Walmart is in talks with the Tata group to snap up a $20 billion to $25 billion stake in the proposed retail app of India’s salt-to-software conglomerate, according to a Mint report.

The proposed ‘super app’, which is expected to be launched in December or January, aims to create a digital services behemoth offering a wide range of products in the retail space, including healthcare, food and grocery ordering, insurance and financial services, according to the report. The valuation of the digital super app platform is estimated at around $50 billion to $60 billion.

If the deal goes through, it would be the country’s largest deal in the retail space, following Walmart’s (WMT) May 2018 purchase of a 66% stake in Flipkart for $16 billion. One of the discussed options, would see the app launch as a joint venture between Tata and Walmart, which will enable leveraging on the synergies between Tata’s e-commerce business and Flipkart, according to the report.

“Walmart is keen to get a strong brand backing its e-commerce business, while Tata group wants a global name and an established player in the online space to boost sales of products currently sold through Tata group’s retail subsidiaries and online platforms to be able to compete against Reliance Industries’ Jio Platforms and Amazon,” Mint cited one person speaking on condition of anonymity.

The digital retail platform is proposed to be run by Tata-Walmart together, with the possibility of other foreign investors taking a share. Goldman Sachs has been appointed as the investment banker by Walmart for the proposed transaction, Mint reported.

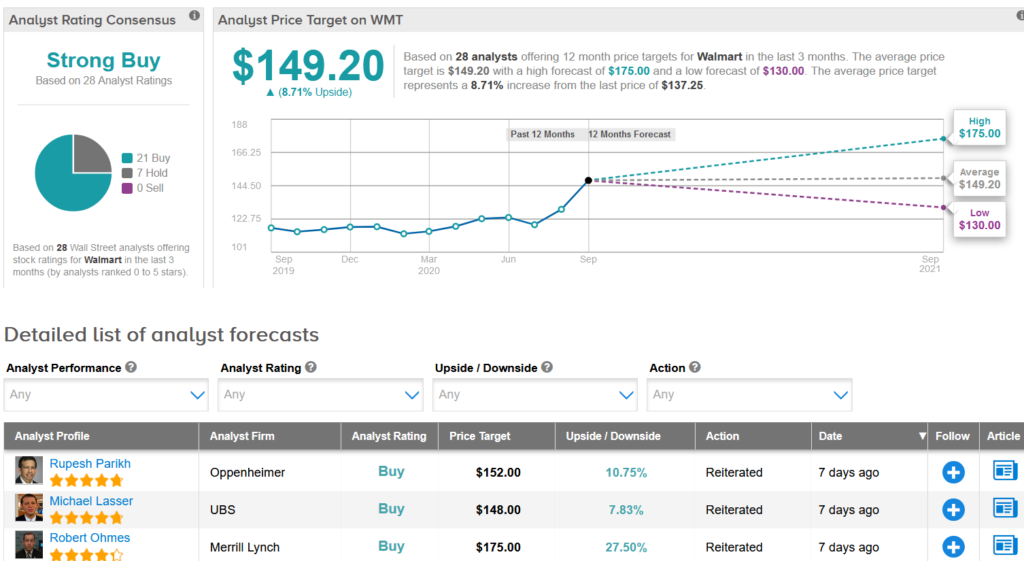

Shares in Walmart have been going from strength to strength since hitting a low in March and are now trading 15% higher than at the start of the year. What’s more, the $149.20 average price target implies 8.7% upside potential over the coming year.

Oppenheimer analyst Rupesh Parikh last week raised the stock’s price target to $152 (11% upside potential) from $145 and maintained a Buy rating, saying that the bull case remains intact with further upside potential amid expectations for continued aggressive investments within the business.

“We still see the case for outperformance driven by the potential to deliver at least LSD operating income growth and upside potential related to new investments,” Parikh wrote in a note to investors. “In coming years, we expect WMT to be one of the bigger beneficiaries related to retail dislocations in the brick & mortar landscape due in large part to the continued omni-channel investments.”

Commenting on the stock’s valuation, the analyst noted that on a relative P/E basis, WMT shares trade at 1.18x below recent peaks. “Similar to other higher performing companies in our universe, shares trade at historical peaks on absolute NTM P/E and EV/EBITDA. These metrics do not capture successful digital investments to date such as JD.com and Flipkart,” he added.

The rest of the Street is in line with Parikh’s bullish stance. The Strong Buy analyst consensus boasts 21 Buy ratings versus 7 Hold ratings. (See Walmart’s stock analysis on TipRanks).

Related News:

US Judge Rules In WeChat’s Favor; Blocks Trump’s Download Ban

Twitter Expands Policy To Block Misinformation Posts Ahead Of US Election

Google Scraps Plan To Rent Large Office Space In Dublin – Report