally, revenue increased 29% compared to the prior-year quarter to $5.05 billion and also surpassed Street estimates of $4.36 billion. Compared to the year-ago period, WDC’s Cloud revenue climbed 72%, Client revenue grew 6%, and Consumer revenue increased 10%.

Citing supply-chain challenges and COVID-19-related impacts, David Goeckeler, Western Digital CEO, said, “While these disruptions are transitory, the long-term opportunities for Western Digital remain unchanged as the world’s digital transformation continues to accelerate. We believe that the migration to the cloud and demand for storage solutions throughout the client and consumer markets will continue to drive a huge opportunity for Western Digital and our customers.”

Based on the continued business momentum, WDS guided for second-quarter revenue to be in the range of $4.70 – $4.90 billion, higher than the consensus estimate of $4.59 billion.

However, earnings are expected to fall in the range of $1.95 – $2.25 per share, lower than the consensus of $2.39 per share.

In response to WDC’s performance, Robert W. Baird analyst Tristan Gerra lowered the price target on the stock to $75 (31% upside potential) from $100 while maintaining a Buy rating.

Gerra noted that Western Digital’s hard disk drive (HDD) guidance hampered investor confidence as the company attributed global supply-chain and manufacturing issues to the lower outlook. Further, the analyst expects a rebound in HDD revenue in the March 2022 quarter, as well as a sequential rebound in earnings in the September 2022 quarter.

Gerra said, “Accelerated debt deleveraging is a positive which will drive multiple expansion over time. While business model sees the near-term impact of inventory digestion in data centers and PCs along with overall macro weakness, we expect operating leverage longer-term, driven both easing comps and the introduction of new architectures.”

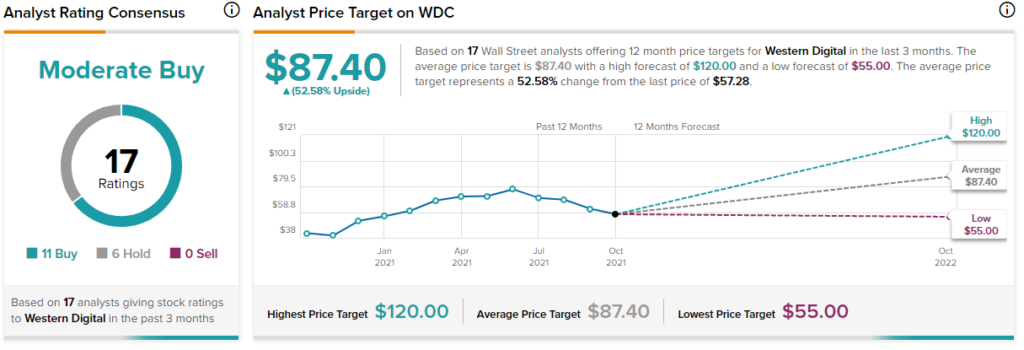

Overall, the stock has a Moderate Buy consensus rating based on 11 Buys and 6 Holds. The average Western Digital price target of $87.40 implies 52.6% upside potential to current levels. Shares have gained 50.3% over the past year.

Related News:

ADP Beats Q1 Expectations; Shares Hit All-Time High

General Motors Plunges 5.4% Despite Exceeding Q3 Expectations

Dynatrace Falls 9.9% Despite Posting Strong Beat-and-Raise Q2 Results