Viatris Inc. (VTRS) recently reported a fourth quarter that fell short of Wall Street expectations, missing revenue and earnings targets. The company, known for its wide array of generic and branded medicines, is venturing into the weight loss market with applications submitted for generic versions of top-selling weight loss drugs. Looking ahead, Viatris is setting its sights on challenging existing patents and providing more affordable weight loss medication alternatives. However, Viatris’ vision has been met with skepticism, with its stock down roughly 15% in the immediate aftermath of Q4’s results.

In Pursuit of a Generic GLP-1

Viatris Inc. uniquely combines generic and branded drugs efficiently, providing affordable medical solutions to various international healthcare markets. The company boasts an extensive portfolio, which includes more than 1,400 approved molecules, and offers high-quality generic and branded medicines to over 165 countries worldwide.

The company is currently developing generic versions of Novo Nordisk’s famous weight loss drugs, Ozempic and Wegovy, both containing semaglutide. It has filed applications with regulatory bodies while also challenging Novo Nordisk’s semaglutide patents. A review of U.S. Patent No. 10,335,462, covering dosage regimens for semaglutide in treatments of diabetes and obesity has been initiated, with a decision expected by October 2025.

The GLP-1 semaglutide is currently a leading market player for obesity drugs. JP Morgan Research predicts that the GLP-1 market will grow to $100 billion by 2030 due to the rising demand for obesity and diabetes medications.

While advanced drugs continue to emerge, Viatris projects the continued market relevance of semaglutide, citing its proven effectiveness in clinical trials. Reports have shown that nearly 77.1% of semaglutide trial participants achieved at least a 5% decrease in weight. Thus, a generic version could offer a cheaper alternative to a broader population.

Prioritizing Return of Capital

In 2024, Viatris reported total revenue of $14.7 billion, a U.S. GAAP net loss of $634 million, an adjusted EBITDA of $4.7 billion, US GAAP diluted EPS loss of $0.53 per share, an adjusted EPS of $2.65 per share, and a U.S. GAAP net cash amount of $2.3 billion generated by operating activities. The company also generated a free cash flow of $2 billion, surpassing its guidance, even accounting for around $650 million in transaction-related costs.

The company declared a quarterly dividend of 12 cents, to be paid on March 18, 2025, for shareholders of record at the close of business on March 10, 2025. This marks the fifth year in a row that the company has paid a dividend. Further, its Board of Directors approved a 2025 dividend policy amounting to 48 cents per share.

For 2025, Viatris plans to prioritize capital return, budgeting between $500 million and $650 million for share repurchases. Management is anticipating important late-stage development milestones for innovative assets Selatogrel, Cenerimod, and Sotagliflozin, along with six Phase 3 data results. Viatris is also prepared for the expected financial impact of the warning letter and import alert associated with the Indore facility.

Analysts Say Caution Warranted

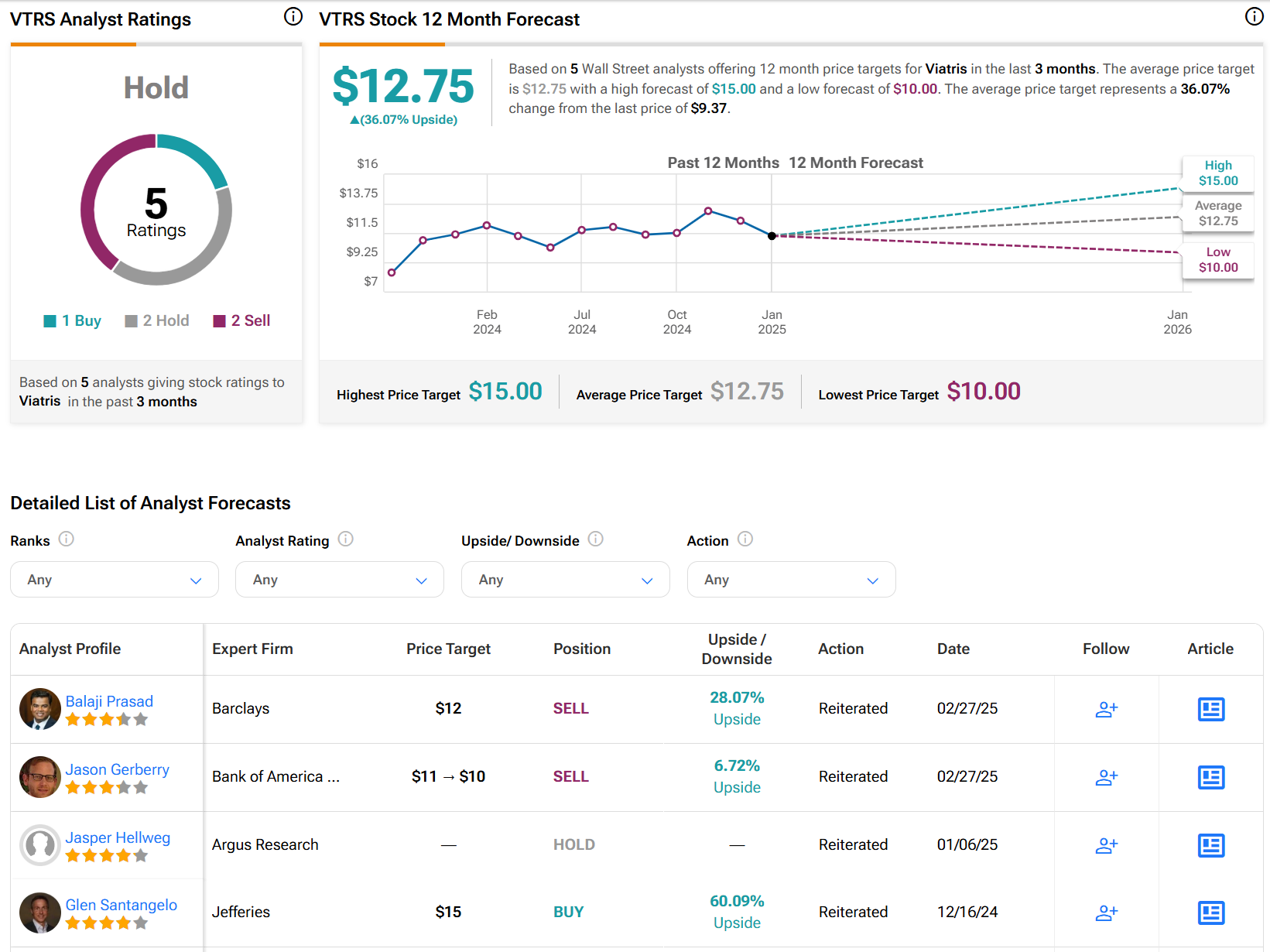

Analysts following the company have warned that caution is warranted on the stock. Bank of America has reiterated an Underperform rating on the shares and reduced the price target to $10 (from $11) due to disappointing FY25 EBITDA guidance and skepticism about the company’s shift to a branded growth strategy. Similarly, Barclays has downgraded VTRS’s target price to $9 (from $12) while keeping an Underweight rating. A 15% drop in the stock amid issues with the Indore Facility impacting the 2025 outlook led to this decision, with resolving this issue crucial for any potential stock recovery.

Viatris is rated a Hold overall, based on the recent recommendations of five analysts. The average price target for VTRS stock is $12.75, which represents a potential upside of 36.07% from current levels.